Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI BRIEF: Cleveland Fed Paper Sees Inflation Higher For Longer

- China’s Population Starts Shrinking, First Drop Since 1960s, Bbg

- ECB MAY OPT FOR 25-BP HIKE IN MARCH AFTER 50-BP MOVE IN FEB, Bbg

- DAVOS-IMF MD: EXPECT GROWTH TO FURTHER DECELERATE IN 2023, Bbg

- DAVOS- IMF MD SAYS EXPECT GROWTH TO DECELERATE TO 2.7 PCT IN 2023, Bbg

Key links: MNI NORGES WATCH: Norges Seen Keeping Hike For March Meeting / MNI POLICY: BOE Looks At Raising Equilibrium Jobless Estimate / MNI BoJ Preview - January 2023: Stick Or Twist / US Treasury Auction Calendar / US$ Credit Supply Pipeline

US TSYS: Yld Curves Bear Steepen Ahead Heavy Data Docket Wednesday

Tsys holding modestly mixed levels after the bell, near top end narrow range since midmorning, yield curves bouncing off deeper inverted levels (2s10s +7.413 at -66.082). Tsys mirrored similar moves in German Bunds in early trade, gapped higher after Bbg story hit wires: "ECB Starts to Ponder Slower Hikes After Half Point in February".

- Tsys extended past early overnight highs (30YY slips to 3.6135% low vs. 3.6948% high) following the headlines while equities bounced to new session highs briefly before moving back to early session range.

- Muted react to limited data (NY FED EMPIRE STATE MFG INDEX -32.9 JAN) participants plied the sidelines ahead Wednesday's heavy data docket that includes Retail Sales, PPI, IP/Cap-U, Business Inventories, Net TIC flows.

- Fed Funds implied hikes have shifted lower, continuing through the session after a sizeable miss for the admittedly volatile Empire mfg index.* 27bp for Feb 1 (unch from Fri close), cumulative 46bp for Mar (-1bp), 57bp to 4.90% terminal in Jun (-2.5bp) before 48bp of cuts to 4.42% for Dec (-5.5bp).

- Comes ahead of the BoJ overnight and tomorrow's stacked docket including multiple important data releases, four Fed speakers (incl Bullard at 0930ET not showing on BBG calendar) and the Fed Beige Book.

- Equity earnings resume, Goldman Sachs just annc ($10.59B 4Q rev vs. $10.7B est, $3.32 EPS), Morgan Stanley (sales & trade rev's $1.42B vs. $1.68B est);, UAL and Interactive Brokers after the close. Earnings on tap early Wednesday: Charles Schwab, Prologis Inc, JB Hunt Transport, PNC Financial Services.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00286 to 4.31657% (+0.00286/wk)

- 1M +0.00514 to 4.47000% (+0.01557/wk)

- 3M +0.00286 to 4.79757% (+0.00514/wk)*/**

- 6M +0.00528 to 5.12071% (+0.01957/wk)

- 12M +0.00229 to 5.39500% (+0.03800/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.82971% on 1/12/23

- Daily Effective Fed Funds Rate: 4.33% volume: $110B

- Daily Overnight Bank Funding Rate: 4.32% volume: $281B

- Secured Overnight Financing Rate (SOFR): 4.30%, $1.101T

- Broad General Collateral Rate (BGCR): 4.27%, $445B

- Tri-Party General Collateral Rate (TGCR): 4.27%, $418B

- (rate, volume levels reflect prior session)

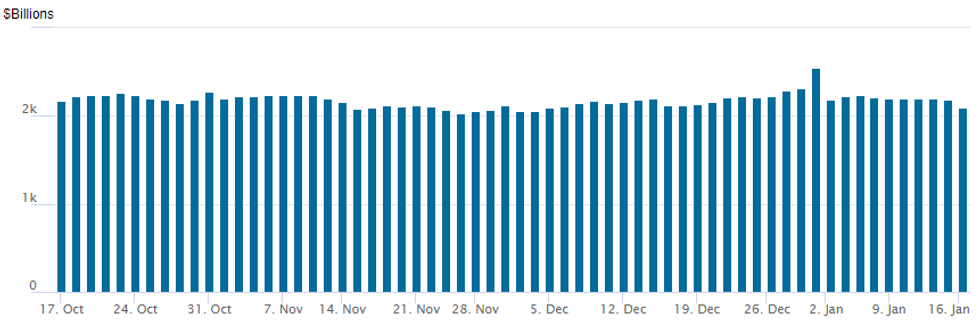

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,093.328B w/ 103 counterparties vs. prior session's $2.179.781B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Better low delta put and put spread trade noted upon US FI markets return from extended holiday weekend, gradual pick-up in rate-hike pivot away from more hawkish stance.- SOFR Options:

- -6,000 SFRU3 94.75/95.75 strangles, 15.5

- Block, 4,000 SFRJ3 95.25/95.43 call spds 1.5 over SFRJ 94.81 puts

- 2,600 SFRU/SFRZ2 94.50/95.00/95.50 put fly spds

- Block, 10,000 SFRM3 94.50/94.75 put spds .25 over OQM3 95.00 puts

- Broken call tree w/ put fly strip 1.0 over put spd package:

- +25,000 SFRJ3 95.06/95.12/95.25 broken call trees w/

- +25,000 SFRJ 94.87/95.00/95.12 put flys vs. SFRJ3 94.87/94.93 put spd

- Block, 25,000 SFRM3/SFRU3 94.68/94.75 call spd strip, 2.0 total

- Block, 5,000 SFRZ3 94.68/94.75 put spds, 1.0 ref 95.62

- 3,000 SFRH3 94.75/95.00/95.25/95.50 call condors, ref 95.145

- Block, 1,250 SFRM3 94.62/94.75/94.87 put flys, 0.75 ref 95.09

- Block, 2,000 SFRU3 94.62/94.75/94.87/95.00 put condors, 2 net ref 95.255

- Block, 10,000 SFRM3 94.50 puts .25 over OQM3 94.75 puts

- 4,000 SFRH3 95.25/95.43 call spds ref 95.14

- 5,750 SFRU3 95.00/95.50/96.00 call flys

- Treasury Options:

- 2,700 TYG 113/114 put spds, 15 ref 114-20.5

- 3,000 FVG 109.5 puts, 29.5 ref 109-12.5

- +5,500 TYG 114 puts, 19 ref 114-28

- 23,000 wk3 10Y 113.25/114.25 put spds, 15 ref 114-16.5

- over 7,600 wk3 TY 116 calls ref 114-18

- 4,700 TYG 114.25/116.25 call spds ref 114-18

- 2,500 TYG 115.5 calls, 14 ref 114-18

- Over 8,500 wk3 TY 114 puts, 15

- 3,500 TYH 115.5 calls, ref 114-19

- over 6,800 TYG 116 calls, 8-10 ref 114-21.5

- over 6,400 TYG 114.25 puts, 26-30

- 5,000 TYG 115.25 calls, 23 ref 114-23.5

EGBs-GILTS CASH CLOSE: Rally On Another Dovish ECB Report

European bonds rallied Tuesday as Bloomberg published a sources piece pointing to a final 50bp ECB hike in Feb with smaller hikes starting in March.

- Similar to the price action following last week's MNI sources piece that pointed to potential for a dovish stepdown in the hiking pace, terminal ECB hike pricing fell sharply (by 17bp at one point).

- Bunds held their gains made in the aftermath, with the curve bull steepening.

- 10Y BTP/Bund spreads tested last week's 8-month low of 177bp, but closed the session a little wider of that. GGBs underperformed as Greece sold new 10Y via syndication.

- Gilts underperformed overall but moved to new session highs on the ECB report. Earlier, UK labour market data showed wage growth a little stronger than expected but the rest of the report was mixed.

- Bonds' strong close came in spite of overnight event risk ahead, with the Bank of Japan decision expected around 0300GMT, and UK CPI at 0700GMT.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

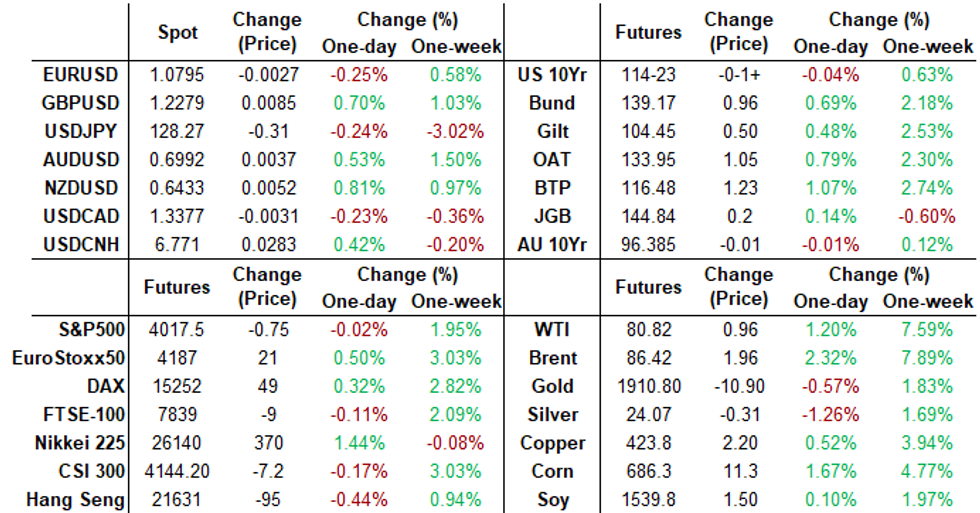

- Germany: The 2-Yr yield is down 10.9bps at 2.457%, 5-Yr is down 8.2bps at 2.108%, 10-Yr is down 8.4bps at 2.091%, and 30-Yr is down 5.6bps at 2.091%.

- UK: The 2-Yr yield is down 5.4bps at 3.462%, 5-Yr is down 3.6bps at 3.276%, 10-Yr is down 6bps at 3.324%, and 30-Yr is down 6bps at 3.667%.

- Italian BTP spread down 4.2bps at 180.1bps / Greek up 5.3bps at 203.6bps

EGB Options: Plenty Of Puts In German Instruments

Tuesday's Europe rates/bond options flow included:

- OEH3 116.50/114.50ps 1x2 vs OEH3 116.00p, bought the ps for 17 in 4k

- OEH3 116.75/116.25ps, bought for 12.5 in 5k

- OEH3 116.75/116.25 put spread sold at 9 in 5k

- DUH3 105.60/105.50/105.30/105.20p condor, bought 1.75 in 4k

- RXH3 136/135ps, bought for 18.5 in 2k

- RXH3 133.5/132 put spds bought for 18-19/0.06% in 5k

- RXH3 131.00 put bought for 13 in 6k. Hearing short cover

- ERM3 96.00 put v 0RM3 95.75 put, buys the front for 0.5 in 10k

FOREX: Broad Euro Weakness Following ECB Report, USDCNH Extends Bounce

- Despite EURUSD rising to within close range of trend highs above 1.0850 in early trade on Tuesday, a Bloomberg report quickly dampened sentiment for the single currency.

- ECB policymakers are said to be starting to consider a slower pace of interest-rate hikes than President Christine Lagarde indicated in December, according to officials with knowledge of their discussions.

- Following the piece, ECB terminal rate pricing briefly dropped as much as 17bp and the Euro traded with a negative bias for the remainder of Tuesday’s session, currently residing 0.25% lower against the greenback around 1.0795. Initial firm support lies further away at 1.0680, the 20-day EMA.

- The relative Euro weakness was more pronounced in the crosses with the likes of EURGBP and EURNZD dropping ~1%.

- USDJPY lacked direction are largely respected the 128-129 range ahead of the much anticipated BOJ meeting & decision due overnight. Options markets are implying moves of approx 275 pip in either direction to cover the premium paid on an ATM straddle, a sure sign that markets are anticipating acute volatility in the wake of the decision.

- USDCNH has risen roughly half a percent, in very similar fashion to Monday’s price action, which may be a reflection of the stabilisation for the greenback but also pre-positioning ahead of lunar new year.

- Aside from the BOJ, UK December CPI, US PPI & retail sales highlight Wednesday’s data calendar.

FX: Expiries for Jan18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0595-05(E558mln), $1.0746-60(E674mln), $1.0815(E575mln), $1.0850-60(E657mln)

- USD/JPY: Y130.70($510mln)

- GBP/USD: $1.1800(Gbp810mln), $1.2440-50(Gbp907mln)

- EUR/GBP: Gbp0.8740-50(E497mln)

Late Equity Roundup: IT Takes Lead, Financials Pressured

Major indexes remain mixed in late session trade, Dow shares underperforming. Earlier risk-on move following Bbg story: "ECB Starts to Ponder Slower Hikes After Half Point in February" faded. SPX eminis currently trades -4.5 (-0.11%) at 4013.75; DJIA -349.83 (-1.02%) at 33951.76; Nasdaq +16.8 (0.2%) at 11095.16.

- SPX leading/lagging sectors: Information Technology takes the lead (+0.51%) several factors in play including improved chip supply chain headlines, Microsoft layoffs spur rebound. Next up: Real Estate (+0.38%), Energy (+0.40%) lead by hotel and resort REITs, and Consumer Discretionary (+0.24%) lead by automakers (TSLA +6.96%).

- Laggers: Materials (-0.85%), Communication Services (-0.75%) with telecoms lagging (LUMN -4.83%, VZ -2.08%). Next up: Industrials (-0.64%) and Financials (-0.47%) w/Banks weighing (BAC -1.5%, JPM -1.48%) following mixed earning sfor GS and MS.

- Dow Industrials Leaders/Laggers: McDonalds (MCD) +6.20 at 275.09, Chevron (CVX) +3.51 at 181.07, AAPL +1.20 at 135.96, MSFT +1.19 at 240.42. Laggers: Goldman Sachs (GS) hammered after earnings miss -24.15to 349.85, Travelers (TRV) -9.01 at 184.91, Honeywell (HON) -3.77 at 212.84.

E-MINI S&P (H3): Conditions Remain Bullish

- RES 4: 4194.25 High Sep 13

- RES 3: 4180.00 High Dec 13 and the bull trigger

- RES 2: 4090.75 High Dec 14

- RES 1: 4043.00 High Dec 15

- PRICE: 4012.75 @ 14:21 GMT Jan 17

- SUP 1: 3891.50 Low Jan 10

- SUP 2: 3788.50/78.45 Low Dec 22 / 61.8% of Oct 13-Dec 13 uptrend

- SUP 3: 3735.00 Low Nov 3

- SUP 4: 3670.00 76.4% retracement of the Oct 13 - Dec 13 uptrend

S&P E-Minis are trading at their recent highs. The contract has cleared resistance at the 50-day EMA and this has strengthened the short-term bullish condition. Price has also traded above the 4000.00 handle to open 4043.00 next, the Dec 15 high. Key support and the bear trigger has been defined at 3788.50, the Dec 22 low. A reversal lower and a break of this support would resume bearish activity.

COMMODITIES: WTI Nears Bull Trigger On China Re-Opening Demand

- WTI prices have increased for the eighth straight gain at settlement (yesterday not a full session with MLK day), buoyed by China re-opening demand hopes adding to broadly stronger than expected China data.

- Separately, Chevron’s CEO expects the US is likely to refill in SPR slowly, with drawdowns leaving it in a delicate situation, whilst ahead, weekly US inventory reports from API and EIA are released tomorrow and Thursday with a day’s delay.

- WTI is +1.0% from Friday’s settle at $80.65, off a high of $81.23 that came close to the bull trigger at $81.50 (Jan 3 high). The corrective bounce is still seen in play although to the downside sits support at $76.96 (20-day EMA).

- Brent is +2.2% from Monday at $86.30, clearing $85.59 (Jan 16 high) and coming close to key resistance at $87.00 (Jan 3 high) with its high of $86.77.

- Gold meanwhile slips -0.4% at $1908.2 on a mixed day for the USD and yields, further down from yesterday’s highs of almost $1929.03 but still comfortably above support at $1874.4 (Jan 12 low).

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/01/2023 | 0001/0001 | * |  | UK | XpertHR pay deals for whole economy |

| 18/01/2023 | 0700/0700 | *** | | UK | Consumer inflation report |

| 18/01/2023 | 0930/0930 | * | | UK | ONS House Price Index |

| 18/01/2023 | 1000/1100 | *** |  | EU | HICP (f) |

| 18/01/2023 | 1000/1100 | ** | | EU | Construction Production |

| 18/01/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 18/01/2023 | - |  | JP | Bank of Japan policy decision | |

| 18/01/2023 | 1330/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 18/01/2023 | 1330/0830 | *** | | US | PPI |

| 18/01/2023 | 1330/0830 | *** | | US | Retail Sales |

| 18/01/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 18/01/2023 | 1400/0900 | | US | Atlanta Fed's Raphael Bostic | |

| 18/01/2023 | 1415/0915 | *** | | US | Industrial Production |

| 18/01/2023 | 1500/1000 | * | | US | Business Inventories |

| 18/01/2023 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 18/01/2023 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 18/01/2023 | 1800/1300 | | US | Kansas City Fed's Esther George | |

| 18/01/2023 | 1900/1400 | | US | Fed Beige Book | |

| 18/01/2023 | 2015/1515 | | US | Philadelphia Fed's Pat Harker | |

| 18/01/2023 | 2100/1600 | ** | | US | TICS |

| 18/01/2023 | 2200/1700 | | US | Dallas Fed's Lorie Logan |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.