Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- Treasuries look to finish weaker after a stronger start Monday, late morning sell-off unexplained by flow or headline.

- Markets well behaved the day after President Biden ended his 2024 reelection plans, fully endorsing VP Harris.

- Treasury curves reversed early flattening to steeper profiles late Monday: 2s10s +1.119 at -26.503.

US Tsys Off Late Morning Lows, Curves Steeper

- Treasuries look to finish weaker after a firmer start Monday, rather subdued trade in the aftermath of President Biden's Sunday annc he would drop out of the 2024 presidential race.

- Treasury futures held a narrow range for much of the first half, gapped lower heading into the London close. Sell-stops were triggered, adding to the speed of the move as Sep'24 10Y futures breached initial technical support at 110-21.5 (20-day EMA) to 110-18.5 low. Focus turned next support at 110-08 (50-day EMA values).

- No obvious headline driver or block for the move, some desks cited incoming Treasury coupon supply (2s, 5s, 7s and 2Y FRN) or possibly some hedging of election risk that had not been addressed as soon as markets opened late Sunday.

- Another driver for the unexplained sell-off could be the ongoing theme were Tsys sell-off going into the London close and gradually reverse in the second half.

- Focus turns to Tuesday's Regional Fed and Existing Home Sales data, Tsy $70B 42D CMB Bill and $69B 2Y Note auctions.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00275 to 5.34950 (+0.01895 total last wk)

- 3M +0.00037 to 5.28336 (-0.00508 total last wk)

- 6M +0.00455 to 5.13923 (-0.03012 total last wk)

- 12M +0.02119 to 4.82145 (-0.06528 total last wk)

- Secured Overnight Financing Rate (SOFR): 5.34% (+0.00), volume: $1.992T

- Broad General Collateral Rate (BGCR): 5.32% (+0.00), volume: $791B

- Tri-Party General Collateral Rate (TGCR): 5.32% (+0.00), volume: $770B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $79B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $223B

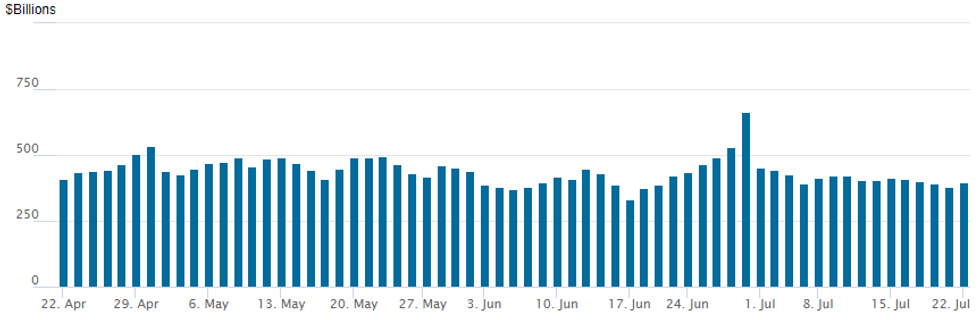

FED Reverse Repo Operation

RRP usage rebounds to $395.901B from $379.801B on Friday. Number of counterparties at 77 from 67 prior. Today's usage compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury options leaned towards better call structures as Monday progressed, fading the weaker price action in the underlying after futures extended lows around the London close. Projected rate cut pricing into year end has receded vs. early Monday levels (*): July'24 at -2.5% w/ cumulative at -0.6bp at 5.323%, Sep'24 cumulative -24.3bp (-25bp), Nov'24 cumulative -38.5bp (-39.5bp), Dec'24 -60.7bp (-62bp). Salient flow includes:- SOFR Options:

- +52,000 SFRH5 96.75/97.75 call spds 4.37 to 4.5

- +5,000 0QU4 96.25/96.50/96.75 call fly 3.5 ref 96.13

- +5,000 SFRU4 94.87/95.00 put spds 2x1 1.125 ref 94.915

- +7,500 SFRX4 95.06/95.18 2x1 put spds, 0.0

- -2,500 SFRZ4 94.87/95.12/95.50/95.75 iron condor 8.0 ref 95.29

- +10,000 SFRX4 95.31/95.43/95.56 call flys 1.625 ref 95.295

- +6,000 SFRZ4 95.25/95.37/96.00/97.00 call condors 2.25

- +4,000 SFRH5 95.00/95.25/95.50 put trees 5.0

- 5,500 SFRX4 95.12/95.25/95.31/95.43 call condors ref 95.30

- Block/screen, -9,000 SFRU4 94.87/95.00/95.12 call flys, 3.25

- -15,000 SFRV4 95.43/95.56 call spds, 30.5

- 1,250 0QZ4 96.50/96.75 call spds ref 96.28

- 1,000 0QV4 97.00/97.50 call spds ref 96.295

- 1,000 SFRQ4/SFRU4 94.93 call spds

- Treasury Options:

- 4,000 USU4 115/117 put spds ref 119-08

- 11,100 wk1 TY 111.25/112.25 call spds w/ TYQ4 111/111.5 call spds, 24 total

- 5,000 FVU4 107.75 calls, 22.5 last

- 1,400 FVQ4 107.75/108 call spds ref 107-10.25

- 3,000 TYU4 108.5/110.5 put spds vs. TYU4 113.5 calls ref 110-31.5

EGBs-GILTS CASH CLOSE: Gilts Underperform As Solid Start Fades

European curves closed Monday bear flatter, with Gilts underperforming Bunds.

- Core FI got off to a solid start, following an unanticipated rate cut overnight by the Chinese central bank.

- That gave way to weakness led by Treasuries as the session progressed, with some pointing to US political uncertainty after Pres Biden withdrew from the presidential election. European core FI yields closed near the highs.

- Gilts underperformed, in part due to new Chancellor Reeves' indications of above-inflation pay rises for UK public sector workers.

- Periphery spreads tightened, led by BTPs and GGBs, mirroring a strong bounce in equities.

- Tuesday's docket is limited, with an appearance by ECB Chief Economist Lane and preliminary Eurozone consumer confidence the highlights.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4.5bps at 2.829%, 5-Yr is up 3.9bps at 2.46%, 10-Yr is up 2.8bps at 2.495%, and 30-Yr is up 1.5bps at 2.679%.

- UK: The 2-Yr yield is up 6bps at 4.063%, 5-Yr is up 5.2bps at 3.98%, 10-Yr is up 3.8bps at 4.161%, and 30-Yr is up 3.3bps at 4.669%.

- Italian BTP spread down 3.3bps at 127.9bps / Greek down 2.9bps at 95.4bps

EGB Options: Euribor Call Structure Selling Monday

Monday's Europe rates/bond options flow included:

- ERZ4 96.75/97.125 1x2 call spread, paper sells for 4.5 in 5k

- ERZ4 97.75 call, paper sells at 0.75 in 15k

Late Equity Roundup: Semiconductor Makers Leads Monday Rebound

- Stocks are firmer late Monday, still off last week's cycle highs amid generally optimistic trade after President Biden's Sunday afternoon annc to drop out of the 2024 presidential race. Currently, the DJIA is up 134.38 points (0.33%) at 40424.83, S&P E-Minis up 60.25 points (1.08%) at 5613.75, Nasdaq up 305 points (1.7%) at 18031.17.

- Information Technology and Communication Services sectors continued to outperform in late trade, semiconductor makers supporting the IT sector following Friday losses tied to CrowdStrike outages: KLA Corp +5.81%, Lam Research +5.64%%, ON Semiconductor +5.43%. Incidentally, CrowdStrike lost another 12.88% in late session trade.

- Communication Services were buoyed by interactive media and entertainment shares: Netflix +3.25%, Electronic Arts +2.68%, Google +2.63. Conversely, weaker telecom stocks leavened Comm Services gains with Verizon -6.34% after reporting flat earnings, AT&T -2.8%.

- Meanwhile, Energy and Consumer Staples sector shares underperformed in the second half, oil and gas shares weighing on the former: Occidental -2.57%, Halliburton -2.11%, Devon Energy -2.01%. Meanwhile, food and beverage shares weighed on the Consumer Staples sector: Hormel -1.70%, Monster Beverage -1.51%, JM Smucker -1.47%.

- Reminder, Monday afternoon earnings announcements from Nucor Corp, W R Berkley, Alexandria Real Estate, Crown Holdings and Cadence Design Systems.

COMMODITIES: Crude Falls, Bearish Corrective Cycle In Copper Persists

- Crude is heading for the US close trading lower today as markets take stock of possible US rate cuts and weaker Chinese economic data.

- WTI Aug 24 is down 0.6% at $79.7/bbl.

- China imports of crude oil from Russia and Saudi Arabia fell in June but shipments from Malaysia were up near record levels, according to General Administration of Customs data released over the weekend.

- For WTI futures, the 50-day EMA gave way during the sell-off late last week, opening the potential for further losses toward $76.95, the June 13 low.

- Spot gold is currently 0.3% lower at $2,394/oz, although it has bounced off its intra-day low around $2,384.

- The yellow metal has now pulled back by 3.6% from its record high set last week.

- The trend condition in gold remains bullish, despite the fade off last-week highs, with initial resistance at $2,483.8, the July 17 high. Initial support is at $2,390.1, the 20-day EMA.

- Meanwhile, copper has slipped by another 1.0% to $420/lb.

- Copper is now more than 10.5% below its July 5 high, having hit an intra-day low of $416 earlier in the day, its lowest level since April 3.

- The bearish corrective cycle in copper futures persists with price now piercing $426.12, a Fibonacci retracement. Key support is at $402.35, the March 27 low.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/07/2024 | 0700/0900 |  | EU | ECB's Lane at ECB/IMF conference in Frankfurt | |

| 23/07/2024 | 0900/1000 | * |  | UK | Index Linked Gilt Outright Auction Result |

| 23/07/2024 | 1100/0700 | *** |  | TR | Turkey Benchmark Rate |

| 23/07/2024 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 23/07/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 23/07/2024 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 23/07/2024 | 1400/1000 | *** | | US | NAR existing home sales |

| 23/07/2024 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 23/07/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 23/07/2024 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

| 24/07/2024 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok