Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI BOC: HIKES RATE TO 4.75%, ASSESSING IF IT’S DONE ENOUGH

- MNI BOC: CONCERNED CPI COULD GET STUCK MATERIALLY ABOVE 2%

- MNI NATO: Secretary General Stoltenberg To Visit White House June 12

- MNI US-INDIA: Biden's National Security Advisor To Travel To India Next Week

- MNI US: JP Morgan Chase's Dimon Tells Democrats Debt Ceiling Should Be Abolished

Key Links: MNI BOC WATCH: Surprise 25BP Hike And Assessing If More Needed / MNI INTERVIEW: BOC Hike Is A Precursor For More- Ex Adviser

US TSYS Markets Roundup: Yields Gaining, Post BOC, Bill Supply Guidance

- Treasury yields have climbed to the highest levels since just prior to the debt ceiling passing Congress. Currently marking the highest level for June so far, 10Y yield is up to 3.7991% high in the aftermath of the Bank of Canada's surprise decision to hike 25bp to 4.75%, while signaling it’s prepared to go further with a strong economy threatening to leave inflation stuck well above its 2% target.

- A second, and well telegraphed factor weighing on the short end after the Tsy provided "additional guidance on bill issuance and cash balance" following the suspension of the debt limit through Jan 1 2025: plans to increase issuance of bills "to continue financing the government and to gradually rebuild the cash balance over time to a level more consistent with Treasury’s cash balance policy." Other highlights of the release:

- The knock-on effect has seen projected rate hike gain momentum in July or Sep (21.9bp and 19.1bp cumulative respectively) while chances of a June hike remains subdued around 20%.

- Broad based selling has gained in the long end, however, as Treasury curves climb off deeper inverted levels: 2s10s currently +4.755 a t -77.512 vs. -86.218 low from this morning.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00725 to 5.13117 (-.01000/wk)

- 3M -0.00076 to 5.23808 (+.00774/wk)

- 6M +0.00093 to 5.27788 (+.03241/wk)

- 12M +0.00902 to 5.10379 (+.07682/wk)

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00257 to 5.06614%

- 1M -0.01943 to 5.18171%

- 3M -0.00343 to 5.50986 */**

- 6M -0.00100 to 5.64357%

- 12M +0.00215 to 5.74629%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.51671% on 5/31/23

- Daily Effective Fed Funds Rate: 5.08% volume: $144B

- Daily Overnight Bank Funding Rate: 5.07% volume: $307B

- Secured Overnight Financing Rate (SOFR): 5.05%, $1.414T

- Broad General Collateral Rate (BGCR): 5.03%, $604B

- Tri-Party General Collateral Rate (TGCR): 5.03%, $594B

- (rate, volume levels reflect prior session)

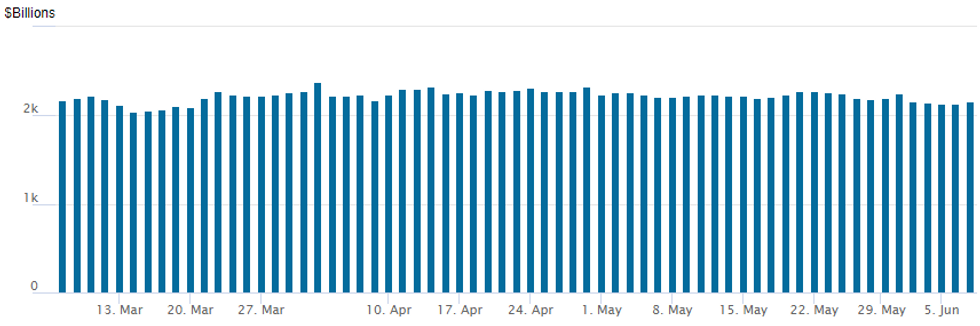

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,161.556B w/ 108 counterparties, compared to $2,134.638B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

Fading the sell-off in underlying futures Wednesday, SOFR option accounts looked to hedge softer policy in the near term as a projected 25bp rate hike in Jul or Sep gained momentum. Chances of a hike gained as well, but to a lesser degree on the day, nevertheless, paper bought over 33,000 Jun'23 SOFR 94.81/94.87 call spreads at 1.0 on the day (June options expire two days after the FOMC annc). Certainly more airtime in the approximately 45,000 Dec'23 SOFR 96.00/97.00 call spds bought from 10.0-10.5 with underlying futures at 95.00.- SOFR Options:

- over +45,000 SFRZ3 96.00/97.00 call spreads 10.00-10.5

- Block, 9,750 SFRM3 94.56/94.68/94.75 broken put flys, 1.75 ref 94.725

- 1,000 SFRM3 94.62/94.68/94.75/94.81 put condors ref 94.7325

- 33,000 SFRM3 94.81/94.87 call spds, 1.0 ref 94.7475

- Block/screen, 5,000 SFRU3 94.25/94.50 put spds, 4.5 ref 94.79

- Block, 5,000 SFRM3 94.87/94.93 call spds, 0.5 vs. 94.76/0.08%

- 3k SFRZ 96.25 and 96.75 calls vs. 1,500 SFRZ3 97.00 and 97.50 calls, Checking

- 1,000 SFRZ3 94.62/96.00 strangles ref 95.05

- 2,000 SFRN3 94.93 calls ref 94.79

- 2,000 SFRQ3 93.12 puts, .5 ref 94.80

- 1,500 SFRH3 94.50/94.75 put spds ref 95.475

- 3,650 SFRM3 94.75/94.81/94.87 put flys, ref 94.75

- 1,500 SFRM3 94.50/94.68 call spds, ref 94.75

- Treasury Options:

- 2,500 FVQ3 109.5/110.5/111 broken call flys ref 108-05.25

- 2,000 FVQ3 110/112 1x3 call spds ref 108-05.25

- +15,000 TYU3 110 puts, 32 vs. 113-05/0.21%

- -12,600 FVQ3 110 calls, 15-15.4 ref 108-04.5 to -03.75

- 3,000 FVN3 107/108

- 2,000 TYN3 110/111.5 put spds, 5 ref 113-14

- 3,000 TYQ3 111/112.5 put spds, 23 ref 113-15.5

- 2,500 TYN3 112.5 puts, 20 ref 113-14.5

- 3,600 TYN3 111/112 put spds, 6 ref 113-22.5

- over 4,000 TYQ3 114 calls, 104 last

EGBs-GILTS CASH CLOSE: Sharply Weaker On Supply And BoC Surprise

Large supply weighed heavily on EGBs Wednesday morning, with losses accelerating in the afternoon after a Bank of Canada rate hike that wasn't fully expected.

- With core euro FI already on the back foot in the face of heavy corporate issuance and large sovereign supply (including E13B in Spain 10Y syndication), the BoC move delivered another blow, triggering weakness in Treasuries that transmitted across the Atlantic.

- The BoC's hawkishness boosted the implied cumulative hiking priced for the ECB and BoE by 3bp / 7bp respectively, to fresh June highs. The German and UK curve bellies underperformed slightly in the aftermath.

- While Spain's large issuance was a key talking point, BTPs underperformed, with spread widening

- The session's data was on the weak side (German industrial production, Italy retail sales), but didn't have any lasting impact. Nor did commentary by Schnabel, Makhlouf or Knot alter any ECB rate expectations.

- Ireland rounds out the week's Euro sovereign supply Thursday, while we also get Eurozone final Q1 GDP data.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

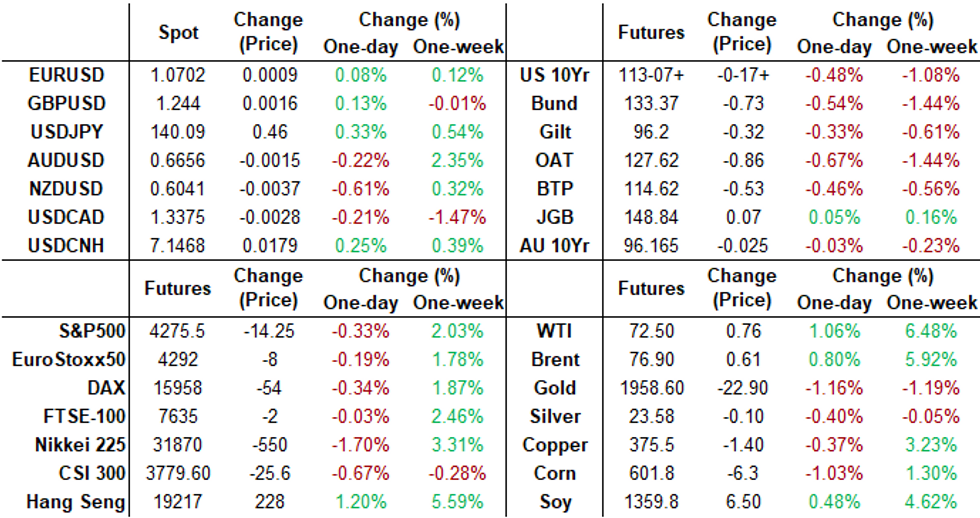

- Germany: The 2-Yr yield is up 8.4bps at 2.938%, 5-Yr is up 9bps at 2.474%, 10-Yr is up 8.4bps at 2.456%, and 30-Yr is up 4.9bps at 2.604%.

- UK: The 2-Yr yield is up 9.4bps at 4.572%, 5-Yr is up 7.2bps at 4.256%, 10-Yr is up 4.4bps at 4.251%, and 30-Yr is up 2.8bps at 4.501%.

- Italian BTP spread up 4.3bps at 182.7bps/ Spanish up 1.8bps at 101.7bps

EGB Options: Large Delta-Hedged Put Fly Highlights Quiet Trade Wednesday

Wednesday's Europe rates / bond options flow included:

- ERM4 96.62/96.1295.62,p fly, bought for 9.5 in 20k vs 96.655

FOREX: USD Index Recovers Back To Unchanged, CAD Surge Short-Lived

- USDCAD was in focus on Wednesday as the bank of Canada surprised the market with a 25bp hike. USDCAD weakened into the decision and extended this move to print as low as 1.3322 in the immediate aftermath. However, the move was fairly short-lived as greenback strength throughout the US session stalled any downside momentum for the pair.

- Assisted by the BOC’s hawkishness, US yields climbed between 10-15bps across the curve at one point which buoyed the US dollar. After some initial weakness, the USD index rose around 0.5% to trade back to unchanged on the session.

- With yield differentials widening, the Japanese Yen has suffered with USDJPY rising as much as 120 pips from the lows to print 140.23 in late trade. Trend conditions in USDJPY remains bullish. Attention is on key resistance at the top of a bull channel, drawn from the Jan 16 low, which intersects at 141.11 today. A clear break of this level would reinforce a bullish theme and open 141.61, the Nov 23 2022 high. Key support to watch is 138.45, the 20-day EMA.

- Some renewed pressure on major global equity indices, the move higher in U.S. Tsy yields and the associated bounce for the greenback all led USD/CNH back towards the day’s highs with the pair printing a fresh year-to-date high of 7.1533 approaching the APAC crossover on Wednesday. A sustained break above 7.1500 might expose bull channel top resistance, currently located at CNH7.1665. It is worth noting that both domestic PPI and CPI data for May will cross on Friday.

- A very light global economic calendar on Thursday as all eyes remain focused on the US CPI print next week, which precedes the June FOMC decision.

FX Expiries for Jun08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0650(E1.3bln), $1.0690-00(E2.6bln), $1.0800(E1.0bln)

- USD/JPY: Y140.00($2.9bln)

- AUD/USD: $0.6650-55(A$538mln), $0.6710-15(A$532mln)

- USD/CAD: C$1.3350($716mln), C$1.3400($860mln)

Equities Roundup: Energy Sector Gains After Crude Inventory Draw

- Stocks are trading mixed, reversing the prior session's moves with Dow components outperforming weaker SPX and Nasdaq stocks late Wednesday.

- DJIA had a rocky climb to 33671.72 -- up 97.99 points (0.29%), while SPX trades down 12 points (-0.28%) at 4277.75, Nasdaq down 134.6 points (-1%) at 13143.02.

- Leading gainers: Energy sector lead by a broad based support in drillers, refiners and distributors as crude inventories showed a small draw vs the market expectation of a small build driven by a large increase in refinery utilization and drop in imports. Utilities followed, supported by independent power and renewable energy shares.

- Laggers: Reversing prior session gains, Communication Services, Information Technology and Consumer Discretionary sectors underperformed, the latter despite automakers trading strong (Ford +4.5%, GM +2.75%).

- For a technical perspective, S&P E-minis are in a consolidation mode but the trend condition is bullish following recent gains. Resistance at 4244.00, Feb 2 high and a bull trigger, has recently been cleared. The break reinforces bullish conditions and confirms a resumption of the uptrend that started in October 2022. The focus is on 4327.50 next, the Aug 16 2022 high (cont). The 50-day EMA, at 4155.00 remains a key support. A break is required to signal a reversal.

E-MINI S&P TECHS: (M3) Outlook Remains Bullish

- RES 4: 4400.00 Round number resistance

- RES 3: 4393.25 High Apr 22 2022 (cont)

- RES 2: 4327.50 High Aug 16 2022 (cont)

- RES 1: 4305.75 High Jun 5

- PRICE: 4278.00 @ 1500 ET Jun 9

- SUP 1: 4229.00 Low Jun 2

- SUP 2: 4202.64 20-day EMA

- SUP 3: 4155.00 50-day EMA

- SUP 4: 4144.00 Low May 24 and a key support

S&P E-minis are in a consolidation mode but the trend condition is bullish following recent gains. Resistance at 4244.00, Feb 2 high and a bull trigger, has recently been cleared. The break reinforces bullish conditions and confirms a resumption of the uptrend that started in October 2022. The focus is on 4327.50 next, the Aug 16 2022 high (cont). The 50-day EMA, at 4155.00 remains a key support. A break is required to signal a reversal.

COMMODITIES: Crude Oil Holds Onto Pre-EIA Gains, Gold Slides Post BoC

- Crude oil has held onto the day’s earlier gains as OPEC production cuts for 2024 support the curve backwardation, despite Treasury yields and the USD climbing in spillover from the BoC hiking after a pause.

- EIA weekly data showed US crude production climbing to the highest since April 2020 (12.4mbpd, breaking out of the 12.2-12.3mbpd range since the start of the year), but it was countered by crude inventories showing a small draw vs the market expectation of a small build driven by a large increase in refinery utilisation and drop in imports.

- WTI is +1.1% at $72.55 but remains off resistance at the key short-term $75.06 (Jun 5 high). In signs of further but limited optimism, most active strikes in the CLN3 were seen at $75/bbl calls.

- Brent is +0.9% at $76.96 but remains off the short-term bull trigger at $78.73 (Jun 5 high).

- Gold is -1.1% at $1942.14, weighed down by the aforementioned macro forces post-BoC. It sees the yellow metal move closer but not yet test support at $1932.2 (May 31 low).

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/06/2023 | 2350/0850 | ** |  | JP | GDP (r) |

| 08/06/2023 | 0001/0101 | ** |  | UK | IHS Markit/REC Jobs Report |

| 08/06/2023 | 0130/1130 | ** |  | AU | Trade Balance |

| 08/06/2023 | 0900/1100 | *** |  | EU | GDP (final) |

| 08/06/2023 | 0900/1100 | * | | EU | Employment |

| 08/06/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 08/06/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 08/06/2023 | 1400/1000 | ** | | US | Wholesale Trade |

| 08/06/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 08/06/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 08/06/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 08/06/2023 | 1920/1520 |  | CA | BOC Deputy Beadury speech |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.