Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

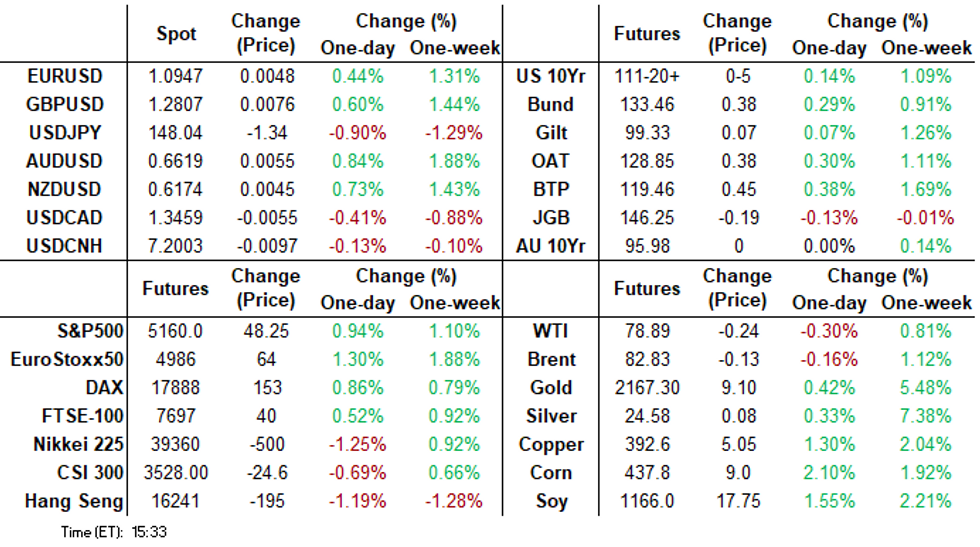

Treasuries inched higher late Thursday, position squaring ahead of Friday morning's February jobs report.

Markets will also be tuning into President Biden's State of the Union Address tonight at 2100ET.

No new insight from Chairman Powell today as he repeated his policy testimony to Congress.

Stocks climbed to new record highs (S&P Eminis 5170.50), led by chip stocks again.

US TSYS Yields Recede on Late Positioning Ahead Friday's Feb Employ Data

- Tsy futures are climbing off a lower, narrow range over the last hour - TYM4 near middle of the range at 111-20 (+4.5) vs. 111-27 high.

- Late support not headline driven - more flow driven as accts square up ahead tomorrow's Feb employ report, with trading desks reporting some renewed real$ buying in 30s. Note, however, curves remain steeper (2s10s +3.023 at -42.136).

- Tsys rallied through technical resistance this morning after lower than expected Unit Labor Costs (0.4% vs. 0.7% est). Weekly jobless claims largely in line: (216k vs. 217k est) while Continuing Claims rise (1.906M vs. 1.880M est; prior down-revised to 1.898M from 1.905M)). Additional data: Nonfarm Productivity (3.2% vs. 3.1% est); Trade Balance (-$67.4B vs. -$63.5B est).

- No new insight from Fed Chairman Powell today as he repeated yesterday's policy testimony to Congress.

- Later this evening: President Biden's State of the Union Address at 2100ET.

- Friday Data Calendar: February Employment Report.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00212 to 5.31771 (-0.00491/wk)

- 3M -0.00332 to 5.32122 (-0.00980/wk)

- 6M -0.01017 to 5.23565 (-0.03166/wk)

- 12M -0.01664 to 4.99749 (-0.05905/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.707T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $681B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $671B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $99B

- Daily Overnight Bank Funding Rate: 5.31% (-0.01), volume: $273B

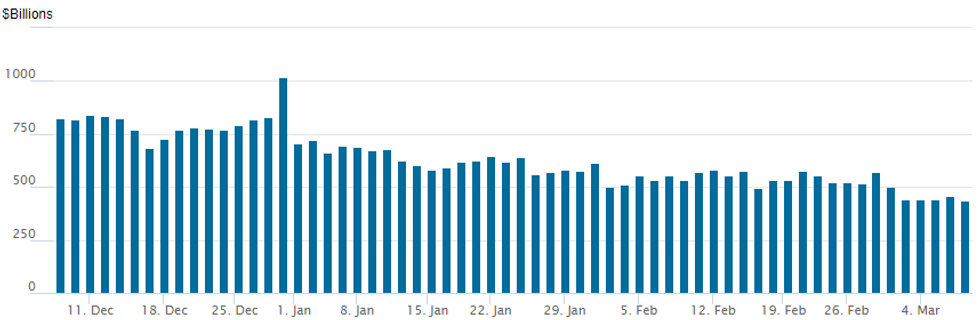

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage falls to new lowest level since May 2021 today: $436,754B from $456.847B Wednesday. Today's usage compares to Monday's low of $439.793B.

- Meanwhile, the latest number of counterparties climbs to 72 from 68 Wednesday (compares to 65 on January 16, the lowest since July 7, 2021).

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury options traded mixed on net Thursday, paired between calls and puts as underlying futures see-sawed mildly higher in narrow range. While Federal Reserve Chairman Powell's testimony to congress a repeat of Wednesday, many clung to the sidelines ahead Friday's February employment report.

- In turn - projected rate cut pricing held steady in the near term to slightly higher again vs. morning highs: March 2024 chance of 25bp rate cut currently -5.4% w/ cumulative of -1.4bp at 5.318%; May 2024 at -22.7% vs. -18.6% this morning w/ cumulative -7bp at 5.261%; June 2024 -68% from -65.5% earlier w/ cumulative cut -24bp at 5.091%. July'24 cumulative -39.4bp vs. -36.8bp at 4.938%.

- SOFR Options:

- +24,000 SFRM4 94.81/94.93/95.06 call flys, 3.5 ref 94.95

- Block, 5,000 SFRU5/0QU4 96.25 straddle spds, 46.0 net/long Red Sep'25 over

- Block, 5,000 SFRM4 95.62/95.87 call spds 1.0 vs. 94.97/0.05%

- Block, 5,000 SFRM4 94.81/94.93 put spds 1.5 over SFRU4 94.87/95.00 put spds

- Block, 5,000 0QZ4/2QZ4 97.50/97.87 call spd spds 1.0, short Dec over

- +10,000 0QH4 95.62/95.81 put spd, 4.75 vs. 95.91/0.25%

- +12,000 0QH4 96.00 calls, 7.0 vs. 95.905/0.38%

- -5,000 SFRU4 95.37/96.00 1x2 call spds, 0.5

- -4,000 2QH4 96.37 puts, 4.5 vs. 96.485/0.32%

- +10,000 SRU4 96.00 calls 11.5 ref 95.26

- -4,000 SRU5 96.00 puts 47.5 vs. 96.31/0.40%

- +5,000 SRM5 95.12/95.62/96.12 put trees .5 ref 96.16

- +12,000 0QH4 96.25 calls 2.0 ref 95.905

- 3,000 SFRM4 94.56/94.75 put spds ref 94.92

- Block, +5,000 SFRM4 95.62/95.87 call spds, 1.0 vs. 94.94/0.05%

- +5,000 SFRJ4 95.37/95.75 call spds, 0.75 vs. 94.93/0.07%

- 1,500 SFRM4 96.00/96.50 call spds

- Treasury Options:

- 7,000 FVK4 100/101/102/103 put condors ref 107-18.25

- 8,000 TYK4 111/111.5/113 broken call flys, 121 ref 111-17.5

- 10,000 TYJ4 111.5/112.5 call spds, 27 ref 111-17

- +9,000 TYK4 111 puts, 55

- 3,000 wk2 FV 107.75/108 call spds, ref 107-17.25 (expire Friday)

- 2,850 wk2 TY 111/112.5 put over risk reversals ref 111-15.5/0.43% (expires Friday)

FOREX Greenback Weakness Extends Ahead of February Employment Data

- Another more volatile session across G10 FX on Thursday culminates in the USD index extending its short-term weakening trend, down a further 0.4% on the day and breaching the February lows. Price action may have been spurred on by a partially dovish read of Powell's comment that the Fed is “not far from confidence needed to cut rates" and partially on the poorer-than-expected weekly jobless claims. Moreover, the short-term path of least resistance appears lower for the USD, with some pre-positioning ahead of tomorrow's NFP potentially in play.

- Alongside the ECB rate decision, a minor downtick for inflation forecasts prompted a very brief selloff for EURUSD, however, a more cautious Lagarde spurred a solid turnaround. EURUSD swiftly recovered back above 1.09 and the greenback weakness assisted the pair higher to 1.0940 as we approach the APAC crossover.

- Notably, EUR crosses remain lower on the session, with the outperformance of AUD and NZD this week extending amid the solid recovery for major equity benchmarks. EURAUD in particular traded as low as 1.6441, briefly expanding the pullback from the week’s highs to 1.8% in the direct aftermath of the ECB decision.

- In similar vein, EURJPY remains half a percent lower, mainly due to the developments in Japan overnight which keep the Japanese Yen as the strongest performer on Thursday. As a reminder, stronger Jan wages data, and a large union announcing larger pay increases this year appears to be supporting calls for a potential exit of negative interest rate policy as early as this month.

- USDJPY tracks closely to 148.00, however, the pair did trade as low as 147.59. The pair has breached the 20-day EMA and is through support at the 50-day EMA - at 148.54. The clear break of this average strengthens the current bearish cycle, potentially signalling scope for a move towards 146.83, a Fibonacci retracement.

- Focus turns immediately to the US employment report, where Bloomberg consensus sees nonfarm payrolls growth of 200k in February but two-month revisions will likely be watched particularly closely. Canadian employment data will also cross.

FX Expiries for Mar08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0700(E1.3bln), $1.0750(E782mln), $1.0770(E1.1bln), $1.0800(E1.4bln), $1.0820-35(E2.1bln), $1.0850(E501mln), $1.0900(E778mln)

- USD/JPY: Y146.90-00($1.1bln)

- GBP/USD: $1.2550-80(Gbp951mln)

- USD/CAD: C$1.3500($742mln), C$1.3590-00($1.2bln)

- USD/CNY: Cny7.1000($650mln)

Late Equities Roundup: Eminis Maintain Trajectory to New Highs

- Stocks continue to march higher in late Thursday trade, S&P Eminis making new all time highs with Communication Services and Information Technology sectors outperforming. Currently, DJIA is up 208.79 points (0.54%) at 38870.46, S&P E-Minis up 57.25 points (1.12%) at 5169, Nasdaq up 269.8 points (1.7%) at 16301.51.

- Communication Services and Information Technology sectors continued to lead gainers in the second half: media and entertainment shares buoyed the former: Paramount +4.13%, Meta +3.70%, Warner Brothers +3.15%. Continued AI demand for high end chips supported IT: ON Semiconductor +9.51%, Microchip Technology +7.06%, Qualcomm +5.13% while Intel, Micron and Nvidia all gained 3.55-3.65%.

- Laggers: Financials and Real Estate sectors underperformed in the first half, banks underperforming insurers late: Truist Financial and JPM both -0.97%, Huntington Bancshares -0.26%. On the flipside: Regions Financial +1.24%, Comerica +1.05%. After halting twice Wednesday, NY Community Bancorp trades +6.07% today after securing over $1B from a consortium of investors that included "LIBERTY STRATEGIC, HUSDON BAY and REVERENCE", Bbg.

- Meanwhile, estate management and retail REITS shares weighed in the Real Estate sector: CoStar Group -1.78%, Simon Property Group -2.04%.

E-MINI S&P TECHS: (H4) Trend Signals Point North

- RES 4: 5193.61 3.0% Bollinger Band

- RES 3: 5172.19 2.0% 10-dma envelope

- RES 2: 5170.86 2.236 proj of the Nov 10 - Dec 1 - 7 price swing

- RES 1: 5157.75 High Mar 1

- PRICE: 5141.50 @ 14:44 GMT Mar 7

- SUP 1: 5055.56 20-day EMA

- SUP 2: 4942.66 50-day EMA

- SUP 3: 4866.00 Low Jan 31 and key support

- SUP 4: 4808.50 Low Jan 19

The trend condition in S&P E-Minis remains bullish and the latest move lower appears to be a correction. Price action continues to highlight the fact that corrections are shallow - this is a bullish signal that highlights positive market sentiment. Support to watch is 5055.56, the 20-day EMA. A clear break of this average would signal potential for a deeper retracement towards 4942.66, the 50-day EMA. Sights are on 5170.86, a Fibonacci projection.

COMMODITIES A Fresh Record High For Gold With USD Tailwind

- Gold sits +0.5% at $2159.2 having earlier pushed onto fresh record highs of $2164.78 with further weakness for the USD index. Next resistance is seen at $2177.6 (Fibo proj of the Oct 6 – 27 – Nov 13 price swing)

- Crude oil markets meanwhile have erased earlier losses, with WTI now down only marginally on the day. The market is weighing a steep decline in the USD against higher non-OPEC+ supply and lacklustre Chinese demand growth.

- WTI is -0.2% at $78.96, although the trend needle points north with resistance at $80.85 (Mar 1 high).

- Brent is +0.05% at $82.99,also with a bullish structure and resistance seen at $84.34 (Mar 1 high).

- Kuwait Petroleum Corp is swapping cargoes with suppliers in order to avoid sailing via the Red Sea, KPC’s CEO Sheikh Nawaf Al-Sabah said, cited by Bloomberg.

- Transits via key waypoints Panama Canal and the Bab-el Mandeb strait remain low, disrupting the fluidity of tonnage and resulting in rerouting between markets according to Voretxa.

- G7-linked tankers, particularly Greek operators, shipped 1.1mbpd, or 33% of the total Russian seaborne crude exports in February, up from 1mbpd in January, Platts said.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/03/2024 | 0500/1400 |  | JP | Economy Watchers Survey | |

| 08/03/2024 | 0700/0800 | ** |  | DE | Industrial Production |

| 08/03/2024 | 0700/0800 | ** | | DE | PPI |

| 08/03/2024 | 0700/0800 | ** |  | SE | Private Sector Production m/m |

| 08/03/2024 | 0745/0845 | * |  | FR | Foreign Trade |

| 08/03/2024 | 0800/0900 | ** |  | ES | Industrial Production |

| 08/03/2024 | 0900/1000 | ** |  | IT | PPI |

| 08/03/2024 | 1000/1100 | *** |  | EU | GDP (final) |

| 08/03/2024 | 1000/1100 | * | | EU | Employment |

| 08/03/2024 | 1200/0700 |  | US | New York Fed's John Williams | |

| 08/03/2024 | 1330/0830 | *** |  | CA | Labour Force Survey |

| 08/03/2024 | 1330/0830 | *** | | US | Employment Report |

| 08/03/2024 | 1700/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 08/03/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.