Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- UK PRIME MINISTER LIZ TRUSS RESIGNs .. LEADERSHIP ELECTION EARLY NEXT WEEK

- US FED: Harker: Can Tighten Further After Pause If Necessary

- US NORTHEAST MAY FACE NATURAL GAS SHORTAGE THIS WINTER: FERC

- US WARNS RUSSIA MAY SOON BUY CONVENTIONAL MISSILES FROM IRAN, Bbg

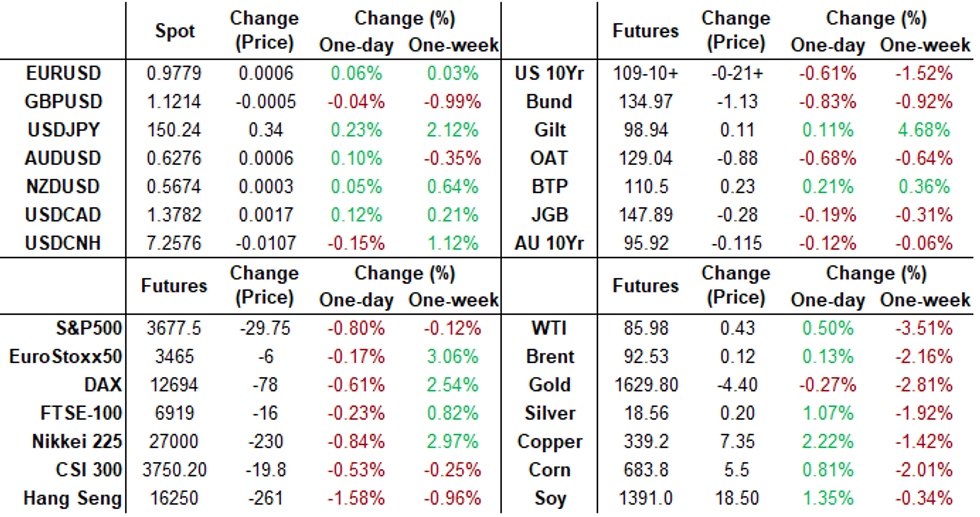

US TSYS: Ylds Continue to Extend Cycle Highs Into the Close

Tsy futures gradually extended session lows since briefly extended early session highs post-data: weekly claims -12k to 214k, continuing claims +.021M to 1.385M, Pilly Fed Mfg index little weaker than expected at -8.7.- U.S. existing home sales fell for an eighth straight month in September to a seasonally adjusted annual rate of 4.71 million, 1.5% lower than the previous month and down 24% compared to 2021 and a ten-year low as mortgage rates climbed, the National Association of Realtors said Thursday.

- Decent total volumes on the day (TYZ2>1.4M), Yield curves bear steepening (2s10s +4.315 at -38.606) as yields continue to extend cycle highs (10YY 4.2304%).

- Modest tail for US Tsy $21B 5Y TIPS auction (91282CFR7): 1.732% high yield vs. 1.725% WI.

- Eurodollar futures remain under heavy pressure, Reds through Golds (EDZ3-EDU7) -0.135-0.150 as markets price in two more 75bp hikes by year end, at least another 50bp to kick off 2023 w/ Fed terminal rate just over 5%.

- Reminder, Fed enters media blackout midnight Friday - yet only NY Fed Williams making open remarks at a careers event at 0910ET is scheduled.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00057 to 3.06114% (-0.00500/wk)

- 1M +0.07172 to 3.57243% (+0.12943/wk)

- 3M +0.04700 to 4.32457% (+0.13086/wk) * / **

- 6M +0.09443 to 4.83186% (+0.14657/wk)

- 12M +0.08171 to 5.42114% (+0.13800/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.32457% on 10/20/22

- Daily Effective Fed Funds Rate: 3.08% volume: $104B

- Daily Overnight Bank Funding Rate: 3.07% volume: $272B

- Secured Overnight Financing Rate (SOFR): 3.04%, $919B

- Broad General Collateral Rate (BGCR): 3.00%, $385B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $375B

- (rate, volume levels reflect prior session)

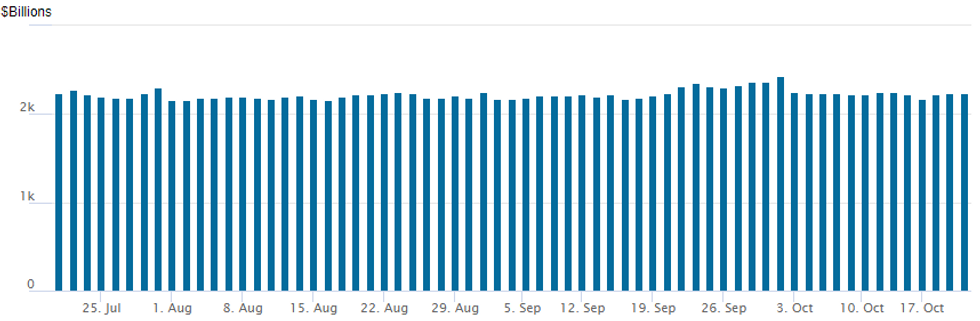

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage receded to $2,234.071B w/ 99 counterparties vs. $2,241.835B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Mixed low delta trade continued through the session, rate hike insurance buyers ongoing, early upside calls looking for a bounce in the underlying, particularly Dec expirys as futures price in two more 75bps hikes by year end - evaporated in the second half.- SOFR Options:

- +6,000 SFRF3 95.37/95.62 call spds, 4.75

- Block, 4,750 SFRX2 95.31/95.43/95.56 put flys, 2.5 - after fly crossed on 2x5x3 ratio earlier at 1.0

- Block, 1,666 x3 short Jun 95.25/95.50 put spds vs. 96.75/97.50 call spds on 3x4 ratio

- Block, 1,250 SFRZ2 95.31/95.43/95.56 2x5x3 call flys, 1.0 net/wings over

- Eurodollar Options:

- +10,000 Dec 94.87/95.12 call spds, 6.25 ref 94.835

- -20,000 EDH3 94.75/95.00 put spds, 15.0 ref 94.725-.73

- +10,000 EDZ2 97.00 calls, 18.0 vs. 95.07/0.12%

- +4,000 EDU4 98.00/99.00 1x2 call spds, 2.5

- +8,000 EDZ2 94.50 puts, 1.75 ref 94.84/0.08%

- Treasury Options:

- +3,000 TYX2 109.75 calls, 9 ref 109-14

- -5,000 TYZ 112.5 calls, 21 ref 109-16.5

- Block, 5,000 TYZ2 106/108 put spds, 26 ref 109-28.5, more on screen

EGBs-GILTS CASH CLOSE: PM Truss Quits, So Does Gilt Rally

Gilts rallied into UK PM Truss's 1330UK resignation announcement, but weakened thereafter as political risks were weighed up and global core FI pulled back. The UK curve twist flattened, and in Germany, the belly underperformed.

- After selling off on the open (China potentially easing Covid quarantine requirements for inbound travelers helped boost risk appetite), European yields headed lower over the course of the morning.

- Gilts in particular were boosted by BoE's Broadbent who said risks to market hike pricing were more to the downside. This depressed terminal rate expectations, and the Gilt rally gained steam as it became clear Truss would resign.

- But Bund and Gilt yields headed higher in the afternoon, no specific catalysts seen - largely regarded as fading the rally.

- MNI's Politics Team looks at what's next for the UK; attention after hours turns to the BoE's announcement for the pace and timing of active gilt sales in Q4 (see our expectations here).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: 2-Yr yield is up 2.6bps at 2.121%, 5-Yr is up 3.2bps at 2.245%, 10-Yr is up 2.8bps at 2.404%, and 30-Yr is up 2bps at 2.367%.

- UK: 2-Yr yield is up 8.2bps at 3.588%, 5-Yr is up 9.5bps at 3.967%, 10-Yr is up 3.5bps at 3.913%, and 30-Yr is down 2.9bps at 3.96%.

- Italian BTP spread down 4.7bps at 235bps / Spanish down 2.1bps at 112.9bps

EGB Options: Bund Call Spreads, Further Sonia Upside

Thursday's Europe rates / bond options flow included:

- RXZ2 144/146cs, bought for 15 in ~5.1k

- RXZ2 141/146cs bought for 57 in 10k vs 135.66

- SFIZ2 96.15/96.40cs, bought for 6.75 in 5k

FOREX

- USDJPY Clears 150 With Latest Push Higher From US Yields

- Rising US yields see USDJPY belatedly move higher, hitting new cycle highs of 150.248 in a firm clearance of 150 in the past half an hour, before a minor retreat to 150.17 latest.

- Next resistance seen 150.45 (3.618 proj of the Aug 2-8-11 price swing) having made light work of the psychological 150.

- The US 10YY is +8.0bp at 4.214% with real yields also climbing of late, +3.4bps on the day and with the associated drag on equities with ESA at session lows.

FX: Expiries for Oct21 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9595-00(E2.5bln), $0.9700(E2.0bln), $0.9725(E996mln), $0.9745-50(E997mln), $0.9770-75(E656mln), $0.9800(E1.8bln), $0.9845-50(E1.6bln)

- USD/JPY: Y147.50-55($1.1bln)

- AUD/USD: $0.6500(A$526mln)

- USD/CAD: C$1.3700-10($525mln), C$1.3750($675mln)

- USD/CNY: Cny7.1000($2.3bln), Cny7.2000($1.0bln)

Late Equity Roundup, Off Lows, Energy, Comms Outperforming

Major indexes still mildly weaker after the FI close, but making another attempt to move off lows w/ Energy, and Communication Services outperforming. Currently, SPX eminis trading -25.75 (-0.69%) at 3682.5; DJIA -54.67 (-0.18%) at 30372.65; Nasdaq -52.8 (-0.5%) at 10630.23.

- SPX leading/lagging sectors: Energy (+0.52%) outperforming lead by oil/gas drillers and servicers, Communication Services (+0.47%) next up lead by telecom names: ATT (T) +7.72% after this morning's Q3 earning beat: $0.68 vs $0.603 est. Laggers: Utilities -2.53% w/ electric and independent power names underperforming gas and water, Industrials (-1.71%) has transportation underperforming - road and rail lagging airlines.

- Dow Industrials Leaders/Laggers: IBM extends gains to +6.38 at 128.89 after narrow earnings beat late Wed($1.81 vs. $1.80 est), Salesforce.Com (CRM) +3.45 at 157.12, Boeing (BA) +0.963 at 139.35. Laggers: Home Depot (HD) -6.41 at 269.08, Travelers (TRV) -3.36 at 170.81, Caterpillar (CAT) -3.13 at 181.28.

E-MINI S&P (Z2): Corrective Bull Cycle Signals Scope For Gains

- RES 4: 4023.44 61.8% retracement of the Aug 16 - Oct 13 downleg

- RES 3: 3923.88 50.0% retracement of the Aug 16 - Oct 13 downleg

- RES 2: 3839.78 50-day EMA

- RES 1: 3820.00 High Oct 5 and a bull trigger

- PRICE: 3680.00 @ 1545ET Oct 20

- SUP 1: 3590.50/3502.00 Low Oct 17 / 13 and the bear trigger

- SUP 2: 3491.13 50.0% retracement of the 2020 - 2022 bull cycle

- SUP 3: 3453.78 1.618 proj of the Aug 16 - Sep 7 - 13 price swing

- SUP 4: 3388.70 1.764 proj of the Aug 16 - Sep 7 - 13 price swing

Despite the latest pullback, S&P E-Minis maintains a firmer tone following last week’s reversal from 3502.00, the Oct 13 low. The latest recovery suggests the contract has entered a corrective phase and if correct, this is allowing an oversold trend condition to unwind. The 20-day EMA has been breached. The break reinforces a bullish theme and opens 3820.00, the Oct 5 high and a bull trigger. Key support is unchanged at 3502.00.

COMMODITIES: A Tale Of Two Halves As Risk Sentiment Sours

- Crude oil and commodities more generally see a mixed session, with gains early on helped by China debating whether to reduce mandatory-quarantine periods for visitors before higher Treasury yields and a bounce in the US dollar put pressure on them.

- Colombian President Petro said oil, gas and coal producers can continue operating with their existing contracts, whilst refilling the US SPR at $67-72/bbl would see the US buying at a much lower rate than the >$85/bbl it’s sold it over the last five years.

- WTI is +0.5% at $85.95, clearing resistance at the 50-day EMA of $87.24 before retracing. Support is seen at at82.09 (Oct 18 low). By far the most active strikes in the CLZ2 today have been $100/bbl calls.

- Brent is +0.05% at $92.46 after coming close to resistance at $95.17 (Oct 12 high) before retracing. Support seen at $88.67 (61.8% retrace of Sep 26 – Oct 10 rally).

- Gold is -0.07% at $1628.3 but remains off the intraday low of $1622.5 after which lies the bear trigger of $1615.0 (Sep 28 low).

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/10/2022 | 2301/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 21/10/2022 | 0600/0700 | *** | | UK | Retail Sales |

| 21/10/2022 | 0600/0700 | *** | | UK | Public Sector Finances |

| 21/10/2022 | 0600/0800 | ** |  | SE | Unemployment |

| 21/10/2022 | 1230/0830 | ** |  | CA | Retail Trade |

| 21/10/2022 | 1310/0910 |  | US | New York Fed's John Williams | |

| 21/10/2022 | 1400/1600 | ** |  | EU | Consumer Confidence Indicator (p) |

| 21/10/2022 | 1600/1200 | ** | | US | Treasury Budget |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.