Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

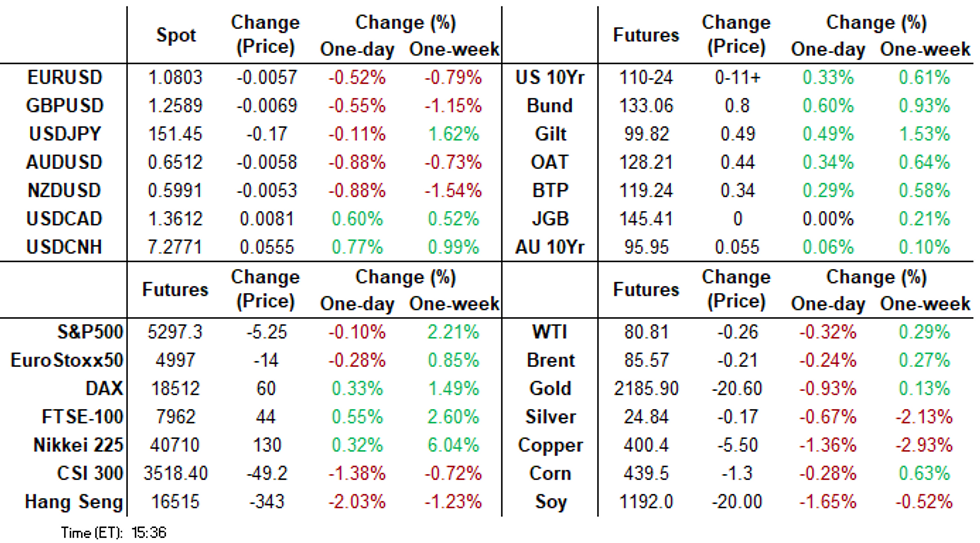

- Treasuries discounted yesterday's flash PMI inflation build, rates back near highs for the week.

- No headline or block driver, US and EU FI markets climb back near last week pre-PPI levels.

- Position squaring, risk unwinds apparent ahead of next week's shortened Easter Holiday schedule.

US TSYS Rates Discount Thursday's Data, Finish Week Near Highs

- Treasuries look to finish higher Friday, trading sideways after marking session highs around midmorning. No particular headline driver, rates see broad based support around midday following a large buy of 35,000 SFRM4 (3M Jun'24 SOFR futures) noted at 94.905 (+0.015) at around 1112ET, trades 94.915 last.

- After the bell, Jun'24 10Y futures trade +11.5 at 110-24 vs. 110-26.5 high. Key short-term resistance to watch is 111-00+, the 50-day EMA. A clear break of this average is required to suggest scope for a stronger recovery.

- Underlying futures discounted yesterday's flash PMI inflation build, trading back near highs for the week while projected rate cut pricing gained ground: May 2024 at -16.5 vs. -14.5% this morning w/ cumulative -4.1bp at 5.286%; June 2024 -69.3% vs. -64.1% earlier w/ cumulative rate cut -21.5bp at 5.113%. July'24 cumulative at -33.5bp vs. -31.5bp.

- Monday Data Calendar: Fed Speak, New Home Sales, Dallas Fed Mfg. Trading floors and Globex are closed next Friday for Good Friday/Easter holiday.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00070 to 5.32871 (-0.00004/wk)

- 3M -0.00748 to 5.31248 (-0.02000/wk)

- 6M -0.01678 to 5.22900 (-0.04614/wk)

- 12M -0.03306 to 5.00378 (-0.07481/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.849T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $684B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $678B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $93B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $248B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage rebounds to $478.531B from $460.631B yesterday. Last Friday saw usage fall to $413.877B - the lowest level since May 2021.

- Meanwhile, the latest number of counterparties slips to 72 vs. 74 yesterday (compares to 65 on January 16, the lowest since July 7, 2021)

SOFR/TEASURY OPTION SUMMARY

Treasury calls dominated Friday's trade volume, with some sporadic 5- and 10Y puts outlined below. Continued 10Y midcurve call trade has paper buying over 100,000 wk2 10Y 110.75 calls that expire on April 12, covering the next employment report on April 5, CPI on April 10 and PPI the day after. Meanwhile, underlying futures discounted yesterday's flash PMI inflation build, trading back near highs for the week while projected rate cut pricing gained ground: May 2024 at -16.5 vs. -14.5% this morning w/ cumulative -4.1bp at 5.286%; June 2024 -69.3% vs. -64.1% earlier w/ cumulative rate cut -21.5bp at 5.113%. July'24 cumulative at -33.5bp vs. -31.5bp.

- Treasury Options: (April options expire today)

- +20,000 FVK4 103.5 puts, 1

- +18,000 Wednesday weekly/wk 4 TY 112 calls, 1 ref 110-23

- Block, +12,000 Wednesday weekly/wk 4 TY 111.75 calls, 2 vs. 110-25

- 3,500 FVJ4 107 puts, 0.5 ref 107-04

- +10,000 TYM4 114.5 calls, 12

- +20,000 TYK4 114/114.5 call strip, 10 vs. 110-25.5/0.10%

- 4,500 TYM4 107.5/109 3x2 put spds ref 110-17.5 to -18

- 50,000 WK2 TY 110.75 calls, 37 vs. 110-18/0.45% (expire Apr 12)

- 15,000 TYK4 109.5/110.5 2x1 put spds, 1 ref 110-19

- -15,000 FVJ4 106.75/107.25 put spds, 21.5-15.5

- -5,000 TYK4 109.5 puts, 20 vs. 110-24.5/0.30%

- Over 5,500 TYJ4 110.5 puts, 4 last

- Over 5,200 TYK4 111 calls, 39 last

- SOFR Options:

- 2,000 SFRM4 94.75/94.81/97.87 put flys, ref 94.915

- -2,000 SFRZ4 94.50/94.75/95.00/95.25 put condors, 5.5 vs. 95.515/0.10%

- +5,000 SFRM4 95.25/95.75/96.25 call flys, 0.5

- +10,00 SFRU4 95.37 calls, 14.0 vs. 95.205/0.34%

- 2,000 0QM4 96.50/97.00 call spds ref 95.98

- 2,000 SFRK4 94.87/95.00 2x1 put spds

- 3,000 SFRK4 94.75 puts, 1.5 last

EGBs-GILTS CASH CLOSE: Further Gains To Cap Dovish Central Bank Week

Gilts and Bunds completed a strong week with a 5th consecutive session of gains Friday, as multiple dovish central bank developments buoyed global core FI.

- Though there were few market-moving developments on the day, Friday's positive tone was attributed to multiple dovish-leaning central bank results (BoJ, SNB, Fed, BoE) earlier in the week.

- The rally extended sharply around midday, with Bund yields' fall through the Mar 14 low of 2.355% rippling through to UK and US markets. From a futures perspective, Gilt tested but failed to break through psychological 100.00 level, with 99.91/100.37 remaining key S/T resistance.

- German IFO and UK retail sales data were each above-consensus, but didn't have much market impact. ECB/Bundesbank's Nagel said at an MNI event that "if I were to put it into probabilities - June has a higher probability than April" for the first ECB rate cut.

- Periphery EGB spreads closed wider. Note expected ratings reviews after hours Friday (Fitch on Portugal, Scope on Spain), against a backdrop of recent ratings upgrades (S&P on Portugal) helping periphery EGB spreads compress.

- Next week's highlights include the beginning of the March Eurozone flash inflation round (Spain, France, Italy).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 4.8bps at 2.827%, 5-Yr is down 7.1bps at 2.334%, 10-Yr is down 8.1bps at 2.324%, and 30-Yr is down 8.4bps at 2.494%.

- UK: The 2-Yr yield is down 5.4bps at 4.124%, 5-Yr is down 6.1bps at 3.817%, 10-Yr is down 6.5bps at 3.93%, and 30-Yr is down 4.6bps at 4.447%.

- Italian BTP spread up 4.9bps at 131.9bps / Portuguese PGB spread up 3.3bps at 66.9bps

EGB Options: Multiple Sonia Structures Friday

Friday's Europe rates/bond options flow included:

- SFIJ4 94.90/94.80ps, bought for 0.25 in 4k

- SFIK4 95.20/95.25cs, bought for 1 in 6k

- SFIM4 95.15/95.25/95.35/95.45c condor, sold at 1.25 in 8k total

- ERJ4 96.50/96.37ps vs ERM4 96.37/96.25ps, sold the April at 6 in 4k

- ERM4 96.50/96.75/97.00c fly, bought for 1.75 in 5k

FOREX Greenback Dominates Amid Global Dovish Repricing

- The greenback was among the strongest performers in G10 on Friday, and comfortably the best performer on the week amid a phase of global central bank re-pricing - particularly dovish shifts in Europe and the UK.

- Dollar strength put the USD Index back above 104.00 and within range of the mid-February multi-month highs. The USD Index is on track to form a key bullish indicator - a golden cross formation - at the close. The signal, formed when the 50-dma rises above the 200-dma, was last printed in September last year, and pre-saged a further 2% rally to the '23 high.

- A corrective pullback in GBP/USD persists, with the pair showing below the 200-dma on Friday, mirroring the build in BoE rate cut pricing since Thursday’s decision. Over 80bps of rate cuts are now priced for this calendar year, up from ~60bps at the beginning of the week. This narrows the gap with next support for GBP/USD undercuts at 1.2536, the Feb14 Low and the bear trigger at 1.2519.

- Focus in the coming week shifts away from global central banks, and is front-loaded with Good Friday keeping markets only partially open on March 29th. Nonetheless, key comms will be watched from BoE's Mann (who dropped her vote for a hike this week) and Fed's Waller on Wednesday.

FX Expiries for Mar25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0780-85(E1.0bln), $1.0850(E876mln), $1.0900(E705mln)

- USD/JPY: Y149.80-00($2.0bln)

- GBP/USD: $1.2716-25(Gbp645mln)

- AUD/USD: $0.6560-65(A$727mln)

- USD/CAD: C$1.3485-00($2.5bln), C$1.3700($658mln)

Late Equities Roundup: Communication, IT Sectors Outperform

- Stocks remain near steady to mixed late Friday, Dow shares still underperforming, S&P Eminis not far off Thursday's all-time high of 5322.75. Currently, S&P E-Minis trades down 1.75 points (-0.03%) at 5300.5, Nasdaq up 39.4 points (0.2%) at 16440.47, DJIA down 200.45 points (-0.5%) at 39580.63.

- Leading Gainers: Communication Services and Information Technology sectors continued to lead gainers in the second half, media and entertainment shares buoyed the former: Google +2.29%, Netflix +0.54%, Meta +0.3%. Semiconductor stocks supported IT: Nvidia +3.24%, Broadcom +1.17%, Micron +1.12%.

- Laggers: Real Estate and financial sectors underperformed in the the second half, Real Estate investment trusts and estate management shares weighed on the former: Boston Properties -3.57%, Kimco -3.0%, Alexandria Real Estate -2.32%. Meanwhile, Banks and services weighed on the Financial sector late: M&T Bank -2.38%, Synchrony Financial -2.32%, Blackstone -2.0% while KeyCorp traded -1.90%.

E-MINI S&P TECHS: (M4) Northbound

- RES 4: 5428.25 1.00 proj of the Oct 27 - Dec 28 - May 1 price swing

- RES 3: 5400.00 Round number resistance

- RES 2: 5379.92 Bull channel top drawn from the Jan 17 low

- RES 1: 5322.75 High Mar 21

- PRICE: 5302.00 @ 1500 ET Mar 22

- SUP 1: 5209.19 Bull channel base drawn from the Jan 17 low

- SUP 2: 5185.88 20-day EMA

- SUP 3: 5073.80 50-day EMA

- SUP 4: 5018.00 Low Feb 21

The trend condition in S&P E-Minis remains bullish and this week’s extension reinforces this theme. The break of 5257.25, Mar 8 high, confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. MA studies are in a bull-mode position reflecting positive market sentiment. Sights are on 5379.92, the top of a bull channel drawn from the Jan 17 low. Initial firm support is at 5196.99, the 20-day EMA.

COMMODITIES Stronger Dollar Weighs On Oil, Gold

- Crude prices are down on the day but are broadly flat on the week. Support has come from Mideast tensions and attacks on Russian oil refineries, although the upside has been capped by a stronger US dollar.

- WTI is down 0.5% on the day at $80.7/bbl.

- For WTI futures, the bull theme remains intact, with sights on $83.87 next, the Oct 20 ‘23 high. Support to watch is $79.27, the 20-day EMA.

- Henry Hub is also trading lower today but holding rangebound on the week, amid continued lower LNG feedgas flows and milder weather.

- US natural gas APR 24 is 1.9% lower on Friday at $1.65/mmbtu.

- Meanwhile, spot gold is down 0.9% on the day to $2,162/oz, leaving the yellow metal around 2.6% off the all-time high reached on the open Thursday. Over the week as a whole, gold is set for a marginal 0.3% gain.

- Copper also traded lower Friday, declining 1.3% to $400.6/lb, taking the loss over the week to 2.9%. Analysts note that seasonal demand in China is lagging, while the stronger dollar also weighed on the metal.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/03/2024 | 0800/0900 | ** |  | ES | PPI |

| 25/03/2024 | 1100/1100 | ** |  | UK | CBI Distributive Trades |

| 25/03/2024 | 1225/0825 |  | US | Atlanta Fed's Raphael Bostic | |

| 25/03/2024 | 1400/1000 | *** | | US | New Home Sales |

| 25/03/2024 | 1415/1415 | | UK | BOE Mann At Royal Economic Society Annual Conference | |

| 25/03/2024 | 1430/1030 | ** | | US | Dallas Fed manufacturing survey |

| 25/03/2024 | 1430/1030 | | US | Fed Governor Lisa Cook | |

| 25/03/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 25/03/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 25/03/2024 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.