Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

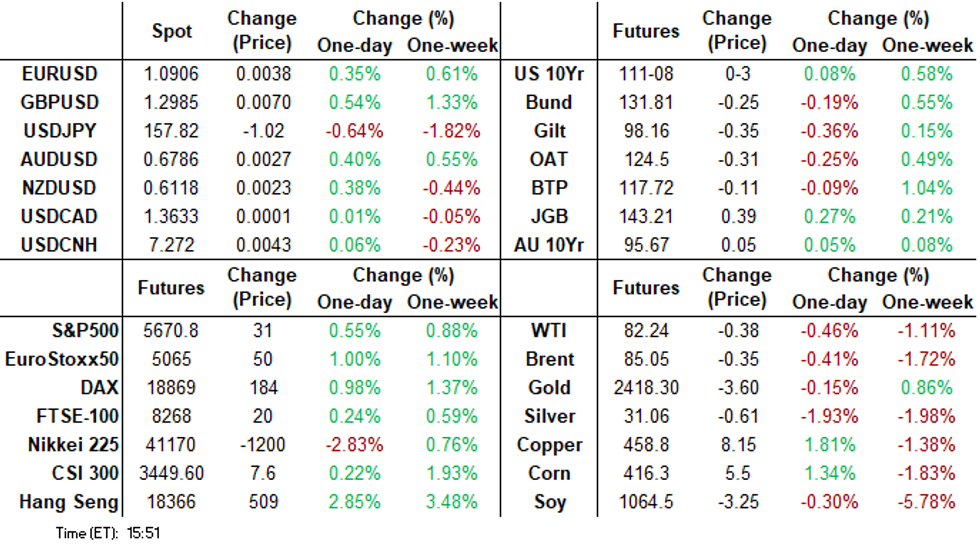

- Treasuries bounced off post-PPI data lows, mixed metrics and prior up-revisions deemed more mixed than the initial hawkish reaction warranted.

- PPI final demand: 0.22% M/M (cons 0.1) in June after -0.03 (revised up from initial -0.25), net upward revisions worth 0.18pps.

- The Treasury bull curve steepening that gained momentum into midday saw projected rate cut pricing into year end surpass Thursday's CPI-driven gains.

US TSYS Near Late Highs, Discounting June PPI & Up-Revisions

- Reversing the initial negative reaction to this morning's PPI data, Treasury futures look to finish mildly higher, at or near late session highs Friday as as economists deemed the data as more mixed than the initial hawkish reaction warranted.

- The Sep'24 10Y contract currently trades +2.5 at 111-07.5 near initial technical resistance is at 111-10+ (High Jul 8) followed by 111-13 (High Mar 25). Clearance of this hurdle would open 111-31, a Fibonacci projection. Curves are bull steepened with 2s10s +3.251 at -27.456, 5s30s +1.557 at 29.122.

- In turn, projected rate cut pricing into year end look firmer vs. early Friday (*): July'24 at -6.5% w/ cumulative at -1.6bp at 5.313%, Sep'24 cumulative -25.2bp (-24.1bp), Nov'24 cumulative -41.4bp (-38.5bp), Dec'24 -62.9bp (-59.6bp).

- Treasuries gapped lower after higher than expected PPI Final Demand MoM (0.2% vs. 0.1% est, with prior PPI up-revised to 0.0% from -0.2%), YoY (2.6% vs. 2.3% est, 2.2% prior).

- The Sep'24 10Y contract traded down to 110-25.5 low (-11.5), well above initial technical support of 110-07+/109-31 (20- and 50-day EMA values) before consolidating and reversing course.

- Futures inched higher after the latest UofM data came out near steady to lower than expected (current Conditions 64.1 vs. 66.0 - the lowest since late 2022) while inflation expectations come out in-line to slightly lower than expected with both 1Y and 5-10Y at 2.9%.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00100 to 5.32780 (+0.00037/wk)

- 3M -0.01526 to 5.28611 (-0.02078/wk)

- 6M -0.04028 to 5.16480 (-0.06167/wk)

- 12M -0.07906 to 4.86554 (-0.13995/wk)

- Secured Overnight Financing Rate (SOFR): 5.34% (+0.00), volume: $1.920T

- Broad General Collateral Rate (BGCR): 5.32% (-0.01), volume: $773B

- Tri-Party General Collateral Rate (TGCR): 5.32% (-0.01), volume: $755B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $90B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $270B

FED Reverse Repo Operation

NY Federal Reserve/MNI

RRP usage inches up to $406.590B from $403.708B on Thursday. Number of counterparties: 73 from 71 prior. Today's usage compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

SOFR/TEASURY OPTION SUMMARY

Heavier SOFR and Treasury option volume continued Friday, upside call skew still outbid puts as underlying futures quickly rebounded off morning lows. Projected rate cut pricing into year end look firmer vs. early Friday (*): July'24 at -6.5% w/ cumulative at -1.6bp at 5.313%, Sep'24 cumulative -25.2bp (-24.1bp), Nov'24 cumulative -41.4bp (-38.5bp), Dec'24 -62.9bp (-59.6bp). Salient flow includes:

- SOFR Options:

- -10,000 SFRU4 94.75/94.81 put spds .875 ref 94.94

- +10,000 SFRH5 94.87/95.50 put spds 15.5 vs. 95.695/0.26%

- -7,000 SFRZ4 94.25/94.62/95.00 put flys, 3.0 ref 95.32

- -5,000 SFRZ4 95.25/95.50 call spds 8.75 ref 95.33

- +5,000 0QU4 95.75 puts, 4.0 vs. 96.22/0.16%

- +5,000 0QU4 96.25/96.50/96.75 call flys 3.875 ref 95.20

- -6,000 SFRN4 94.93 calls, .5 ref 94.94

- -5,000 2QU4 96.25/96.50 call spds, 15.0 ref 96.51

- -5,000 2QU4 96.37/96.50 call spd with 2QU4 96.25/96.50 call spd strip 22.0

- Block/pit, -40,000 SFRZ4 95.50/96.25/97.00 call flys, 5.5 ref 95.33 to -.32

- -6,000 SFRU4 95.00/95.50 call spds, 3 ref 94.945

- -5,000 SFRX4 95.18 puts, 10.0 vs. 95.27/0.38%

- +5,000 SFRU4 94.87/94.93 put spds, 2.5 vs. 94.935/0.20%

- -12,000 2QQ4 96.25 puts, 4.0 vs. 96.53/.20%

- +6,000 SFRU4 94.62/94.75 put spds vs SFRZ4 94.62/94.75 put spds 0.25 net

- -4,000 SFRZ4 95.25/95.50 call spds, 8.5 ref 95.32

- +/-5,000 SFRN4 94.93 conversions

- 4,500 SFRZ4 95.25/95.31/95.37 call flys

- 13,000 SFRZ4 95.25/95.50 call spds ref 95.295 to -.30

- 3,500 0QN4 96.12/96.25 call spds ref 96.155

- 3,500 SFRV4 95.12/95.31 2x1 put spds ref 95.30

- 1,000 SFRN4 94.93/95.00 3x2 call spds ref 94.935

- Treasury Options:

- 12,000 TYQ4 111.5/112 2x3 call spds, 13 net ref 111-05

- +11,100 TYU4 108/113 strangles, 19 vs. 111-04/0.13%

- -2,000 TYU4 111 straddles, 140

- 2,300 TUQ4 102.25/102.5 call spds ref 102-15.12

- 1,300 TYU4 112/113.5/115 call flys ref 111-00.5

- 2,000 USU4 122124 call spds

- 15,000 TYQ4 111/111.5 call spds ref 110-31.5

- Block, -20,000 TYQ4 111.5 calls, 16-14 ref 110-31.5 to 111-00.5

EGBs-GILTS CASH CLOSE: Yields Partially Rebound From Thursday's Drop

European yields partially rebounded Friday from the prior session's US CPI-induced drop.

- Yields rose in early trade, amid small upward revisions in French and Spanish final June inflation data, and an uptick in oil prices.

- Pressure peaked in early afternoon after US producer price indices came in stronger than expected.

- But the move faded after PPI details looked less worrying, with the effect later compounded by soft US consumer sentiment data (UMichigan), helping European yields close toward the lower end of the daily range and well below the week's highs.

- Periphery spreads tightened modestly, led by BTPs, with equities rising sharply (Eurostoxx futures +1.3%). 10Y OAT/Bund spread closed flat on both the day and the week (65.6bp).

- Next week's risk events include UK CPI Wednesday, with the ECB decision Thursday - while there are no expectations of a rate cut, communications will be eyed for the outlook for September's expected easing.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3.1bps at 2.823%, 5-Yr is up 3.6bps at 2.475%, 10-Yr is up 3.3bps at 2.496%, and 30-Yr is up 2.5bps at 2.683%.

- UK: The 2-Yr yield is up 1.8bps at 4.086%, 5-Yr is up 2.6bps at 3.948%, 10-Yr is up 3.5bps at 4.109%, and 30-Yr is up 2.6bps at 4.615%.

- Italian BTP spread down 2.4bps at 129.7bps / Spanish down 0.5bps at 76.4bps

EGB Options: Friday Features Unwinding Of Bobl And Schatz Put Structures

Friday's Europe rates/bond options flow included:

- DUQ4 105.60/105.40/105.20p ladder sold at 5 in 2k

- DUQ4 105.60/105.40/105.20/105.00p condor sold at 5.5 in 2k

- DUU4 105.5/106.0/106.3/106.8c condor, sold at 18 in 5k total

- OEU4 116.25/115.50ps 1x2, sold at 15 in 7k vs 1.4k at 116.39 (liquidation)

- RXU4 135/138cs 1x1.5, bought the 1 for 10 in 5k

FOREX: Greenback Weakens Further, JPY & GBP Strength in Spotlight

- Higher-than-expected US PPI data did little to affect post-CPI sentiment in currency markets, and a subsequent bounce for major equity indices weighed on the greenback into the week’s close. The USD index sits 0.3%, set to post its lowest close in around five weeks.

- The Japanese Yen was once again in the spotlight, following the apparent confirmation that the BOJ intervened on Thursday, following the US inflation figures. Price action remained volatile in today’s session and another sudden jolt to the downside has prompted speculation that another round of intervention may have occurred.

- USDJPY resides 0.58% lower on the session around 157.90, having tested the pullback low at 157.38. This level has held well, suggesting decent support layered at the Thurs/Friday lows. The 50-dma has been pierced, but a close below the mark at 157.78 today would be the first since March of this year.

- For reference, according to a Bloomberg analysis of central bank accounts. Scale of intervention was probably around ¥3.5 trillion ($22 billion), based on a comparison of Bank of Japan accounts and money broker forecasts.

- GBP strength into the London close has helped GBPUSD (+0.56%) again print the best levels since mid-'23. On the weekly chart, a close at current levels would be the first above the 200-week moving average since the false break last year, and would open M/T targets at 1.3142 - the 76.4% retracement for the Jun'21 (post COVID high) - Sep'22 (Truss budget low) downleg.

- For EURGBP, weakness through the June low puts the cross at the lowest level since Aug'22. We note that this resumes the downtrend and places the immediate focus on 0.8366, the 2.236 projection of the Apr 23 - 30 - May 9 price swing.

- On Monday, Fed Chair Powell makes his final scheduled appearance ahead of the pre-July FOMC meeting communications blackout period. Elsewhere next week, CPI data from Canada, New Zealand and the UK is scheduled, with Thursday marking the ECB’s July decision.

OPTIONS: Expiries for Jul15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0750-60(E2.6bln), $1.0790-00(E1.2bln), $1.0825-30(E1.6bln), $1.0850-70(E1.6bln), $1.0895-15(E4.7bln), $1.0930(E582mln)

- USD/JPY: Y157.75($585mln), Y158.00($966mln), Y160.50($1.4bln)

- EUR/GBP: Gbp0.8450-60(E1.6bln)

- AUD/USD: $0.6645-55(A$1.1bln), $0.6750(A$599mln)

Late Equities Roundup: Strong Gains Around, DJIA Crush May Highs

- Despite briefly revisiting the lows for the week after this morning's data, stocks surged to new cycle highs as the PPI details were deemed more mixed than the initial hawkish reaction warranted.

- S&P Eminis marked a new high of 5,708.25, while the DJIA blew past the prior high of 40,065.18 set on May 20 to 40,244.94 in the second half. While the Nasdaq traded strong, the index was still off Thursday morning's cycle high of 18,661.46.

- Currently, the DJIA is up 444.46 points (1.12%) at 40198.6, S&P E-Minis up 62.75 points (1.11%) at 5703.25, Nasdaq up 252.7 points (1.4%) at 18538.42.

- Information Technology and Consumer Discretionary sectors continued to lead gainers in the second half, semiconductor makers recovering from Thursday's profit taking: Enphase +6.86%, ON Semiconductor +5.09%, Intel +4.93%, Monolithic Power +4.73%. Auto makers continued to buoy the Consumer Discretionary sector: Ford +5.09% outpacing Tesla +3.99%, while GM gained 2.61%.

- Conversely, Communication Services and Energy sectors continued to lag in late trade, interactive media and entertainment pared midweek support with Paramount -2.56%, Meta -1.79%, News Corp -0.54%. Oil & Gas shares weighed on the Energy sector: Diamondback Energy -1.46%, ConocoPhillips -0.61%, Marathon Petroleum -0.49%.

- Meanwhile, banks kicked off the latest earnings cycle this morning, mixed results for Wells Fargo -6.0%, JP Morgan -1.21% and Citigroup -1.55%, while Bank of NY Mellon surged 3.29%.

- Next week sees Blackrock and Goldman Sachs on Monday; Bank of America, Charles Schwab, State Street and Morgan Stanley on Tuesday; Citizens Financial, US Bancorp, Discover Financial and Ally Financial on Wednesday; KeyCorp, M&T Bank and Blackstone on Thursday; Fifth Third, Regions Financial, Comerica, American Express and Huntington next Friday.

E-MINI S&P TECHS: (U4) Bullish Trend Sequence Remains Intact

- RES 4: 5764.00 3.50 proj of the Apr 19 - 29 - May 2 price swing

- RES 3: 5741.34 3.236 proj of the Apr 19 - 29 - May 2 price swing

- RES 2: 5713.31 3.236 proj of the Apr 19 - 29 - May 2 price swing

- RES 1: 5707.75 High Jul 11

- PRICE: 5698.00 @ 1520 ET Jul 12

- SUP 1: 5630.00 Low Jul 11

- SUP 2: 5559.64/5453.20 20- and 50-day EMA values

- SUP 3: 5398.75 Low Jun 11

- SUP 4: 5267.75 Low May 31 and key support

The trend condition in S&P E-Minis is bullish and the contract traded to a fresh trend high once again Thursday. The continuation higher confirms a resumption of the uptrend and maintains the bullish sequence of higher highs and higher lows. Moving average studies are in a clear bull-mode set-up too and this continues to highlight positive market sentiment. Sights are on the 5713.31, a Fibonacci projection. Firm support is at 5559.64, the 20-day EMA.

COMMODITIES Crude Falls on Week, Spot Gold Remains Close To May Highs

- Crude has slipped back during US hours although prices remain within the three-day trading range. WTI has erased some earlier gains driven by US inflation data supportive of near-term Fed rate cuts. WTI is down 0.8% on the week.

- WTI Aug 24 is down 0.2% today at $82.5/bbl.

- For WTI futures, sights are on $85.27, the Apr 12 high and a bull trigger. Initial firm support to watch is $80.01, the 50-day EMA.

- Spot gold is broadly unchanged at $2,417/oz, leaving the weekly gain at 1% and keeping the yellow metal around its highest level since May 22.

- The breach of $2,387.8, the Jun 7 high, has opened key resistance at $2,450.1, the May 20 high. Initial support to watch lies at the 50-day EMA, at $2,336.2.

- Meanwhile, copper has rebounded by 1.9% to $459/lb, unwinding most of yesterday’s losses, although the red metal remains down by 1.3% on the week.

- Prices have been under pressure this week due to an increase in inventories at the LME, highlighting concerns about excess supply as Chinese demand softens.

- A bearish corrective cycle in copper that started May 20, remains in play for now.

- A resumption of the bear leg would open $426.12, a Fibonacci retracement. Initial resistance to watch is $489.25, the May 29 high.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/07/2024 | 0200/1000 | *** |  | CN | GDP |

| 15/07/2024 | 0200/1000 | *** | | CN | Fixed-Asset Investment |

| 15/07/2024 | 0200/1000 | *** | | CN | Retail Sales |

| 15/07/2024 | 0200/1000 | *** | | CN | Industrial Output |

| 15/07/2024 | 0200/1000 | ** | | CN | Surveyed Unemployment Rate M/M |

| 15/07/2024 | 0700/0900 |  | EU | ECB's Lagarde and Cipollone in Eurogroup meeting | |

| 15/07/2024 | 0900/1100 | ** | | EU | Industrial Production |

| 15/07/2024 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 15/07/2024 | 1230/0830 | ** | | CA | Wholesale Trade |

| 15/07/2024 | 1230/0830 | ** |  | US | Empire State Manufacturing Survey |

| 15/07/2024 | 1430/1030 | ** | | CA | BOC Business Outlook Survey |

| 15/07/2024 | 1435/1035 | | US | San Francisco Fed's Mary Daly | |

| 15/07/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 15/07/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 15/07/2024 | 1630/1230 | | US | Fed Chair Jerome Powell |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.