- Treasuries continued to drift lower Friday, fully unwinding midweek support back to pre-CPI/Retail Sales levels.

- Leading Index missed (-0.6% MoM vs. -0.3 est) while stocks saw first negative contribution since October.

- Fed Gov Bowman reiterated stance in keeping interest rates steady to allow restrictive policy to bring inflation down.

US TSYS Mildly Weaker Tsys Flirting with Technical Support

- Treasury futures continued to gradually extend session lows by the bell, fully unwinding Wednesday's post-CPI/Retail Sales related rally. The Jun'24 10Y futures are -10.5 to 109-05, just below initial technical support of 109-07+ (50-day EMA).

- Little data to trade off of Friday, the Conference Board leading indicator fell by more than expected in April, -0.6% M/M (cons -0.3) after -0.3% in March.

- Unscheduled Fed speak underscored the day's move as Fed Gov Bowman reiterated stance in keeping interest rates steady to allow restrictive policy to bring inflation down.

- Rate cut projections remain largely in-line with this morning's levels (*): June 2024 at -10% w/ cumulative rate cut -2.5bp at 5.313%, July'24 at -22% w/ cumulative at -8bp at 5.258%, Sep'24 cumulative -21.1bp, Nov'24 cumulative -29.2bp, Dec'24 -44.4bp.Looking ahead to next week, the minutes to the May 1 FOMC will be released next Wednesday.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00032 to 5.31976 (-0.00011/wk)

- 3M +0.00006 to 5.32580 (+0.00382/wk)

- 6M +0.00513 to 5.28321 (-0.00110/wk)

- 12M +0.01638 to 5.12252 (-0.01641/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $2.001T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $753B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $737B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $78B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $265B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage rebounds to $449.373B from $410.121B prior; number of counterparties 73. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury option trade remained mixed Friday with better puts emerging in the former as underlying futures trade trade back to pre-CPI and Retail Sales levels. Rate cut projections remain largely in-line with this morning's levels (*): June 2024 at -10% w/ cumulative rate cut -2.5bp at 5.313%, July'24 at -22% w/ cumulative at -8bp at 5.258%, Sep'24 cumulative -21.1bp, Nov'24 cumulative -29.2bp, Dec'24 -44.4bp.

SOFR Options:- +10,000 SFRN4 94.68/94.75 put spds, 1.0 ref 94.885

- Over -45,000 (15k Blocked) SFRH5 96.00/96.50 call spds 7.5 vs. 95.38 to -.39/0.11%

- Block, +11,000 SFRM4 94.62 puts, 0.5 vs. 94.6675/0.05%

- +15,000 SFRV4 94.75/94.87/94.93/95.06 put condors, 2.5

- -2,000 SFRU4 94.87 straddles, 21.0-20.5

- Block, 15,000 SFRM4 94.75/95.00 1x2 call spds 0.0 ref 94.6925

- +4,000 SFRM4 94.62/95.00 call over risk reversals vs. 94.695/0.10%

- 1,000 SFRU4 94.62/94.75/94.81/94.88 broken put condors

- 1,800 SFRU4 94.62/94.75 put spds

- 2,000 SFRN4/SFRU4 94.68 put spds

- +5,500 0QH5 94.50/95.00 put spds, 6.0 ref 96.05

- 2,500 TYM4 108 puts

- 2,500 TYM4 107/108/109 call flys

- 5,000 TYN4 112/TYU4 114 call spd

- 4,000 USU4 112/117 2x1 put spds ref 117-22

- 1,000 TYM4 108.75/109.25 3x2 put spds, 13 ref 109-13

- 1,500 FVM4 106.25/107 1x2 call spds, 5 ref 106-01

- 3,800 FVM4 105.75/FVN4 106.75 call spds

EGBs-GILTS CASH CLOSE: Pullback Continues

Friday's trade closely mirrored the prior session's, with initial gains fading steadily over the rest of the day.

- ECB's Schnabel catalysed a bearish tone for core FI with her comment reported overnight that a July rate cut looked unlikely based on data to this point.

- Otherwise the main theme was a continued reconsideration of Wednesday's seemingly dovish US inflation and retail sales data, with both Bund and Gilt yields having now risen back above levels just prior to those releases. 2024 ECB / BoE implied cut pricings were pared by around 3bp apiece on the day.

- The calendar was limited in terms of speakers and data - final April Eurozone HICP was in line, with the ECB's calculated underlying inflation measures showing moderation.

- The German curve bear flattened, with the UK's bear steepening.

- Periphery EGB spreads tightened a touch, with Portugal (Moody's) and Spain (Fitch) due for ratings reviews after the close.

- Next week's calendar includes UK CPI data and an appearance by BoE's Bailey, along with flash May PMIs.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

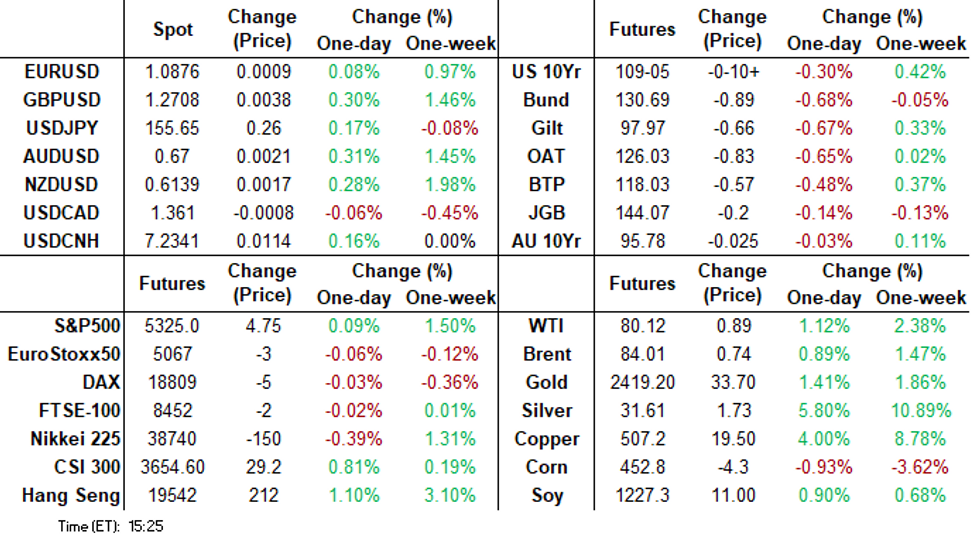

- Germany: The 2-Yr yield is up 5.9bps at 2.986%, 5-Yr is up 6.1bps at 2.561%, 10-Yr is up 5.5bps at 2.515%, and 30-Yr is up 4.7bps at 2.653%.

- UK: The 2-Yr yield is up 3.6bps at 4.31%, 5-Yr is up 4.3bps at 4.009%, 10-Yr is up 4.8bps at 4.127%, and 30-Yr is up 4.1bps at 4.6%.

- Italian BTP spread down 0.1bps at 129.9bps / Spanish down 0.2bps at 75.7bps

EGB Options: Schatz Structures Feature Friday

Friday's Europe rates/bond options flow included:

- DUN4 105.40/105.60/105.80c fly, bought for 4 in 3k

- DUN4 105.50/105.20ps vs 105.70c, bought the ps for half in 12k

- RXN4 134.50/135.00cs, bought for 5 in 1875, total 7,875 for 5 and 5.5 all day

- ERM5 97.25/97.75/98.00c fly vs 96.75/96.50ps, bought the c fly for 2.75 in 2k

FOREX USD Sales Pick Up into WMR Fix

- USD selling bias becoming more evident headed into the Friday WMR fix, with EUR/USD and GBP/USD now touching new daily highs and putting GBP/USD within range of 1.2701, the mid-week high and firm resistance. Clearance here opens firmer resistance and the bull trigger at the mid-April high of 1.2709.

- USD move seemingly independent of the more muted equity and bond markets in recent trade - but is favouring precious metals, as gold takes advantage and narrows the gap with 2417.89 (late April high), and 2431.5 (Alltime high).

- No specific news or data catalyst to drive greenback weakness - but volumes are lower than average for this time of day. EUR futures see cumulative activity around 15% below the recent average.

FX Expiries for May20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0680-00(E1.9bln), $1.0850-55(E1.5bln), $1.0875(E885mln), $1.0900(E772mln)

- USD/JPY: Y154.00($1.2bln), Y155.00($584mln), Y156.45-50($1.4bln)

- GBP/USD: $1.2625-45(Gbp718mln)

- AUD/USD: $0.6780-00(A$1.2bln)

- NZD/USD: $0.6100(N$732mln), $0.6144-50(N$520mln)

- USD/CAD: C$1.3535($721mln), C$1.3730($735mln)

- USD/CNY: Cny7.2490($530mln)

Late Equities Roundup: Extending Late Session Lows

- Stocks have retreated slightly late Friday, extending session lows recently heading into the weekend. Currently, the DJIA is up 26.64 points (0.07%) at 39895.89, S&P E-Minis down 7.5 points (-0.14%) at 5312.5, Nasdaq down 56.7 points (-0.3%) at 16641.39.

- Energy and Materials sectors continue to lead gainers in the second half, oil and gas shares supporting the former: Valero +3.60%, Marathon Petroleum +2.8%, EQT Corp +1.93%. Metals and mining stocks buoy the latter with gold trading over $40 higher now: Freeport McMoRan +3.6%, Newmont Corp +1.96%.

- Laggers: Information Technology and Utilities traded weaker late, semiconductor stocks weighing on IT as they unwound early week gains: Lam Research -3.91%, Nvidia -2.47%, Micron -2.15%. Electricity providers weighed on the Utilities sector: Constellation Energy -2.08%, Ameren Corp -1.08%, Eversource Energy -0.96%.

- Reminder: a few late cycle corporate earnings expected next week: Zoom Video Conf, Palo Alto Networks, Macy's Inc, Lowe's Inc, AutoZone Inc, Target, Petco, Analog Devices, TJX, Synopsys, Nvidia, Autodesk, Dollar Tree Inc.

E-MINI S&P TECHS: (M4) Bulls Remain In The Driver’s Seat

- RES 4: 5417.75 2.00 proj of the Apr 19 - 29 - May 2 price swing

- RES 3: 5400.00 Round number resistance

- RES 2: 5372.73 1.764 proj of the Apr 19 - 29 - May 2 price swing

- RES 1: 5349.00 High May 16

- PRICE: 5312.50 @ 1450 ET May 17

- SUP 1: 5207.52 20-day EMA

- SUP 2: 5166.93 50-day EMA

- SUP 3: 5036.25 Low May 2

- SUP 4: 4963.50 Low Apr 19 and bear trigger

S&P E-Minis have traded higher this week as the contract extends the bull cycle from Apr 19. Bullish trend conditions remain intact. Recent gains have resulted in a break of key resistance at 5333.50, Apr 1 high. This confirms a resumption of the primary uptrend and signals scope for a climb to 5372.73, a Fibonacci projection. Moving average studies remain in a bull-mode set-up, highlighting a clear uptrend. Initial support is at 5207.52, the 20-day EMA.

COMMODITIES Silver Surges To Highest Since 2013, Gold, Copper Near Record Highs

- Spot silver has surged by 5.6% on Friday to $31.2/oz, taking it to its highest level since 2013.

- A technical breakout has been at play, as the precious metal has risen by more than 10% this week, taking YTD gains to over 30%.

- Silver maintains a bullish theme and next resistance is seen at $31.623, a Fibonacci projection.

- Meanwhile, spot gold is up by 1.6% to $2,415/oz, taking the weekly gain to 2.3%, and leaving the yellow metal less than 1% below its April 12 record high.

- Clearance of this level would confirm a resumption of the uptrend, with attention on $2,452.5 next.

- Copper has also surged by another 3.8% today to $506/lb, leaving the metal just 1.3% below its record high reached earlier this week.

- Copper futures remain in a clear uptrend and have pierced a key resistance again at $503.95, the Mar 2022 high. Next resistance is at $516.58, a Fibonacci projection.

- WTI is on track for weekly gains of 2.3%, with some US and Chinese economic data appearing more supportive for future oil demand. The market’s focus has shifted from geopolitical risks back towards supply-demand fundamentals.

- WTI Jun 24 is up 1% at $80.0/bbl.

- For WTI futures, scope is seen for a move to $76.07, the Mar 11 low. On the upside, initial firm resistance is at $84.46, the Apr 26 high.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 18/05/2024 | 2145/1745 |  | US | Fed Governor Adriana Kugler | |

| 19/05/2024 | 1930/1530 | | US | Fed Chair Jerome Powell | |

| 20/05/2024 | 0600/0800 | ** |  | DE | PPI |

| 20/05/2024 | 0900/1000 |  | UK | BOE's Broadbent Monetary Mechanism Workshop | |

| 20/05/2024 | - | | UK | DMO to hold quarterly consultation investors / GEMM consultation | |

| 20/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 20/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |