Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

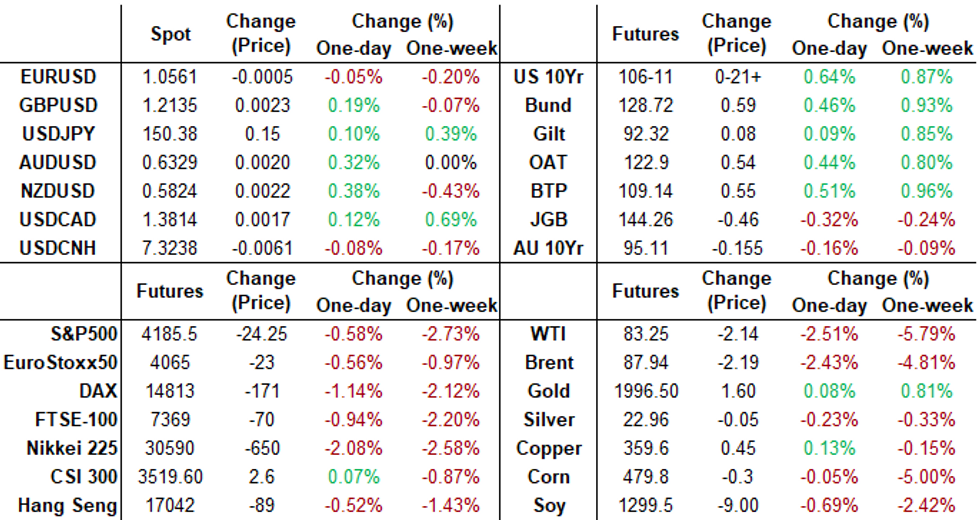

- YELLEN: YIELDS REFLECT STRONG ECONOMY, HIGHER-FOR-LONGER RATES, Bbg

- MNI SLOVAKIA: PM Announces Halt To Ukraine Military Aid, Sets Up Confrontation w/EU

- ECB POLICYMAKERS AGREED TO DEBATE PEPP REINVESTMENT END DATE THIS WINTER AND MINIMUM RESERVES AS PART OF THE FRAMEWORK REVIEW - SOURCES, Rtrs

US TSYS FI Consolidation, Tsys Near Midrange for the Week

- US Treasury futures continued to extend gains in late trade, near session highs to midrange for the week. Shorts consolidated following this morning's higher than expected Q3 GDP (4.9% vs. 4.5% est, 2.1% prior) - largely driven by inventories and softer than expected core PCE prices (2.4% vs. 2.5% est) and jobless claims (210k vs 207k est, 198k prior) at their highest in five months, suggesting that labor market tightness may start to wane.

- Additional FI support after the $38B 7Y note auction (91282CJG7) stops through: 4.908% high yield vs. 4.910% WI; 2.70x bid-to-cover vs. 2.47x last month.

- Current Dec'23 10Y futures are at 106-10 +20.5) vs. 106-13 high, still well below initial technical resistance of 106-31 (20-day EMA), 10Y yield at 4.8487% (-.1062) vs. 4.9873% high overnight. Curves reverse course - mostly flatter: 3M10Y at -61.524 (-8.971), 2Y 10Y -3.332 at -20.112.

- FI short end support translates to softer projected rate hikes into early 2024: November holding at 1.6%, w/ implied rate change of +.4bp to 5.333%, December cumulative of 5.5bp at 5.383%, January 2024 cumulative 7.9bp at 5.408%, while March 2024 slips to 3.5bp at 5.364%. Fed terminal at 5.438% in Jan'24. Fed terminal at 5.410% in Feb'24.

- Look Ahead: corporate earnings after the close that includes: L3Harris, Ford, Juniper Networks, Olin, Capital One, Intel, US Steel and Amazon. Friday data calendar includes Personal Income/Spending, UofM Inflation Exp

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00081 to 5.32686 (-0.00476/wk)

- 3M +0.00249 to 5.38998 (-0.00849/wk)

- 6M +0.00108 to 5.45691 (-0.01257/wk)

- 12M +0.00763 to 5.40349 (-0.03486/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $93B

- Daily Overnight Bank Funding Rate: 5.32% volume: $239B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.439T

- Broad General Collateral Rate (BGCR): 5.30%, $564B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $554B

- (rate, volume levels reflect prior session)

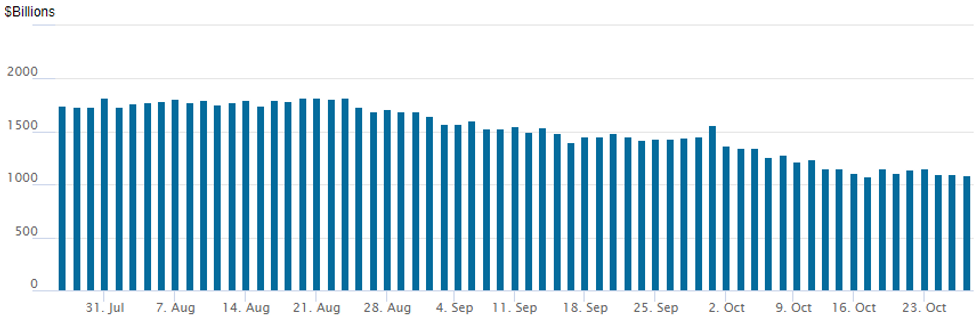

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

The NY Fed Reverse Repo operation usage slips to $1,089.850B w/98 counterparties vs. $1,100.617B in the prior session -- just above last week Tuesday's $1,082.399B - the lowest level since mid-September 2021. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

Mixed SOFR/Treasury option flow remained mixed even as underlying futures reversed early losses/finishing higher after mixed data. Projected rate hikes into early 2024 have cooled: November holding at 1.6%, w/ implied rate change of +.4bp to 5.333%, December cumulative of 5bp at 5.379%, January 2024 cumulative 7.4bp at 5.403%, March 2024 at 3.3bp at 5.361%. Fed terminal slips to 5.405% in Feb'24. Reminder, Nov serial Tsy options also expire Friday.

SOFR Options:

Block, 5,000 SFRM4 95.50/96.25 call spds 9.5 vs. 94.855/0.12%

Block, 2,500 SFRH4 94.25/94.37 put spds vs. SFRH4 94.62/94.75 call spds ref 94.63, appr 7.5k more on screen

9,000 SFRZ3 94.31/94.37/94.43/94.50 put condors ref 94.55

over 4,000 SFRH4 94.12/94.37 put spds vs. SFRH4 94.62/94.87 call spds ref 94.63

2,000 0QZ3 95.50/95.87/96.25 call flys ref 95.31

2,000 SFRX3 94.75/95.00 call spds ref 94.56

2,800 0QZ3 95.37/95.62/96.00 broken call trees ref 95.31

Block, 10,000 SFRM4 94.50/94.81 put spds vs. 95.50 calls, 3.5 net call over

Block, 5,000 SFRM4 94.50/94.81 put spds vs. 95.50 calls, 4.0 net call over

2,000 SFRU4 95.50/96.50/97.00 broken call flys ref 95.075

Treasury Options: Reminder, Nov serial options expire Friday

2,500 TYZ3 104/107.5 strangles, 52 ref 106-03.5

+4,000 TYZ3 99.5/103/104.5/105.5 put condors 5 over the TYZ3 108.5/110 call spds

9,000 FVX3 FVX3 103.5/103.75 2x1 put spds

over 8,500 TYX3 106.5 calls, 3 ref 105-16 to -21

2,000 TYZ3 109.5/110.5 call spds

5,000 TYZ3 105/106 2x3 put spds ref 105-19 to -18.5

3,000 USZ3 99/100 put spds ref 107-31

2,000 FVZ3 101.5/102 put spds ref 104=02.75

Note on Wed's 50,000 TYZ3 107.5 puts open interest +39,936 to 94,166

EGBs-GILTS CASH CLOSE: Rally On Lack Of Hawkish ECB Surprises

Bunds outperformed Gilts Thursday, as the ECB meeting was in line with expectations.

- The decision to leave rates unchanged with communication virtually identical to the September meeting and no hawkish surprises (eg on balance sheet policy) saw a modest drop in EGB yields to session lows.

- Periphery spreads tightened after Pres Lagarde said early in the press conference that the Governing Council didn't discuss changes to PEPP policy at this meeting.

- However, Reuters reported just before the close that ECB policymakers agreed to debate PEPP policy early next year - pushing BTP/Bund spreads back up above 200bp.

- European instruments also benefited concurrently from US data that was seen as soft (including core Q3 inflation and weekly jobless claims).

- The German and UK curves finished steeper, with outperformance at the short end/belly.

- Friday's docket includes Italian and French sentiment data, the ECB's Survey of Professional Forecasters, and Spanish GDP., with attention likely to turn quickly to Eurozone flash October inflation data Mon and Tues.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 5bps at 3.075%, 5-Yr is down 4.4bps at 2.725%, 10-Yr is down 2.8bps at 2.861%, and 30-Yr is unchanged at 3.126%.

- UK: The 2-Yr yield is down 2.4bps at 4.82%, 5-Yr is down 2.7bps at 4.542%, 10-Yr is down 1.3bps at 4.597%, and 30-Yr is up 0.6bps at 5.068%.

- Italian BTP spread down 1.7bps at 200.9bps / Greek down 5.1bps at 134.1bps

EGB Options: Mostly Euribor Midcurve Plays On ECB Day

Thursday's Europe rates / bond options flow included:

- 0RH4 97.375 call v 2RH4 97.625 call, buys the 0R for 1.5 in 3k

- 2RZ3 97.50/98.00 call spread bought for 4 in 2k

FOREX USD Index Consolidates Strength Despite Yield Pullback

- Firmer US growth data and struggling equity indices have underpinned further greenback strength on Thursday. With currency volatility low throughout the US session, the USD index stands just 0.10% in the green ahead of the APAC crossover. The consolidation of USD strength is notable given the pullback for US yields that have shifted between 8-12bps lower across the curve.

- The morning session was highlighted by some significant moves for the Japanese yen, especially after the period of stagnant price action in recent weeks. With the post-5y auction weakness in Treasury futures persisting into Thursday morning and the resulting widening of the US/JN yield differential, USDJPY pushed to a new recovery high of 150.78. Shortly following the print, a sharp spike in volumes saw the rate correct lower, prompting a ~75 pip slide to new lows before stabilising. Price action raised focus on the October 31st BoJ reserves release, at which markets will gain official confirmation of any market intervention.

- Very little reaction for the single currency following the ECB hold, with EURUSD grinding to session lows around 1.0530 amid the additional stronger US GDP data.

- Price has risen 30 pips from those lows but overall, this week’s sell off reinforces a bearish theme for the pair. Note too that Tuesday’s price pattern is a bearish engulfing candle - a reversal signal. A continuation lower would signal scope for 1.0496, the Oct 13 low. The key support and bear trigger lies at 1.0448, Oct 3 low.

- The minor weakness in the Euro has been offset by a firmer AUD and NZD, both rising around 0.35% and eating into yesterday’s steep move lower.

- On Friday, US Core PCE deflator data will cross as well as personal income data. The week’s calendar will finish with the revisions to UMich sentiment data and inflation expectations.

FX Expiries for Oct27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500-10(E2.1bln), $1.0535-50(E2.4bln), $1.0575-80(E756mln), $1.0600(E1.3bln), $1.0650(E1.0bln)

- USD/JPY: Y149.00($749mln), Y150.00($4.2bln), Y150.50($534mln)

- AUD/USD: $0.6325(A$544mln)

- USD/CAD: C$1.3835($758mln)

- USD/CNY: Cny7.3000($1.1bln)

Late Equity Roundup: Paring Losses Ahead Corporate Earnings

- Stocks are still weaker but paring losses in late Thursday trade, short covering ahead another round of corporate earnings after the close that includes: L3Harris, Ford, Juniper Networks, Olin, Capital One, Intel, US Steel and Amazon. Currently, the DJIA is down 88.99 points (-0.27%) at 32944.3, S&P E-Mini futures down 29.5 points (-0.7%) at 4177.5, Nasdaq down 160.2 points (-1.2%) at 12658.2.

- Laggers: Communication Services, Information Technology and Energy sectors continued to underperform, media and entertainment weighing on the former with Meta -3.8%, Charter Comm -2.95%, Google -2.35%. Meanwhile Comcast shed -8.2% after beating estimates but annc'd a drop in broadband subscribers.

- Hardware/software makers weighed on the IT sector: Western Digital -9.7% after merger with Japan's Kioxia is called off, Arista Networks -7.47%, Microsoft -3.45% and Nvidia -3.3%. Meanwhile, Energy sector shares weighed by weaker crude prices (WTI -2.10 at 83.29): Diamondback -2.45%, Halliburton -2.35%, APA -2.1%.

- Leaders: Real Estate and Materials sectors continued to outperform, specialized and office REITs buoyed the former: American Tower +8.2%, Equinix +5.15%, Crown Castle +4.8%. Metals and mining shares supported the Materials sector: Steel Dynamics +3.7% while Newmont gained +3.15% despite missing estimates, apparently up after reports it's purchase of Newcrest Mining will go through in early November.

E-MINI S&P TECHS: (Z3) Bear Cycle Extends

- RES 4: 4469.25 Trendline resistance drawn from the Jul 27 high

- RES 3: 4430.50 High Oct 12

- RES 2: 4391.63 50-day EMA

- RES 1: 4213.25/4328.94 Low Oct 23 / 20-day EMA

- PRICE: 4180.00 @ 1450 ET Oct 26

- SUP 1: 4166.25 1.50 proj of the Jul 27 - Aug 18 - Sep 1 price swing

- SUP 2: 4134.00 Low May 4

- SUP 3: 4124.19 61.8% retracement of the Mar - Jul bull leg (cont)

- SUP 4: 4100.00 Round number support

S&P e-minis maintain a softer tone and the contract has traded lower today. This week’s breach of support at 4235.50, the Oct 4 low and bear trigger, confirms a resumption of the downtrend and maintains the bearish price sequence of lower lows and lower highs. Moving average studies are in a bear-mode position too. The focus is on 4166.25, a Fibonacci projection. Initial firm resistance is at 4328.94, the 20-day EMA.

COMMODITIES Crude Reverses Yesterday’s Lift On Gaza Ground Invasion Headlines

- Crude markets have been dropping further during US hours, as some of the additional geopolitical risk premium continues to fall. Focus also remains on an uncertain demand picture. Crude has retreated following a partial rebound after the release of stronger than expected GDP growth, although which landed at the same time as a surprise lift in continuing jobless claims.

- Overnight saw confirmation that the Israeli military had put a “relatively large” contingent of troops and tanks into northern Gaza in order to attack several Hamas militant targets in the area. The incursion at present looks short of a full ground operation in the territory.

- The oil futures market may have priced in a war premium in recent weeks, but the fall today is more reflective of the sell-off observed in the physical market.

- MNI COMMODITY ANALYSIS: Russian Crude Exports Breaching Commitments as Refining Still Lags. Full piece here.

- WTI is -2.5% at $83.23 but having only unwound yesterday’s invasion headlines driven increase remains above key support at $80.20 (Oct 6 low).

- Brent is -2.5% at $87.90, above support at $85.18 (Oct 12 low) after which lies the bear trigger at $83.44 (Oct 6 low).

- Gold is +0.35% at $1986.45, gaining late in the session as the USD fades to help the yellow metal lift further off lows $1971.87 back to levels from earlier in the session. Resistance is seen at $1997.2 (Oct 20 high).

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 27/10/2023 | 2330/0830 | ** |  | JP | Tokyo CPI |

| 27/10/2023 | 0030/1130 | * |  | AU | Producer price index q/q |

| 27/10/2023 | 0600/0800 | ** |  | SE | Retail Sales |

| 27/10/2023 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 27/10/2023 | 0700/0900 | *** |  | ES | GDP (p) |

| 27/10/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 27/10/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 27/10/2023 | - |  | EU | ECB's Lagarde Participates in Euro Summit | |

| 27/10/2023 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 27/10/2023 | 1300/0900 | | US | Fed's Michael Barr | |

| 27/10/2023 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 27/10/2023 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.