Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI US FED: Fed’s Barkin Sees No Hurry To Cut Rates, Bbg TV

- MNI US: Senate Republicans Hint At Positive Movement On NatSec Supplemental

- MNI GERMANY: New Populist Party Erodes AfD Polling Support As EP Election Nears

- TSY SEC YELLEN: IT'S OBVIOUS THAT THERE IS GOING TO BE BANKING STRESS, LOSSES ASSOCIATED WITH COMMERCIAL REAL ESTATE, Rtrs

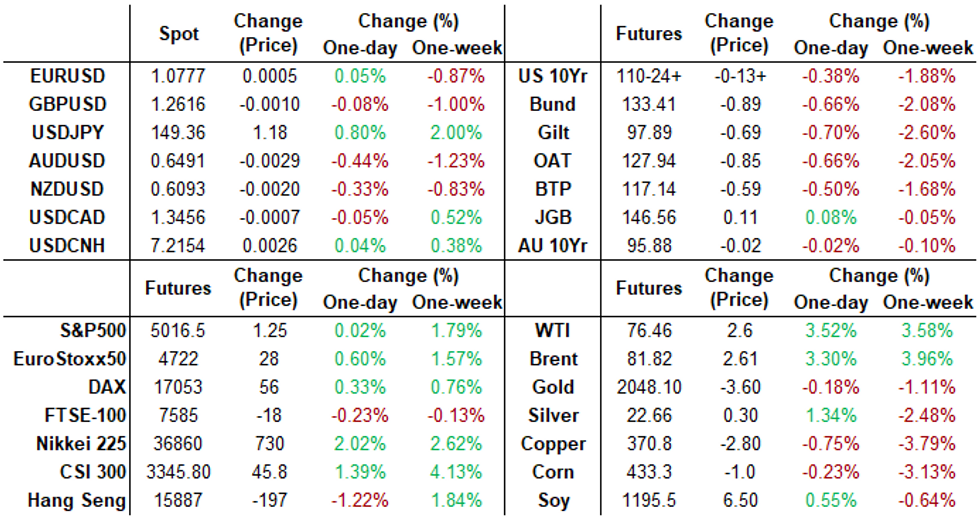

US TSYS Markets Roundup: Yields Climb Ahead Friday's CPI Revisions

- Tsy futures are extending session lows since gradually reversing post-30Y Bond auction support. Currently, Mar'24 10Y futures tap 110-23.5 low (-14.5; 10Y yield 4.1696% high) - nears initial technical support of 110-22+ (Low Feb 5 and the bear trigger) followed by 110-16 Low Dec 13).

- TYH4 had bounced to 110-31.5 after the strong $25B 30Y auction (912810TX6) stopped through for the third consecutive time: 4.360% high yield vs. 4.380% WI. Decent to strong demand all week, all three coupon auctions stopping through- which hasn't occurred since January 2023.

- Rates ticked lower following this mornings Initial jobless claims recorded a seasonally adjusted 218k (cons 220k) in the week to Feb 3 after last week’s surprise increase was revised a little higher to 227k (initial 224k).

- Fed speak: the Federal Reserve has time to wait before cutting interest rates as the economy remains strong even as inflation falls, Richmond Fed President Thomas Barkin said Thursday. “You don’t have to be in any particular hurry. We’ve got some time to be patient,” Barkin said in an interview with Bloomberg TV.

- Otherwise, Thursday was a generally quiet session as market awaits CPI revisions from the BLS early Friday: BLS will update seasonal factors affecting CPI inflation through 2019-23 on Friday, Feb 9 “from 0830ET”.

- This won’t impact the underlying NSA data, but will sway near-term trends and has been flagged by both Fed Governor Waller and Chair Powell referencing the upside surprise in last year’s annual revision. Analysts are mixed, seeing either very little impact or modest uplift in recent trend rates.

FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00311 to 5.31800 (-0.00411/wk)

- 3M -0.01291 to 5.30135 (+0.01089/wk)

- 6M -0.02111 to 5.17233 (+0.07623/wk)

- 12M -0.02704 to 4.84630 (+0.15350/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.797T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $688B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $673B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $96B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $270B

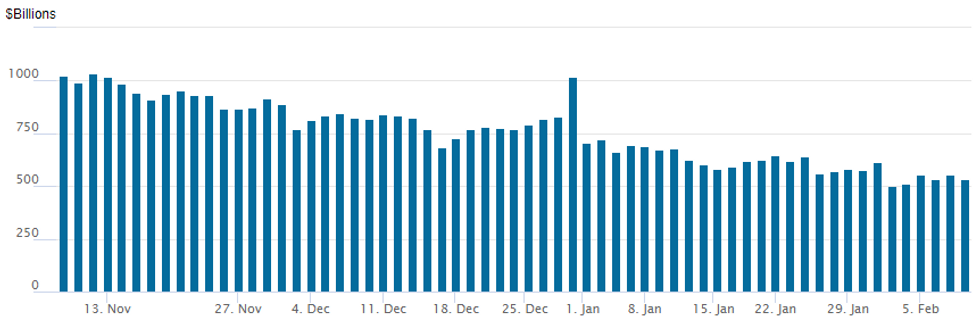

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage slips back to $535.705B vs. $553.055B Wednesday. Holding above recent cycle low of $503.548B from Thursday, February 1, the lowest level since mid-2021.

- Meanwhile, the latest number of counterparties is at 78 from 75 Wednesday (compares to 65 on January 16, the lowest since July 7, 2021).

SOFR/TREASURY OPTION SUMMARY

SOFR and Tsy option flow remained mixed but leaned toward low delta put structures Thursday as underlying futures continued to extend lows: TYH4 at 110-23 (-15) still above Monday low of 110-2.5. Projected rate cut pricing consolidates vs. late Wednesday lvls: March 2024 chance of 25bp rate cut currently -21.2% w/ cumulative of -5.3bp at 5.271%, May 2024 at -53.1% vs. -61.2% late Wednesday w/ cumulative -18.6bp at 5.138%, while June 2024 -89.3% vs. -90% (105% pre-NFP for comparison) w/ cumulative -40.9bp at 4.915%. Fed terminal at 5.325% in Feb'24.

SOFR Options:

Block 18,000 SFRJ4 94.62/94.93 put spds 3.75 vs. SFRM4 94.68/94.87 put spds 4.5

Block, 10,000 SFRM4 95.12/95.25 call spds, 4.5 vs. 95.155/0.10, more on screen

Block, 1,875 SFRU4 95.25/95.37 5x4 put spds, 6.0 net ref 95.535

Block, 5,000 SFRH4 94.81/94.87 call spds 1.0 ref 94.785

4,000 SFRM4 94.87/95.00 put spds ref 95.16

4,000 0QH4 96.00/3QH4 96.37 put spds

3,000 SFRH4 95.00/95.06/95.12 call flys ref 94.79

2,000 SFRU4 95.50/95.62 call spds vs. 94.93/95.06 put spds ref 95.545

4,000 SFRK4 95.18/95.31/95.43 call flys ref 95.165

over 25,800 SFRH4 94.75 puts, 3.5 last tied to 94.68/94.75/94.68 ratio put fly

Block, 5,000 SFRU4 95.68/96.00 call spds 1.0 over 94.87/95.12 put spd ref 95.56

4,000 SFRH4 94.75 puts ref 94.785

Treasury Options:

35,000 TYH4 109.25/110.25/111.25 put flys

1,200 FVH4 109.75/FVJ4 109.25/FVK4 110.5/FVM4 110 call condor, Mar/Jun bought vs. Apr/May

3,000 USH4 116/118 put spds 17 ref 120-01

5,000 FVH4 110.25 calls ref 107-13.75

Block, 8,000 TYH4 110/110.25/110.75 put trees, 1 net - 2 legs over vs. 111-05/0.10%

1,000 TYH4 109/110 3x2 put spds , 12 ref 111-05.5

5,000 wk1 10Y 109.5/110.5 put spds ref 111-20.5 (expire March 1)

1,000 FVH4 106.75/107 put spds ref 107-16.25

EGBs-GILTS CASH CLOSE: 4th Down Day in 5 Sees Bellies Underperform

Bunds and Gilts weakened for the 4th session in 5 Thursday with curve bellies undeperforming, as central bank speakers maintained a cautious tone on the rate cut trajectory.

• ECB's Lane reiterated that more disinflation will need to be seen before having confidence that inflation will sustainably return to target. Wunsch, and - after the close, Holzmann - were unsurprisingly hawkish. All of the above eyed wage growth dynamics in particular.

• BoE's Mann said little to suggest she would soon change her vote after opting for a hike in February, and noted she "can't say whether there will be rate cuts this year".

• On the day, 2024 ECB and BoE cut pricing were each pared by 4-5bp.

• Gilts underperformed Bunds, with both the UK and German curves leaning bear flatter (though as mentioned, the bellies of the curves performed weakest, as rate cuts got priced out).

• Periphery spreads were largely unchanged, with GGBs outperforming.

• Friday morning's schedule includes Italian industrial production and final German inflation data.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

• Germany: The 2-Yr yield is up 3bps at 2.66%, 5-Yr is up 4.1bps at 2.284%, 10-Yr is up 3.8bps at 2.354%, and 30-Yr is up 2.9bps at 2.569%.

• UK: The 2-Yr yield is up 7.6bps at 4.553%, 5-Yr is up 8bps at 4.052%, 10-Yr is up 6.3bps at 4.051%, and 30-Yr is up 3.9bps at 4.609%.

• Italian BTP spread up 0.4bps at 157.7bps / Greek down 3.4bps at 115.2bps

FOREX Japanese Yen Remains On Backfoot, Substantial Moves In EM FX

- Mixed price action across G10 on Thursday saw the USD index tilt marginally into positive territory, rising 0.1% as we approach the APAC crossover. This was dominated by a strong 0.75% move higher in USDJPY, on the back of some dovish leaning rhetoric from Bank of Japan’s Uchida.

- The policymaker acknowledged the likely need for tighter policy in Japan in the near-term, but played down the prospect of a more protracted tightening cycle after a first theoretical rate hike. He stated that it is hard to see Japan requiring a sharp hiking pace after rate lift-off, helping boost USDJPY back to the best levels of 2024 above 148.89.

- JPY weakness then persisted across the US session with the slightly better-than-expected jobless claims data providing additional impetus for USDJPY above 149.00. The pair rose to a high of 149.48 and will now focus on 149.75, the Nov 22 high.

- The higher US yields also weighed on the likes of AUD and NZD, however, the Euro remained more resilient throughout Thursday’s session. A bearish theme in AUDUSD remains intact and any short-term gains continue to be considered corrective. The latest break to fresh cycle lows confirmed a resumption of the downtrend and signals scope for weakness towards 0.6453, the Nov 17 low and 0.6412, a Fibonacci retracement level.

- In emerging markets, divergence in communication between the central banks of the CE3 economies has led to some interesting moves across CE3 FX.

- A dovish CNB vote split and relatively hawkish NBP press conference by Governor Glapinski has led to a 1.6% surge in PLNCZK, which pierced the 5.8000 handle for the first time since March 2021, and is currently at its highest since December 2020.

- Additionally, USDCLP brushed off a higher inflation release and has extended its powerful move higher, rising 1.2% on the session.

- US inflation revisions in focus Friday. BLS will update seasonal factors affecting CPI inflation through 2019-23 on Friday, Feb 9 “from 0830ET”.

FX Expiries for Feb09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0700(E1.0bln), $1.0725(E745mln), $1.0750(E716mln), $1.0800-10(E1.2bln), $1.0850(E2.8bln), $1.0900(E2.1bln)

- USD/JPY: Y147.50($1.4bln), Y148.50-65($2.1bln), Y149.00($647mln)

- EUR/JPY: Y157.65-75(E812mln)

- AUD/USD: $0.6500-10(A$1.2bln), $0.6525(A$551mln)

- USD/CAD: C$1.3300($1.1bln), C$1.3340-50($1.9bln), C$1.3400($736mln), C$1.3545-55($1.1bln)

- USD/CNY: Cny7.2115($1.3bln)

Equities Roundup: Nasdaq Posting Modest Gains

- Stocks are trading mildly firmer late Thursday, Nasdaq led gainers later in the second half. Currently, the DJIA are up 37.46 points (0.1%) at 38713.98, S&P E-Minis up 1 points (0.02%) at 5016.25, Nasdaq up 44.6 points (0.3%) at 15800.79.

- Leading gainers: Real Estate and Energy sector shares narrowly outperformed in the second half, industrial and office real estate investment trusts (REITS) buoyed the former: Prologis +2.23%, Boston Properties +1.77%. Oil and gas shares supported the Energy sector as crude prices rebounded (WTI +2.19 at 76.05): Devon Energy +1.94%, Conoco-Phillips +1.46% while Exon Mobil gained 1.22%.

- Laggers: Utilities and Financial sectors underperformed, electricity and independent power shares weighed on the former: Duke Energy -2.69%, Pinnacle West -2.59%, Edison Int -2.44%. Meanwhile banks and financial services traded weaker: despite beating earnings estimates ,PayPal Holding sank -11.21% on disappointing forward guidance, Everest Grp -8.29%, FleetCor -7.7%.

- Looking ahead: corporate earnings expected after the close: Expedia, Mettler-Toledo, Take-Two Interactive, Pinterest. Early Friday: PepsiCo, Blue Owl Capital and Catalent Inc.

E-MINI S&P TECHS: (H4) Bull Cycle Extends

- RES 4: 5110.50 2.00 proj of Nov 10 - Dec 1 - 7 price swing

- RES 3: 5100.00 Round number resistance

- RES 2: 5050.14 1.764 proj of Nov 10 - Dec 1 - 7 price swing

- RES 1: 5020.00 High Feb 7

- PRICE: 5015.50 @ 1510 ET Feb 8

- SUP 1: 4902.99 20-day EMA

- SUP 2: 4866.000/4796.82 Low Jan 31 / 50-day EMA values

- SUP 3: 4702.00 Low Jan 5

- SUP 4: 4594.00 Low Nov 30

The trend condition in S&P E-Minis is unchanged and remains bullish - yesterday’s gains reinforce current conditions. The contract has traded to a fresh cycle high, confirming a resumption of the uptrend. Recent corrections have been shallow - this also highlights a strong uptrend. The focus is on 5050.14, a Fibonacci projection. On the downside, initial key short-term support has been defined at 4866.00, the Jan 31 low.

COMMODITIES Crude Oil Climbs On Fading Hopes Of Near-Term Ceasefire Deal In Gaza

- Crude prices are headed for their highest close since Jan. 31. Prices are finding support from diminishing hope of any near-term ceasefire deal in Gaza and thus no end in sight for Middle East tensions.

- Israeli PM Netanyahu, appeared to pour cold water on a ceasefire, telling reporters that Israel, "will not suffice with less," than a decisive victory in their war against Hamas.

- The attacks in the Red Sea have become increasingly dangerous in the last days and the level of threats have likely not peaked yet, Maersk CEO Vincent Clerc said.

- Oil demand is better than expected in the first week of February with a boost in China from the Lunar New Year holiday and with better weather in the US and Asia according to JPMorgan.

- WTI is +3.5% at $76.47, gaining through the session to push closer to resistance at $76.95 (Feb 1 high) after which lies key resistance at $79.29 (Jan 29 high).

- Brent is +3.3% at $81.85, clearing $81.55 (Feb 1 high) to key open a key short-term resistance at $84.17 (Jan 29 high).

- Gold is -0.1% at $2032.73 despite ceasefire diminishing prospects, having mostly reversed a fleeting low of $2020.29 that remained above support at $2015.0 (Feb 5 low). The yellow metal sees some modest net downward pressure from the USD index reversing yesterday’s decline

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/02/2024 | 0700/0800 | *** |  | DE | HICP (f) |

| 09/02/2024 | 0700/0800 | ** |  | SE | Private Sector Production m/m |

| 09/02/2024 | 0700/0800 | *** |  | NO | CPI Norway |

| 09/02/2024 | 0900/1000 | * |  | IT | Industrial Production |

| 09/02/2024 | 1330/0830 | *** |  | CA | Labour Force Survey |

| 09/02/2024 | 1415/1515 |  | EU | ECB's Cipollone speaks at Assiom Forex Annual Congress | |

| 09/02/2024 | 1530/1030 | | CA | BOC Senior Loan Officer Survey | |

| 09/02/2024 | 1800/1300 | ** |  | US | Baker Hughes Rig Count Overview - Weekly |

| 09/02/2024 | 1830/1330 | | US | Dallas Fed's Lorie Logan |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.