Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- NY Fed Williams: Rate Path Driven By Developments In Economy

- MNI INTERVIEW: QE Has Run Its Course, Says Ex-Boe's Sentance

- MNI INTERVIEW: China May Bring In Tobin Tax-Ex PBOC Advisor

- MNI: FED BULLARD NO NEED TO MAKE ANY MOVES RIGHT NOW ON QE

- FED: St Louis Fed's Bullard: Room For "Substantial Decline" In Jobless Rate

US

FED: St Louis' Bullard Remains Satisfied With Current QE Bullard's tune on being satisfied with the current Fed QE setup hasn't changed in a while so those comments are no surprise...on Oct 6 he said: "[On further stimulus] I think the most likely direction would be quantitative easing, if we needed to do more. ... I think we're in good shape for now [re purchases]"..."We have our (quantitative easing) program in place with a substantial amount of purchases. I think that is appropriate. I like monetary policy right now. I really don't think we have to do anything differently now or going into next year."

FED: St Louis Fed President Bullard today is largely focused on COVID and the labor market. Key bit in that regard, from his speech today, is on unemployment, with room for a "substantial decline" in the jobless rate (Fed median from most recent projections in September is 7.6% end-2020, 5.5% end-2021, 4.6% end-2022).

- "A back-of-the-envelope calculation suggests that there is room for a substantial decline in the official unemployment rate in the months ahead."

- "If all those unemployed identifying as "on temporary layoff" are simply recalled and nothing else changes, the official unemployment rate would decline to 4.9%."

- "If the 'on temporary layoff' category returns to a normal value (e.g., 1 million workers) and nothing else changes, the official unemployment rate would still decline to 5.5%."

FED: On Judy Shelton's nomination for the Fed board (Senate votes on her next week): The decision about who to appoint is the President's / Senate's call, don't have any comments on that.

- On Fed's new forward guidance: Not a date-based based commitment; driven by economic developments. Given your view on the economy, what's the appropriate path for monetary policy.

- On Fed's avg inflation targeting: 'Not a mathematical formula', about having well-anchored inflation expectations at 2%. Not a complicated model, a simple principle.

- On climate change policy: It's an important risk to financial stability; Fed's already discussing climate change risks with banks.

- On post-election fiscal stimulus, and what the Fed's assumptions are: The lesson of the last 9 months is scenario analysis and understanding how different fiscal actions affect the econ outlook and the Fed's policy choices. Not going to give advice on what Congress etc should do; my view is that we're still in an extraordinary period with COVID. Previous fiscal stimulus made a huge difference in boosting consumer spending through the pandemic.

EUROPE

BOE: With yield curves flat and any surprise factor exhausted, the Bank of England's quantitative easing programme is largely impotent in supporting economic activity in the face of a pandemic and government-mandated lockdowns, former Monetary Policy Committee member Andrew Sentance told MNI.

- "People say 'another GBP150 billion of QE, what's that?' It has no impact on financial markets or on the public," he said, speaking after the BOE's latest expansion of its gilt purchases on Nov. 5. For more see 11/13 main wire at 0627ET.

ASIA

PBOC: The People's Bank of China could consider measures such as a tax on foreign exchange transactions as it accelerates the opening up of its financial markets, a former senior advisor to the PBOC told MNI. For more see 11/13 main wire at 0853ET.

OVERNIGHT DATA

US DATA: October PPI +0.3%; Core +0.1%

- U.S. final demand PPI rose 0.3% in October, above market expectations for a 0.2% gain, according to figures released Friday by the Bureau of Labor Statistics.

- From a year earlier, final demand PPI was up 0.5%.

- Nearly 60% of October's increase cam from a 0.5% increase in prices for final demand goods, the BLS said. Final demand services were up 0.2%, with trade services up 0.2% following another 0.2% increase in September.

- Final demand energy prices rose 0.8% in October following a 0.3% decline in September. Final demand food prices were up 2.4%.

- Excluding food and energy, final demand PPI was up 0.1%, below market expectations for a 0.2% increase. September core PPI was unrevised at +0.4%.

- From a year earlier, core PPI was up 1.1%.

- Excluding food, energy, and trade services, PPI was up 0.2% after rising 0.4% in September and up 0.8% from a year earlier.

MICHIGAN PRELIM. NOV. CONSUMER SENTIMENT AT 77; EST. 82

STATCAN: 74% OF FIRMS SEE STEADY PAYROLLS; 10% SEE LAYOFFS

CANADA FLASH OCT INDUSTRIAL PRICES 0.0% MOM; +1.0% YOY

MARKET SNAPSHOT

Key market levels in late Friday trade:- DJIA up 366.36 points (1.26%) at 29306.68

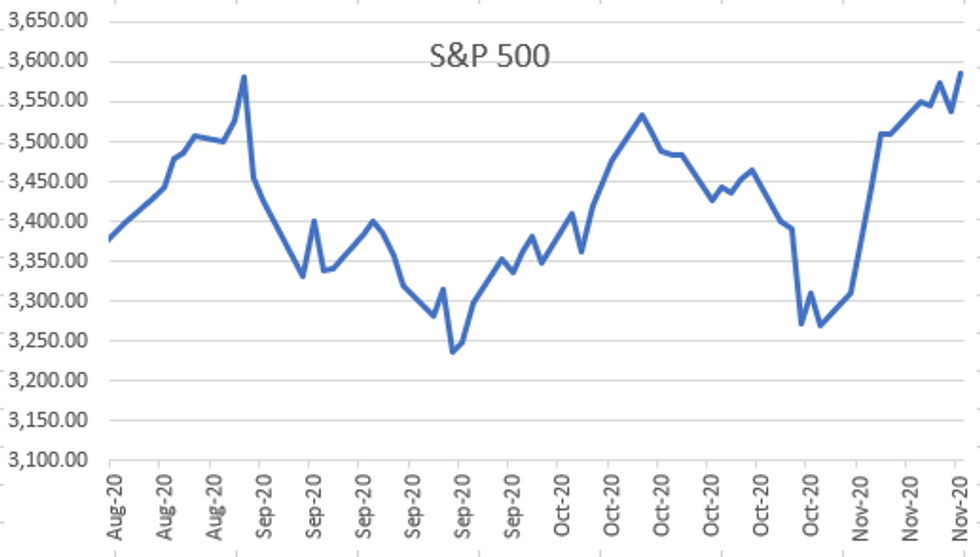

- S&P E-Mini Future up 40.5 points (1.15%) at 3558.5

- Nasdaq up 81.7 points (0.7%) at 11752.01

- US 10-Yr yield is up 0.7 bps at 0.8881%

- US Dec 10Y are down 1.5/32 at 138-3.5

- EURUSD up 0.0027 (0.23%) at 1.1827

- USDJPY down 0.51 (-0.49%) at 104.63

- WTI Crude Oil (front-month) down $0.9 (-2.19%) at $40.28

- Gold is up $8.52 (0.45%) at $1894.03

- European bourses closing levels:

- EuroStoxx 50 up 3.87 points (0.11%) at 3437.52

- FTSE 100 down 22.55 points (-0.36%) at 6323.13

- German DAX up 23.77 points (0.18%) at 13086.99

- French CAC 40 up 17.59 points (0.33%) at 5388.06

US TSY SUMMARY: Ready For A Change?

Swing states were called: Trump takes N. Carolina, Biden takes Georgia, final electoral count: Biden 306, Trump with 232. And yet, President Trump has not conceded. President Trump is scheduled to have his first press conference since the election at the WH Rose Garden this afternoon (after 1600ET) to discuss Operation Warp Speed as virus cases continue to rise globally).

- Tsy futures traded mostly weaker after the closing bell (Dec Ultra-bond bucked move), with equities trading near highs (ESZ0 +56.0) after remaining Much more sedate trade Fri, lighter volumes: TYZ<910k, only 57% 20D avg.

- Eurodollar futures were mildly weaker for the most part, lead quarterly EDZ0 holds -0.005 after 3M LIBOR set +0.00100 to 0.22200%, +0.01612 on week after falling to new all-time low of 0.20500% Monday of this week. November options expire.

- CBOE vol index VIX was notably weaker late: -2.29 at 23.06 vs. 22.74 session low.

- The 2-Yr yield is up 0bps at 0.177%, 5-Yr is up 1bps at 0.4014%, 10-Yr is up 0.7bps at 0.8881%, and 30-Yr is up 0.2bps at 1.6402%.

US TSY FUTURES CLOSE: Risk-On Gains Late

Futures traded mostly weaker after the closing bell (Dec Ultra-bond bucked move), with equities trading near highs (ESZ0 +44.0) after remaining swing states were called: Trump takes N. Carolina, Biden takes Georgia, final electoral count: Biden 306, Trump with 232. Much more sedate trade Fri, lighter volumes: TYZ<910k, only 57% 20D avg. Yld curves mildly mixed, update:

- 3M10Y +1.147, 80.174 (L: 76.558 / H: 80.666)

- 2Y10Y +1.124, 71.397 (L: 68.71 / H: 71.925)

- 2Y30Y +0.741, 146.714 (L: 143.568 / H: 147.646)

- 5Y30Y -0.38, 124.158 (L: 122.641 / H: 125.07)

- Current futures levels:

- Dec 2Y down 0.12/32 at 110-11.5 (L: 110-11.25/ H: 110-11.75)

- Dec 5Y down 0.75/32 at 125-15.25 (L: 125-14.5 / H: 125-17.75)

- Dec 10Y down 2/32 at 138-3 (L: 138-01.5 / H: 138-10.5)

- Dec 30Y down 3/32 at 172-6 (L: 172-00 / H: 172-27)

- Dec Ultra 30Y up 5/32 at 215-5 (L: 214-22 / H: 216-12)

US EURODOLLAR FUTURES CLOSE: Weaker By The Bell

Mildly weaker for the most part, lead quarterly EDZ0 holds -0.005 after 3M LIBOR set +0.00100 to 0.22200%, +0.01612 on week after falling to new all-time low of 0.20500% Monday of this week.

- Dec 20 -0.005 at 99.750

- Mar 21 -0.005 at 99.780

- Jun 21 -0.005 at 99.785

- Sep 21 -0.005 at 99.780

- Red Pack (Dec 21-Sep 22) -0.005 to steady

- Green Pack (Dec 22-Sep 23) -0.010 to -0.005

- Blue Pack (Dec 23-Sep 24) -0.010 to -0.005

- Gold Pack (Dec 24-Sep 25) -0.015 to -0.010

US DOLLAR LIBOR

Latest settles

- O/N +0.00175 at 0.08325% (+0.00062/wk)

- 1 Month -0.00450 to 0.13638% (+0.00863/wk)

- 3 Month +0.00100 to 0.22200% (+0.01612/wk)

- 6 Month -0.00538 to 0.24600% (+0.00262/wk)

- 1 Year -0.00112 to 0.33938% (+0.00605/wk)

US TSY: Short Term Rates

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.09% volume: $57B

- Daily Overnight Bank Funding Rate: 0.09%, volume: $165B

- Secured Overnight Financing Rate (SOFR): 0.09%, $912

- Broad General Collateral Rate (BGCR): 0.07%, $350

- Tri-Party General Collateral Rate (TGCR): 0.07%, $323

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.801B accepted vs. $29.858B submission

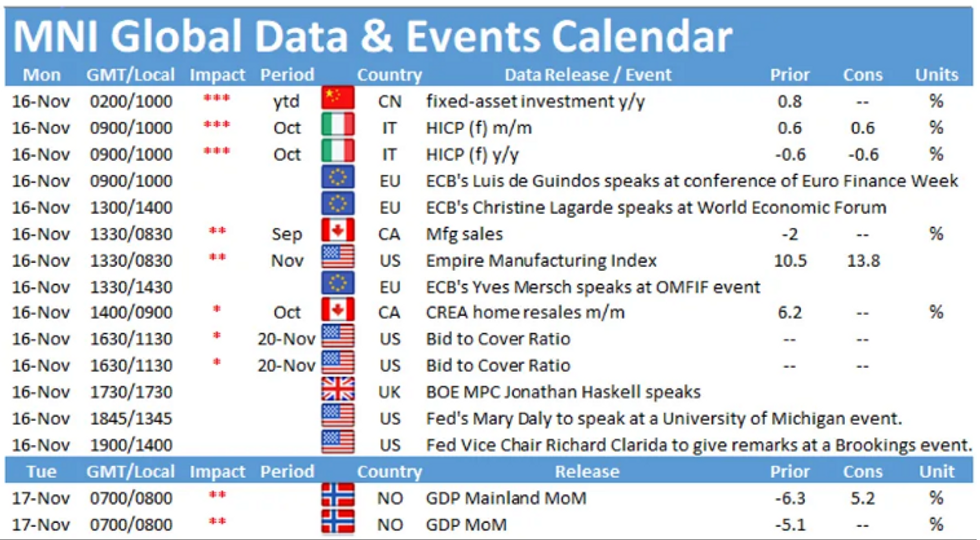

- Updated NY Fed operational purchase schedule, $40.2B from 11/16-11/30

- Mon 11/16 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Tue 11/17 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Tue 11/17 1100-1120ET: Tsy 2.25Y-4.5Y, appr $8.825B

- Wed 11/18 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Thu 11/19 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

- Fri 11/20 1010-1030ET: Tsy 0Y-2.25Y, appr $12.825B

- Mon 11/23 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Tue 11/24 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

- Mon 11/30 1010-1030ET: Tsys 20Y-30Y, appr $1.750B

- Mon 11/30 Next forward schedule release at 1500ET

PIPELINE: Strong Week

Total $44.35B high-grade debt priced over 3 sessions. Headliners: $7B Bristol-Myers Squibb 6pt Monday; $12B Verizon 5pt Tuesday; $5.75B JP Morgan fix-FRN 3pt Thursday.

- Date $MM Issuer (Priced *, Launch #

- Not new issuance Friday, may price next week:

- 11/?? $Benchmark Rep of Italy, 5Y, 30Y

- 11/?? $Benchmark BNG Bank 5Y Reg S

- -

- $10B Priced Thursday

- 11/12 $5.75B *JP Morgan fix-FRN: $2.75B 6NC5 +65, $1.4B 11NC10 +90, $1.6B 21NC20 +87.5

- 11/12 $1.5B *Societe Generale PNC10 5.375%

- 11/12 $1.45B *Pacific Gas & Electric 1Y FRN 3M LIBOR +137.5

- 11/12 $800M *Equitable Financial Life $500M 3Y +32, $300M 10Y +90

- 11/12 $500M *Inner Mongolia Yili 5Y Reg S +125

FOREX: JPY in Demand Despite Equity Market Progress

Despite the uptick in US equities Friday, haven currencies were in demand, prompting JPY to climb to the top of the G10 pack. USD/JPY made decent progress below the Y105.00 handle as markets further reversed the reflation trades placed at the beginning of the week. Despite the JPY strength, however, the week's lows are yet to be tested at 103.19.

- GBP traded well, but GBP/USD failed to make any meaningful attempt on the 1.32 handle, with near-term Brexit risks still clearly the driver. Some saw the departure of key PM aide Cummings as paving the path for a smoother Brexit deal, keeping attention on forthcoming Brexit negotiations in the coming week.

- USD was mixed, with a lack of key drivers Friday. Data was ineffectual, with the October PPI report mixed.

- The upcoming week sees the frequency of tier 1 data pick up, with industrial production & retail sales numbers from China & the US, UK & Canadian inflation and Australian jobs numbers. Speeches from various ECB, Fed and BoE members are due throughout the week.

EGBs-GILTS CASH CLOSE: Ending The Week With A Whimper

Having started the day on a firm footing, gilts have oscillated within a relatively tight band and have traded through the course of the afternoon towards yesterday's closing levels.

- Cash yields are now broadly unch on the day Last yields: 2-year -0.0312%, 5-year 0.0184%, 10-year 0.3428%, 30-year 0.9286%.

- The Dec-20 gilt future trades at 134.70, towards the weaker end of the day's range (L: 134.58 / H: 134.96).

- Short sterling futures trade mixed. whites/reds are flat/1.0 ticks lower while greens are flat/0.5 ticks lower and blues are flat/0.0 ticks higher.

- Speculation that PM Boris Johnson's close advisor Dominic Cummings could soon leave Downing St as been a source of constant newsflow through the day, but direct implications are limited.

- Looking ahead, next week sees the release of CPI data for October, public finance data and retail sales for October.

UP TODAY

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.