Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI POLICY: Fiscal Help Best For Next 6 Months-Fed's Williams

- MNI EXCLUSIVE: Canada Could Have Tapped FX Reserves In Crisis

- MNI INTERVIEW: UK To Avoid Fiscal Rules In Spending Review

- MNI INTERVIEW: Swedish Unemployment To Rise After Improvement

- TSY SEC MNUCHIN: TO PLACE $455 BLN UNSPENT CARES MONEY IN GENERAL FUND; NEEDS CONGRESSIONAL APPROVAL TO USE GENERAL-FUND MONEY, Bbg

US

FED New York Fed President John Williams said Tuesday the best tool to get through the next six months is fiscal policy even while the Fed could reopen emergency lending facilities or adjust asset purchases.

- "Fiscal policy is really the most powerful tool right now" and "that's the thing that would be most effective at getting us through the next six months," Williams said. For more see MNI Policy Main Wire at 1246ET.

CANADA

CANADA: Canada's finance department laid out options for accessing cash in May in case regular debt auctions became doubtful, like tapping emergency funds held at the central bank or dipping into foreign reserves, according to a briefing document obtained by MNI following a freedom-of-information request.

- "Should the government anticipate difficulties in issuing debt in time and cash balances drop too low to meet financial requirements, additional contingency measures may be considered," said the eight-page document addressed to then-Finance Minister Bill Morneau from Paul Rochon, the department's top civil servant. For more see MNI Policy Main Wire at 1317ET.

EUROPE

UK: The UK Treasury will avoid producing new fiscal rules to accompany a year-long spending review to be announced Wednesday, James Smith, Research Director at leading think tank the Resolution Foundation, told MNI.

- "I presume they will say they will come back at the Budget with a new fiscal framework," Smith said in an interview. "They don't want to tie their hands to a fiscal stance that's too tight or make promises to deliver against particular rules when that would be economically damaging," Smith said. For more see MNI Policy Main Wire at 1221ET.

SWEDEN: Swedish unemployment is set to start rising again as new Covid restrictions hit sectors such as hotels and restaurants which had powered a recent labour market recovery, particularly among young workers, Sara Schanberg, an economist at the government's National Institute of Economic Research told MNI. For more see MNI Policy Main Wire at 1141ET.

OVERNIGHT DATA

- US SEP CASE-SHILLER SEAS ADJ HOME PRICE INDEX +1.3% M/M

- US SEP CASE-SHILLER UNADJ HOME INDEX +1.2% M/M; +6.6% Y/Y

- US SEP CASE-SHILLER NATIONAL IDX +1.4% SA, +1.2% NSA, +7.0% Y/Y

- US NOV PHILADELPHIA FED NONMFG INDEX -15.9

- US REDBOOK: NOV STORE SALES -0.5% V OCT THROUGH NOV 21 WK

- US REDBOOK: NOV STORE SALES +1.9% V YR AGO MO

- US REDBOOK: STORE SALES +2.8% WK ENDED NOV 21 V YR AGO WK

- "The advance results for October indicate that manufacturing sales increased 0.6%, mostly due to higher sales in the petroleum and coal products, paper, primary metals and wood products industries," Statistics Canada said Tuesday

- Response rate of 58% vs 12m average of 90%

- On Monday StatsCan's Oct wholesale flash was +0.9%

MARKETS SNAPSHOT

- DJIA up 421.02 points (1.42%) at 30037.1

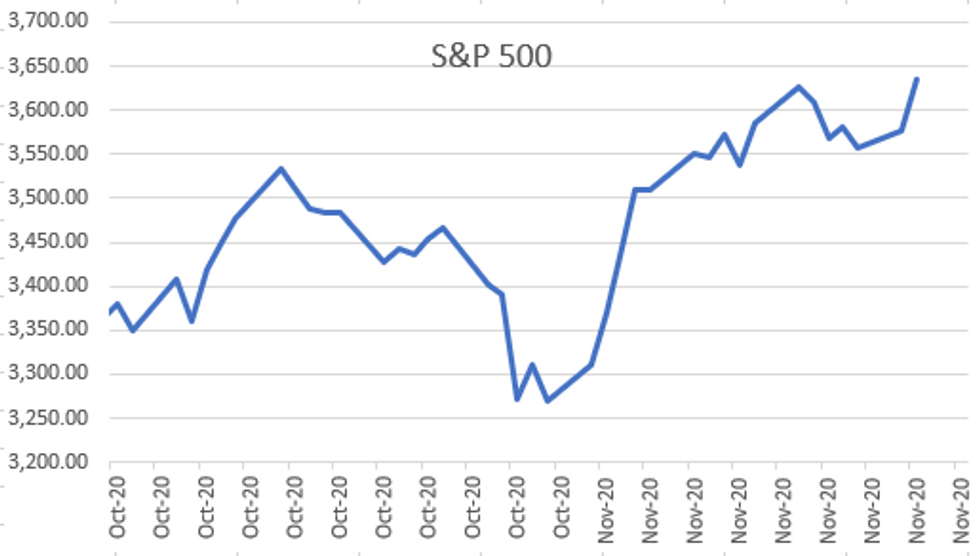

- S&P E-Mini Future up 53 points (1.48%) at 3631.75

- Nasdaq up 145.3 points (1.2%) at 12029.89

- US 10-Yr yield is up 2.5 bps at 0.8783%

- US Dec 10Y are down 1/32 at 138-9

- EURUSD up 0.0047 (0.4%) at 1.1879

- USDJPY down 0.04 (-0.04%) at 104.55

- WTI Crude Oil (front-month) up $1.83 (4.25%) at $44.82

- Gold is down $29.8 (-1.62%) at $1804.79

- European bourses closing levels:

- EuroStoxx 50 up 44.94 points (1.3%) at 3502.4

- FTSE 100 up 98.33 points (1.55%) at 6405.48

- German DAX up 165.47 points (1.26%) at 13256.4

- French CAC 40 up 66.27 points (1.21%) at 5566.74

US TSY SUMMARY: Risk Appetite Grows

Long-end support after early London Block buys evaporated quickly, Tsys chopped lower through NY session as equities made new highs (DJIA cracked 30,000 for first time, climbed to 30116.51 all-time high). No market react to headline "TRUMP WEIGHING SANCTIONS RELATED TO CRACKDOWN IN HONG KONG: NYT".

- Modest, short term bounce after decent 7Y auction stopped through: $56B 7Y Note drew high yield 0.653% rate (0.600% last month) vs. 0.657% WI; 2.37 bid/cover vs. 2.24 prior.

- Heavy volumes tied to Dec/Mar futures rolls, more than half complete ahead next Monday's first notice.

- Eurodollar futures volume Spike, on more LIBOR retirement positioning? Over -50,000 EDH2 at 99.71-.705. Massive volumes centered in Eurodollar Reds (EDZ1-EDU2) both outright and on spreads recorded this month most likely due to LIBOR transition to the Secured Overnight Financing Rate (SOFR) positioning and risk mitigation.

- The 2-Yr yield is up 0.3bps at 0.1622%, 5-Yr is up 0.8bps at 0.3924%, 10-Yr is up 2.1bps at 0.875%, and 30-Yr is up 4.4bps at 1.5974%.

US TSY FUTURES CLOSE: Risk-Appetite Gains Momentum

Tsy futures see-sawed around session lows after the bell, short end outperforming, yld curves broadly steeper on the day as equities made new highs (DJIA breached 30,000).

- 3M10Y +1.836, 79.348 (L: 76.309 / H: 80.004)

- 2Y10Y +2.754, 71.577 (L: 68.956 / H: 72.234)

- 2Y30Y +5.154, 143.912 (L: 138.555 / H: 144.569)

- 5Y30Y +3.909, 120.614 (L: 116.42 / H: 120.955)

- Current futures levels:

- Dec 2Y up 0.12/32 at 110-12.5 (L: 110-12.37 / H: 110-12.87)

- Dec 5Y steady at 125-17.75 (L: 125-16.75 / H: 125-19)

- Dec 10Y down 2/32 at 138-8 (L: 138-05.5 / H: 138-12)

- Dec 30Y down 19/32 at 172-28 (L: 172-20 / H: 173-18)

- Dec Ultra 30Y down 1-26/32 at 216-12 (L: 216-03 / H: 218-14)

US TSY FUTURES: Late Dec/Mar Roll Update: Well Over 50% Complete

Second Day Heavy Volumes as position holders scrambling to roll from Dec to Mar with shortened Thanksgiving holiday work week ahead Nov 30 "first notice". Dec futures won't expire until mid-late December: 10s, 30s and Ultras on 12/21; 2s & 5s 12/31.

- TUZ/TUH appr 656,800 0.25 last; 64% complete

- FVZ/FVH appr 844,200 -10.25 last; 64% complete

- TYZ/TYH appr 1,297,600 12.5 last; 69% complete

- UXYZ/UXYH appr 279,700, 18.75 last; 70% complete

- USZ/USH appr 480,800, -1-06.25 last; 77% complete

- WNZ/WNH appr 312,200, 1-21 last; 83% complete

US EURODOLLAR FUTURES CLOSE: Under Pressure, 3M LIBOR Bounce

Mostly steady in the short end to modestly weaker out the strip, Blues-Golds near low end narrow session range. Lead quarterly EDZ0 weaker after 3M LIBOR gapped +0.02575 higher to 0.23225% (+0.02737/wk). Heavy volume in Reds again, likely related to LIBOR retirement positioning. Latest levels:

- Dec 20 -0.005 at 99.750

- Mar 21 steady at 99.785

- Jun 21 steady at 99.790

- Sep 21 steady at 99.785

- Red Pack (Dec 21-Sep 22) -0.01 to steady

- Green Pack (Dec 22-Sep 23) -0.005 to steady

- Blue Pack (Dec 23-Sep 24) -0.015 to -0.01

- Gold Pack (Dec 24-Sep 25) -0.025 to -0.015

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles

- O/N -0.00187 at 0.08013% (-0.00250/wk)

- 1 Month -0.00713 to 0.14300% (-0.00713/wk)

- 3 Month +0.02575 to 0.23225% (+0.02737/wk)

- 6 Month +0.00075 to 0.25450% (+0.00575/wk)

- 1 Year +0.00000 to 0.33563% (-0.00087/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $62B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $201B

- Secured Overnight Financing Rate (SOFR): 0.05%, $913B

- Broad General Collateral Rate (BGCR): 0.04%, $343B

- Tri-Party General Collateral Rate (TGCR): 0.04%, $315B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $2.399B accepted vs. $4.407B submission

- Next scheduled purchase:

- Mon 11/30 1010-1030ET: Tsys 20Y-30Y, appr $1.750B

- Mon 11/30 Next forward schedule release at 1500ET

PIPELINE: Supra-Sovereigns Drives $6.5B US$ Issuance

- Date $MM Issuer (Priced *, Launch #)

- 11/24 $2.25B #Rep of Turkey 10Y +6.0%

- 11/24 $2B #IDA (Int Dev Assn, extn of World Bank), 10Y +19

- 11/24 $1.25B *Kommunivest 3Y +4

- 11/24 $1B #NWB (Nederlandse Waterschapsbank) 5Y +9

FOREX: JPY Sold as Equities Roar

The JPY was comfortably the poorest performer in G10 Tuesday, with USD/JPY topping the Monday high with relatively little resistance and prompting AUD/JPY to near a new multi-month high. JPY traded poorly alongside rallying equities worldwide. The Dow Jones crested 30,000 for the first time on record as further US states (notably Pennsylvania and Nevada) certified their election counts in favour of Biden).

- This worked in favour of antipodean and commodity-tied FX, with NZD, AUD and NOK outperforming. NZD/USD showed above the 0.70 level for the first time since mid-2018, opening congestion resistance above of 0.7060.

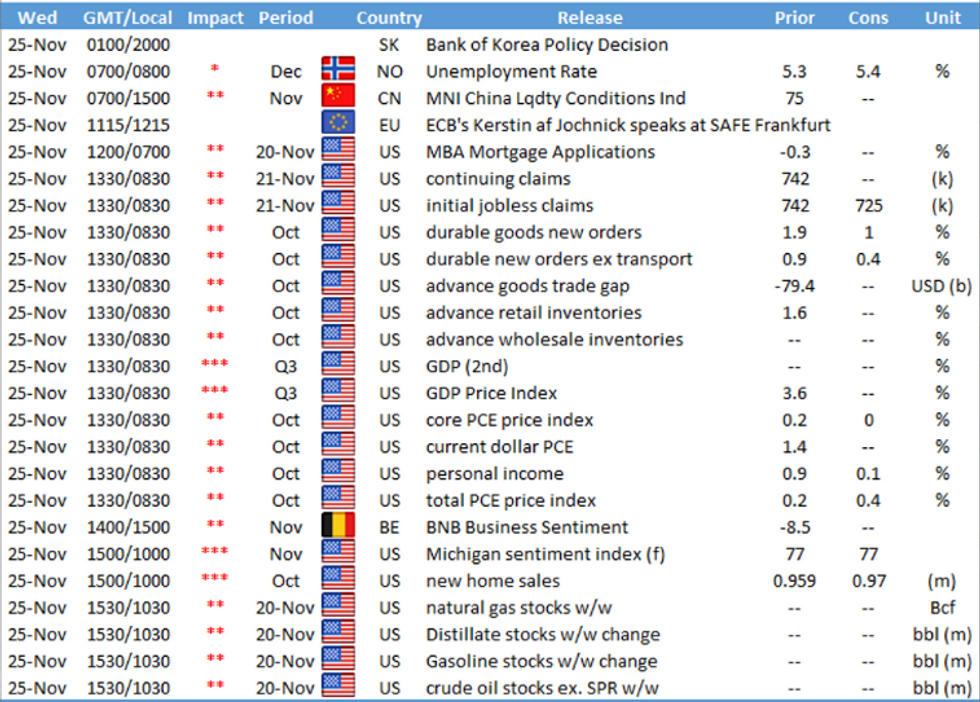

- Markets will likely quieten down either side of the Thanksgiving holidays on Thursday. As a result of the Thursday closures, data's frontloaded to Wednesday, with weekly jobless claims, secondary pass at GDP, trade balance, personal income/spending and durable goods orders as well as the FOMC minutes.

EGBs-GILTS CASH CLOSE: Can't Resist Soaring Equities

Core yields shrugged off higher equities for most of Tuesday's session, but UK and German yields bottomed out around 1500GMT and began moving sharply higher as European stocks rocketed following the U.S. cash equity open. Not to be outdone, 10-Yr BTP yields hit a record low (0.596%).

- French and German business confidence data were slightly weaker than expected, reflecting November lockdown woes, but this did not have a lasting impact. Speakers including ECB's Lagarde also did not move the needle.

- ECB's Lane and de Cos speak after the European close Tuesday; no scheduled speakers Wednesday and no key data scheduled. In supply, Italy sells CTZ and linkers.

- Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is up 1bps at -0.743%, 5-Yr is up 1.7bps at -0.745%, 10-Yr is up 1.8bps at -0.563%, and 30-Yr is up 1.6bps at -0.149%.

- UK: The 2-Yr yield is up 1.1bps at -0.018%, 5-Yr is up 1.5bps at 0.024%, 10-Yr is up 1.2bps at 0.33%, and 30-Yr is down 0.1bps at 0.901%.

- Italian BTP spread down 3bps at 117.5bps

- Spanish bond spread down 1.5bps at 63.7bps

- Portuguese PGB spread down 1bps at 59.6bps

- Greek bond spread down 1.8bps at 123.3bps

Up TODAY

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.