Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- SENATE AND HOUSE OF REPS LEADERS TO MEET ON STIMULUS

- "BIG BUZZ" AMONG TORY MPS THAT UK HEADING TOWARD BREXIT DEAL (BBC)

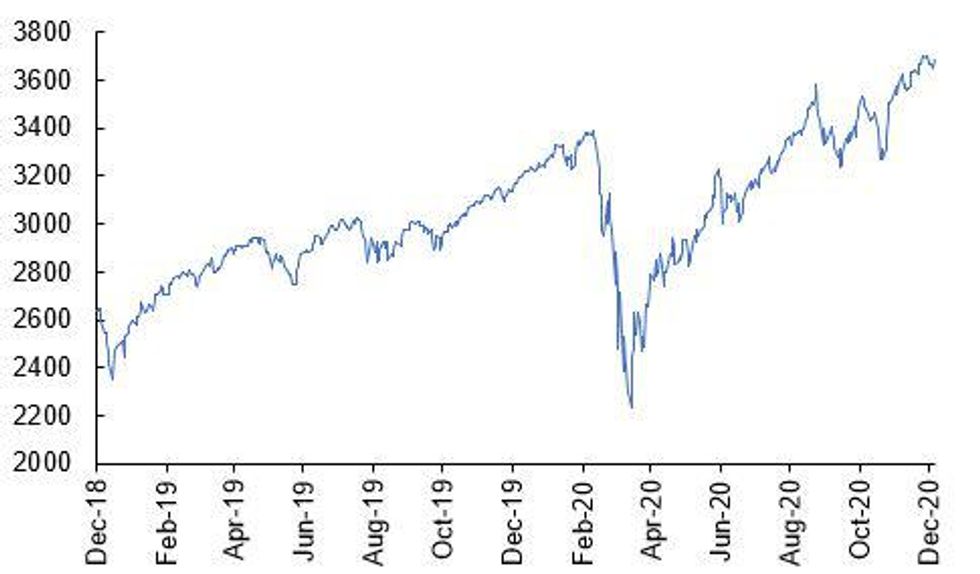

Fig.1: S&P 500 - Betting On A Deal

Source: MNI, Bloomberg

NEWS:

U.S.: A "big meeting" for Pelosi, McConnell, McCarthy, and Schumer at 4pm ET ... according to Politico's Jake Sherman via Twitter:

"NEW @SpeakerPelosi has invited her fellow leaders to a meeting thisafternoon to discuss finalizing govt funding and covid relief. meeting is for the Four Corners - @SpeakerPelosi, @senatemajldr, @GOPLeader and @SenSchumer...this meeting will be ~4p. invites are out to the leaders. govt funding runs dry fri. and leadership wants covid relief to ride on govt funding. this is a big mtg"

BREXIT: Gilts hit session lows and Cable flies on tweet by BBC Newsnight political editor @nicholaswatt: "Big buzz in the last hour among Tory MPs that the UK is heading towards a Brexit deal with the EU. Eurosceptics being reassured they will be happy." Gilts hit low of 134.48 (just below 134.56 EMA support) before bouncing; GBPUSD hits 1.3448 (testing 1.3446 yesterday's high, 1.3478 next resistance)before falling back.U.S.

U.S.: Senate Majority leader Mitch McConnell for the first time acknowledged Joe Biden as president-elect on the floor of the senate today.

* McConnell said "Our country has, officially, a president-elect and a vice president-elect.. Our system of government has processes to determine whowill be sworn in on Jan. 20. The Electoral College has spoken. So today I want to congratulate President-elect Joe Biden."* "I also want to congratulate the Vice President-elect, our colleague from California, Sen. Harris. Beyond our differences, all Americans can take pridethat our nation has a female Vice President-elect for the very first time."

Comes after the electoral college formally voted in Biden as president-elect yesterday. The next stage is for a joint session of Congress to tabulate andcertify the electoral college's votes on 6 January before the inauguration on20 January.

McConnell's reluctance to acknowledge Biden's win in the 3 November presidential election was becoming a story in itself, with even Russian President Vladimir Putin congratulating Biden before McConnell did.

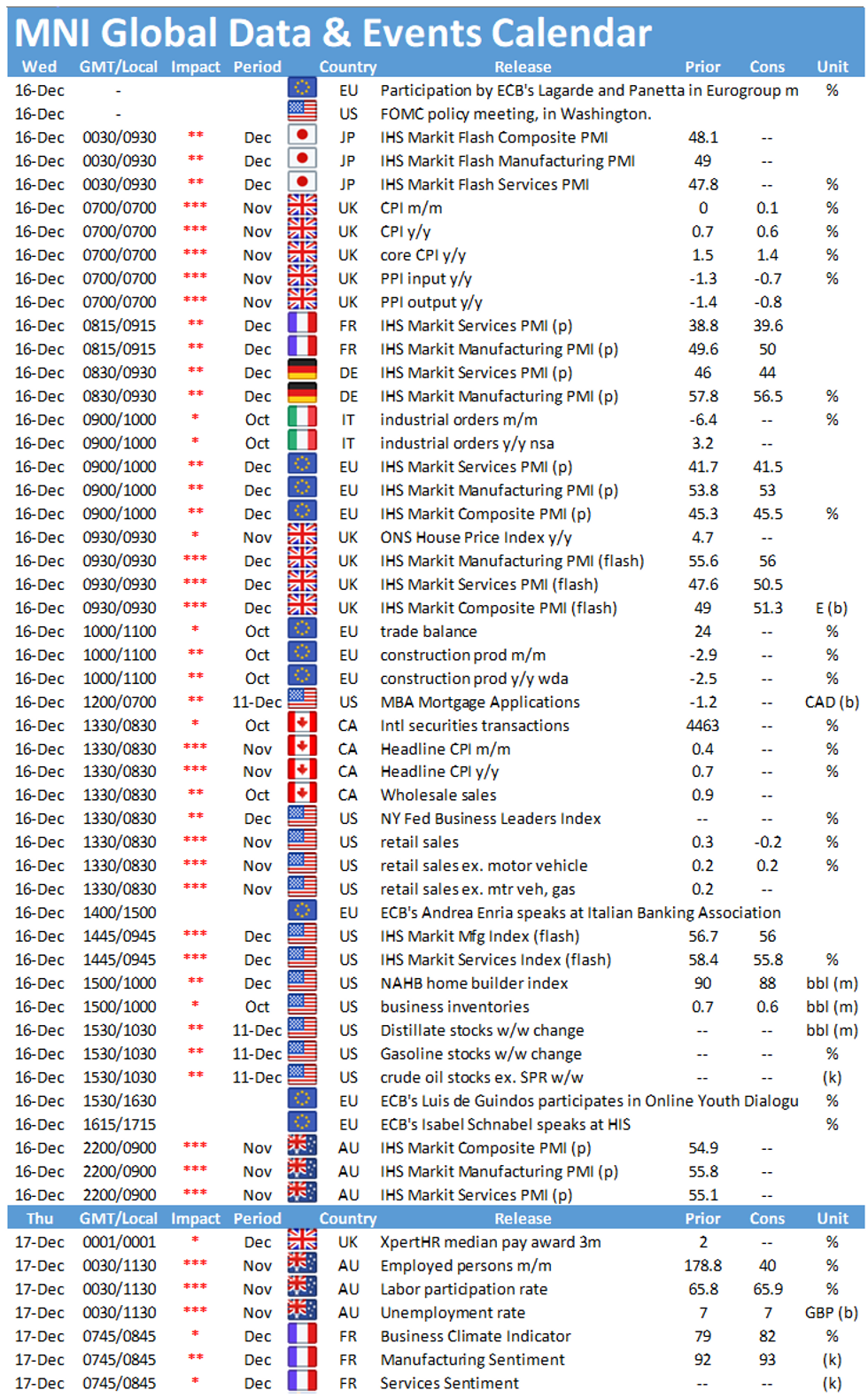

DATA:

MNI: US NOV INDUSTRIAL PROD +0.4%; CAP UTIL 73.3%

US DATA: November Import Prices +0.1%; Export +0.6%

MNI: US NY FED EMPIRE STATE MFG INDEX 4.9 DEC

MNI:US REDBOOK: DEC STORE SALES -2.2% V NOV THROUGH DEC 12 WK

MNI: CANADIAN OCT MANUFACTURING SALES +0.3% MOM

MNI: CANADA NOV HOUSING STARTS +14.4% TO 246,033 SAAR

US TSYS SUMMARY: Hopes of A Fiscal Deal Rising

Improving sentiment on the prospect of a US fiscal spending bill, coupled with a positive shift in global tailwinds (rising optimism on the Covid vaccine rollout and an orderly Brexit deal), has propelled equities higher and underpinned the bear steepening of the UST curve.

- Equities started the session on the weak footing, but soon gained ground with momentum building through the afternoon.

- UST yields are up to 3bp higher on the day with the long end of the curve underperforming. The 2s30s spread is 2bp wider. Last yields: 2-year 0.1190%, 5-year 0.3670%, 10-year 0.9113%, 30-year 1.6529%.

- TYH1 hit a session low of 137-26 in the afternoon before pulling back to 137-30.

- Today's data slate was relatively uneventful. Industrial production for November was a touch stronger than expected (0.4% M/M vs 03% survey), while the Empire Manufacturing print for December missed (4.9 vs 6.3).

- Looking ahead, tomorrow sees the release of November retail sales data and the flash PMI prints for December.

USD LIBOR FIX

O/N 0.08200 (-0.0005)

1W 0.10200 (0.00375)

1M 0.15250 (-0.00063)

2M 0.17925 (0.00587)

3M 0.22875 (0.0095)

6M 0.25175 (0.00462)

12M 0.33125 (-0.00363)

New York Fed EFFR for prior session (rate, chg from prev day):

- Daily Effective Fed Funds Rate: 0.09%, no change, volume: $51B

- Daily Overnight Bank Funding Rate: 0.08%, no change, volume: $143B

REPO REFERENCE RATES (rate, change from prev. day, volume):

- Secured Overnight Financing Rate (SOFR): 0.08%, no change, $907B

- Broad General Collateral Rate (BGCR): 0.06%, no change, $355B

- Tri-Party General Collateral Rate (TGCR): 0.06%, no change, $331B

NY Fed Operational Purchase (1st of 2)

Fed buys $8.801bn of 2.25-4.5Y Tsys, of $27.675bn submitted.

Next operation later today (1100-1120ET):- 7-20Y Tsys, ~$3.625bn

NY Fed Operational Purchase (2nd of 2)

Fed buys $3.601bn of 7-20Y Tsys, of $7.496bn submitted.

Next operations (both Thursday, skipping Weds due to FOMC):

- Thu 12/17: 20-30Y, ~$1.750bn (1010-1030ET)

- Thu 12/17: 1-7.5Y TIPS, ~$2.424bn (1100-1120ET)

EGBs-GILTS CASH CLOSE: A "Big Buzz" On Brexit Sinks Gilts

Gilts had already been having a weak day (in part due to a poor BoE APF result), but plummeted to session lows on a BBC political editor's tweet claiming a "big buzz" among Conservative MPs of a Brexit deal being reached this week.

- This exaggerated the bear steepening move in Gilts (5s30s shot 5bps higher between the 1445GMT APF result and the close). Periphery spreads tighter too as equities rose. In contrast, German curve fairly flat.

- Flash Dec PMIs and UK Nov CPI in focus on Wednesday.

Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is up 1.5bps at -0.756%, 5-Yr is up 1.1bps at -0.787%, 10-Yr is up 0.9bps at -0.611%, and 30-Yr is up 1.1bps at -0.201%.

- UK: The 2-Yr yield is up 3.5bps at -0.054%, 5-Yr is up 3.2bps at -0.029%, 10-Yr is up 3.8bps at 0.26%, and 30-Yr is up 6.4bps at 0.826%.

- Italian BTP spread down 3.1bps at 113bps

- Spanish bond spread down 2.9bps at 59.4bps / Portuguese down 2.6bps at 55.5bps

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.