Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI INTERVIEW: Fed Paper Makes New Case for Standing Repo Tool

- MNI POLICY: BOC Keeps QE and 0.25% Rate, Sees Slack Into '23

- MNI STATE OF PLAY:BOC Needs QE For a While, Depends on Rebound

- MNI BRIEF: BOE Bailey: Effects Of Lockdowns Diminishing

- MNI SOURCES: EU Officials Fear Politics To Delay Covid Funds

- CHINA SANCTIONS TRUMP ADMINISTRATION FIGURES INCLUDING POMPEO -bbg

US

US/CHINA: Google translate of the China Foreign Ministry Statement: "The spokesperson of the Ministry of Foreign Affairs announced that China imposed sanctions on Pompeo and others."

- "In the past few years, some anti-China politicians in the United States, out of their own political self-interest and prejudice and hatred towards China, have planned and promoted a series of crazy actions in disregard of the interests of the Chinese and American peoples, seriously interfering in China's internal affairs and harming China's interests It hurt the feelings of the Chinese people and severely damaged Sino-US relations. The Chinese government is unwavering in its determination to defend its national sovereignty, security and development interests. China has decided to impose sanctions on 28 people who have seriously violated China's sovereignty and are primarily responsible for China-related issues, including Pompeo, Navarro, O'Brien, Starwell, Pottinger, and Ahmad in the Trump administration. Zha, Krach, Kraft, Bolton, Bannon, etc. These people and their families have been prohibited from entering the mainland of China, Hong Kong and Macau. They and their affiliated companies and institutions have also been restricted from dealing with and doing business with China."

- A. Lee Smith of the Kansas City Fed and Victor J. Valcarcel of the University of Texas at Dallas said in an interview Friday that the drain on market liquidity as the Fed unwound its post-financial crisis balance sheet was almost twice as strong as the expansionary liquidity effects of QE, causing financial conditions to tighten and funding pressures to ripple into money markets and further to Treasury, corporate bond and foreign exchange markets.

CANADA

BOC: The Bank of Canada on Wednesday left its key lending rate at a record low 0.25% and said it will continue with at least CAD4 billion a week of asset purchases, with the near-term setback from the second wave of Covid-19 keeping the economy weak into 2023.

- "In view of the weakness of near-term growth and the protracted nature of the recovery, the Canadian economy will continue to require extraordinary monetary policy support," the Governing Council said in a statement. "Governing Council will hold the policy interest rate at the effective lower bound until economic slack is absorbed so that the 2 percent inflation target is sustainably achieved. In our projection, this does not happen until into 2023."

BOC: Bank of Canada Governor Tiff Macklem said Wednesday quantitative easing is needed for a while given the economy won't return to full output until 2023, but added he may taper federal government bond purchases if the economic rebound is better than projected.

- "This will be a gradual process," he said at a press conference when asked about scaling back the purchases. "We expect a protracted recovery, this is going to take some time, we are going to need this program for some time."

EUROPE

UK: Evidence suggested that successive Covid-19 lockdowns are having progressively less impact on the economy, Bank of England Governor Andrew Bailey told at a Citizens Panel event Wednesday.- The BOE is currently working on its latest quarterly forecast round and Bailey cited the rapid rise in online shopping as an example of how consumers and businesses are finding ways to mitigate the impact of the lockdowns. The UK is in its second full national lockdown and Bailey said that he anticipated "a quite pronounced recovery in the economy" as the vaccines rolled out.

- Ratification before the summer of an agreed increase in the EU's own resources, which is key to the bloc's bond issuance for the RRF and disbursement of the 13% pre-financing element of the fund, is essential for timely issuance and disbursement in coming months, officials told MNI.

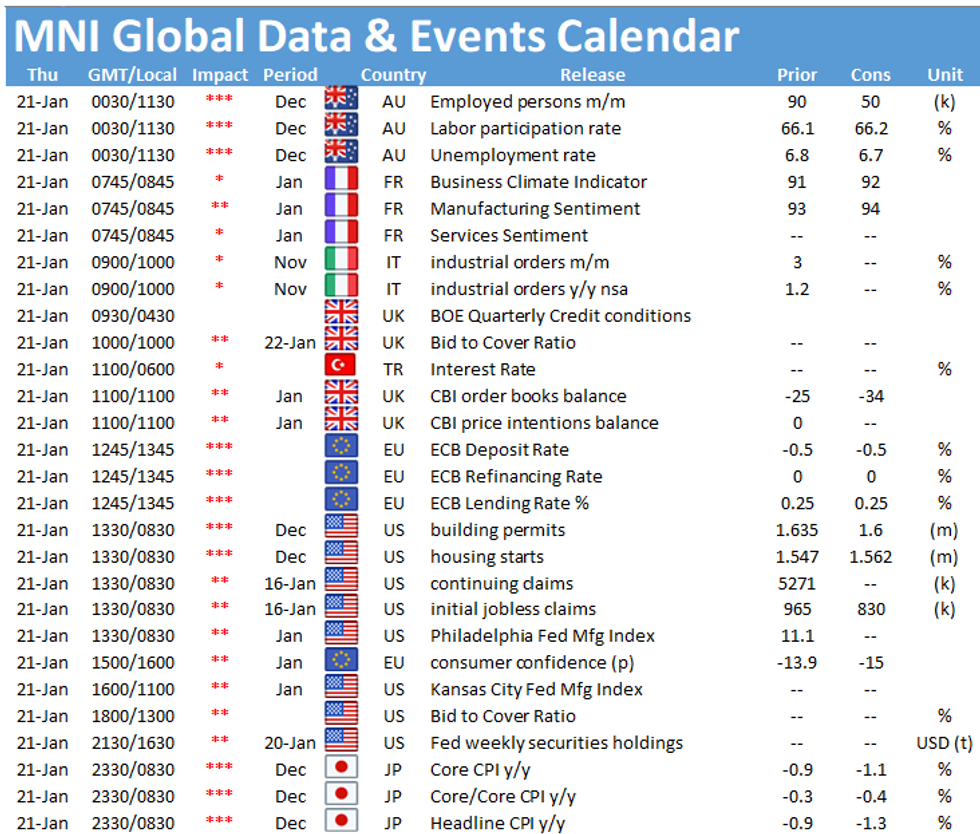

OVERNIGHT DATA

US NAHB HOUSING MARKET INDEX 83 IN JAN

US NAHB JAN SINGLE FAMILY SALES INDEX 90; NEXT 6-MO 83

US REDBOOK: JAN STORE SALES -2.5% V DEC THROUGH JAN 16 WK

US REDBOOK: JAN STORE SALES +2.2% V YR AGO MO

US REDBOOK: STORE SALES +2.2% WK ENDED JAN 16 V YR AGO WK

US MBA: MARKET COMPOSITE -1.9% SA THRU JAN 15 WK

US MBA: 30-YR CONFORMING MORTGAGE RATE 2.92% VS 2.88% PREV

US MBA: UNADJ PURCHASE INDEX +15% VS YEAR-EARLIER LEVEL

US MBA: REFIS -5% SA; PURCH INDEX +3% SA THRU JAN 15 WK

BANK OF CANADA LEAVES KEY INTEREST RATE AT 0.25%

BANK OF CANADA KEEPS QE PACE OF AT LEAST CAD4B A WEEK

MARKETS SNAPSHOT

- DJIA up 251.64 points (0.81%) at 31165.38

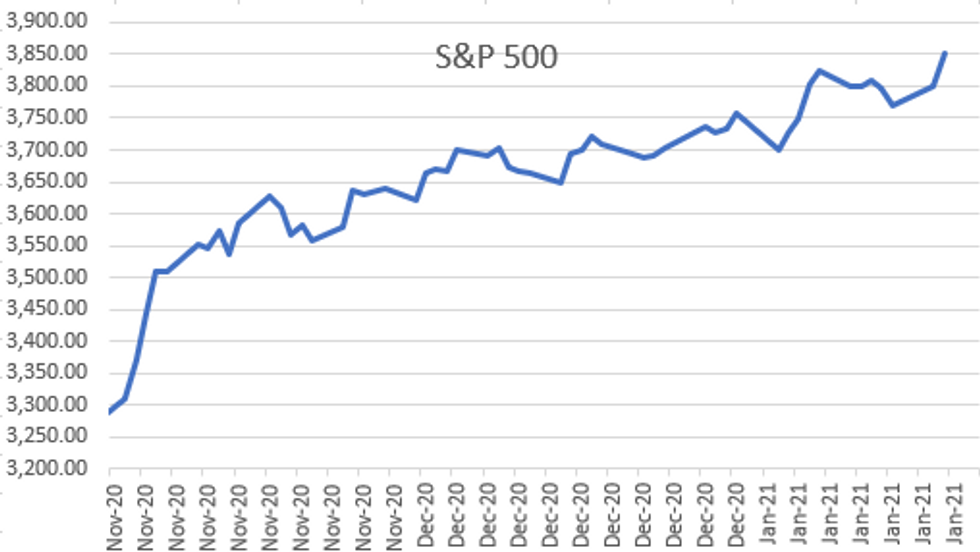

- S&P E-Mini Future up 57.5 points (1.52%) at 3846

- Nasdaq up 283.9 points (2.2%) at 13464.97

- US 10-Yr yield is down 0.2 bps at 1.087%

- US Mar 10Y are up 0.5/32 at 136-30.5

- EURUSD down 0.0024 (-0.2%) at 1.2106

- USDJPY down 0.38 (-0.37%) at 103.57

- WTI Crude Oil (front-month) up $0.26 (0.49%) at $53.18

- Gold is up $28.83 (1.57%) at $1867.43

- EuroStoxx 50 up 28.62 points (0.8%) at 3624.04

- FTSE 100 up 27.44 points (0.41%) at 6740.39

- German DAX up 106.31 points (0.77%) at 13921.37

- French CAC 40 up 29.83 points (0.53%) at 5628.44

US TSY SUMMARY

Rates reversed early losses, finished near modest session highs Wednesday, even as equities climbed to new all-time highs, ESH1 3850.0. Relative modest volumes and quiet trade as markets preoccupied with President Biden/VP Harris inauguration, a seemingly all-day affair that started with Pres Trump's early WH exit.

- Decent volumes on two-way trade in the first half gave way to better buying in the lead up to the US Tsy 20Y Bond auction re-re-open, long end extending session highs briefly. Pick-up in corp debt issuance, return of domestic banks generated two-way hedging.

- Rates gapped lower after weak auction: US Tsy $24B 20Y bond auction re-re-open (912810ST6) tailed 1.2bp: high yield of 1.657% (1.470% last month) vs. 1.645% WI, on a bid/cover 2.28% (2.39% previous).

- Heavy second half selling in Eurodollar lead quarterly futures -60k EDH1 at 99.81(-0.005); Block: 10,000 Green packs (EDH3-EDZ3), -0.0075 at 0914:10ET, paper focus on sector since late 2020. 10k Old Red packs (EDZ2-EDU3) blocked last Friday while option accounts have been building large rate hike insurance positions via buying puts

- The 2-Yr yield is down 0.4bps at 0.127%, 5-Yr is up 0.2bps at 0.447%, 10-Yr is down 0.2bps at 1.087%, and 30-Yr is up 0.5bps at 1.8388%.

US TSY FUTURES CLOSE

Tsy futures held mildly higher levels by the closing bell, but continued to extend duration heading into the equity close with stocks making new highs (ESH1 3852.5). Moderate volumes with market preoccupied with Pres Biden inauguration. Choppy post 20Y Bond auction trade, futures gapped lower after 20Y re-re-open tailed 1.2bp. Large 2s5s steepener block earlier: +19,968 TUH 110-14.25 vs. -12,793 FVH 125-23.

- 3M10Y -0.761, 99.736 (L: 99.567 / H: 102.035)

- 2Y10Y -0.613, 94.946 (L: 94.776 / H: 96.894)

- 2Y30Y -0.299, 169.781 (L: 169.457 / H: 171.901)

- 5Y30Y -0.615, 138.304 (L: 137.904 / H: 139.895)

- Current futures levels:

- Mar 2Y up 0.125/32 at 110-14.875 (L: 110-14.25 / H: 110-15)

- Mar 5Y up 0.75/32 at 125-25.25 (L: 125-22.5 / H: 125-25.5)

- Mar 10Y up 2.5/32 at 137-0.5 (L: 136-25.5 / H: 137-01)

- Mar 30Y up 9/32 at 169-8 (L: 168-21 / H: 169-10)

- Mar Ultra 30Y up 12/32 at 206-5 (L: 205-04 / H: 206-09)

US EURODOLLAR FUTURES CLOSE:

Futures holding steady to mostly weaker across the strip after the bell, heavy second half volume in short end: over 60k EDH1 at 99.81 (-0.005). 3M LIBOR settled -0.00125 to 0.22238% (-0.00100/wk). Current levels:

- Mar 21 -0.005 at 99.810

- Jun 21 steady at 99.825

- Sep 21 -0.005 at 99.815

- Dec 21 steady at 99.785

- Red Pack (Mar 22-Dec 22) -0.005 to steady

- Green Pack (Mar 23-Dec 23) -0.005 to steady

- Blue Pack (Mar 24-Dec 24) -0.005

- Gold Pack (Mar 25-Dec 25) steady to +0.005

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N +0.00150 at 0.08663% (+0.00000/wk)

- 1 Month -0.00100 to 0.12850% (-0.00100/wk)

- 3 Month -0.00125 to 0.22238% (-0.00100/wk)

- 6 Month +0.00200 to 0.23788% (-0.01025/wk)

- 1 Year +0.00425 to 0.31725% (-0.00538/wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $61B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $162B

- Secured Overnight Financing Rate (SOFR): 0.07%, $936B

- Broad General Collateral Rate (BGCR): 0.05%, $350B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $323B

- (rate, volume levels reflect prior session)

- TIPS 1Y-7.5Y, $2.401B accepted vs. $7.983B submission

- Next scheduled purchases:

- Thu 1/21 1010-1030ET: Tsy 7Y-20Y, appr $3.625B

- Fri 1/22 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.825B

PIPELINE: Domestic Bank Issuance Returning

- Date $MM Issuer (Priced *, Launch #)

- 01/20 $7.5B #Morgan Stanley $3B 3NC2 +40, $2.5B 11.25NC10.25 fix/FRN +85, $2B 31NC30 fix/FRN +97

- 01/20 $5.5B #Goldman Sachs $2.25B 2NC1 +35, $750M 2NC1 FRN SOFR+41, $2.5B 11NC10 fix/FRN +90

- 01/20 $3B *Asia Infrastructure Inv Bank (AIIB) 5Y +6

- 01/20 $2.45B #Panama 2032 tap +112, 2060 tap +155

- 01/20 $2B *Gazprom 8Y 2.95%

- 01/20 $2B #Kingdom of Bahrain $500M 7Y 4.25%, $1B 12Y 5.25%, $500M 30Y 6.25%

- 01/20 $1B *QNB Finance (Qatar National Bank) 5Y +95

- 01/20 $450M *Korean Southern Power 5Y +40

- Next on tap:

- 01/21 $1B Kommunekredit WNG 5Y +9

- 01/21 $1B Canada Pension Plan Inv Brd (CPPIB) 10Y +25a

- 01/21 $Benchmark European Bank for R&D (EBRD) 5Y +5a

- 01/?? $Benchmark SK Innovations 3Y +150a, 5Y +175a

FOREX: Haven FX Hit as Biden Assumes Office

Haven currencies were sold Wednesday, with CHF, USD and JPY trading poorly as equities globally rallied in response to the smooth inauguration of Joe Biden as the 46th President of the US.

- EUR also traded poorly, undoing much of the Tuesday rally to zero in on the week's lows at 1.2054, but a resumption of USD weakness kept the technical picture in tact. Nonetheless, the bearish risk clearly remains present, allowing overbought conditions to unwind.

- While the Bank of Canada kept rates unchanged, CAD managed to hit new multi-year highs vs. the USD at 1.2606 as the Bank declined to utilise any form of 'micro' cut to interest rates to manage policy. The Bank also appeared upbeat on growth in the second half of 2021, leaving unchanged as the most likely path for policy at this juncture.

- Focus Thursday turns to Australia's December jobs report, weekly US jobless claims data and central bank decisions from Japan, Indonesia, the Eurozone, South Africa and Turkey.

EGBs-GILTS CASH CLOSE: BTP Retrace, ECB Eyed Thursday

BTPs were the focal point again Wednesday, with spreads widening in a "buy the rumour, sell the fact"-type move following PM Conte's successful survival of confidence votes Monday and Tuesday.

- Bunds saw little movement, while Gilts underperformed amid bear steepening. Before the open, UK Dec inflation data surprised to the upside.

- Though no change is expected, ECB decision/presser is the focal point Thursday; contact us if you haven't seen the MNI Preview. We also get supply from Spain, France, and the UK. Closing levels/10-Yr Periphery EGB spreads/Bunds:

- Germany: The 2-Yr yield is down 0.3bps at -0.71%, 5-Yr is down 0.6bps at -0.722%, 10-Yr is down 0.3bps at -0.529%, and 30-Yr is down 0.4bps at -0.118%.

- UK: The 2-Yr yield is up 1bps at -0.117%, 5-Yr is up 0.8bps at -0.033%, 10-Yr is up 1.2bps at 0.301%, and 30-Yr is up 2.2bps at 0.881%.

- Italian BTP spread up 3.4bps at 114.8bps / Spanish spread up 0.9bps at 60.4bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.