Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI BRIEF: White House Rejects Splitting USD1.9T Covid Plan

- MNI INTERVIEW: ECB May Be In Liquidity Trap-Bank Of Greece No2

- MNI BRIEF: Europe May Need Fiscal Leeway In 2020: Gentiloni

- COVID VARIANT FROM SOUTH AFRICA DIAGNOSED IN SOUTH CAROLINA: AP

- GERMANY RECOMMENDS ASTRAZENECA SHOT ONLY FOR 18-64 YEAR OLDS, Bbg

- ROBINHOOD RESTRICTIONS APPLY TO GME, AMC, BB, BBBY, NOK, OTHERS ... ADDS AAL, CTRM, SNDL, OTHERS TO RESTRICTED TRADING, Bbg

US

US: The White House on Thursday said it is not looking to break up President Joe Biden's USD1.9 trillion Covid relief plan into two pieces despite growing skepticism from Republicans and moderate Democrats who have raised questions about the timing and size of the plan.

- Biden's director of the National Economic Council, Brian Deese, said the proposal "can't be done piecemeal." White House spokesperson Jen Psaki wrote on twitter: "We are engaging with a range of voices...we aren't looking to split a package in two."

US: Q4 GDP increased at an annual rate of 4.0%, slightly lower than expectations for an annualized increase of 4.2%. 3Q GDP was unrevised at 33.4%.

- That reflects increases in exports (+22.0%), nonresidential fixed investment (+13.8%), PCE (+2.5%), and residential fixed investment(+33.5%), the Bureau of Economic Analysis said Thursday.

- That was partially offset by declines in state and local government spending (-1.7%), and federal government spending (-0.5%).

- Current-dollar GDP was up an annualized 6.0% in Q4 following a 38.3% increase in Q3.

- The GDP price index increased 1.7% after a 3.3% in Q3. The PCE price index was up 1.5% following a larger 3.7% increase in the previous quarter.

EUROPE

EU: European policymakers should be careful that the significant fiscal policy response to the Covid-19 crisis isn't phased out prematurely, EU Commissioner for the Economy Paolo Gentiloni said Thursday, meaning any ideas that surfaced back in the Autumn about un-triggering the General Escape Clause, set to expire at the end of the year, may need to be reevaluated.

GREECE: The European Central Bank may have lost its ability to boost inflation via monetary policy, the deputy governor of the Central Bank of Greece told MNI in an interview, saying the eurozone was in secular stagnation and that the only way to boost aggregate demand was via public spending.

- "Monetary policy seems to have reach[ed] limits as interest rates are close to the zero lower bound, meaning that monetary policy cannot currently set [the] inflation rate," Theodore Pelagidis said in emailed responses to questions. "In the context of a severe, Covid-led, economic downturn, monetary policy might be ineffective."

OVERNIGHT DATA

- US JOBLESS CLAIMS -67K TO 847K IN JAN 23 WK

- US CONTINUING CLAIMS -0.203M TO 4.771M IN JAN 16 WK

- US DEC ADVANCE WHOLESALE INVENTORIES +0.1%, $650.4B VS NOV $649.6B

- US DEC ADVANCE RETAIL INVENTORIES +1.0%, $624.1B VS NOV $617.7B

- US 4Q ADV CHANGE IN PRIVATE INVENTORIES +$44.6B V 3Q -$3.7B

- US DEC ADVANCE INTL TRADE BALANCE -3.5%; -$82.5B VS NOV -$85.5B

- US 4Q ADV PCE 2.5% VS 3Q 41.0% (3.1% EXPECTED)

- US 4Q GDP ADV EST 4.0% VS 4.2% EXP; Q3 33.4%

- US 4Q ADV GDP FINAL SALES +3.0% V 3Q +25.9%

- US DEC. INDEX OF LEADING ECONOMIC INDICATORS UP 0.3%

- US Conference Board Dec Leading Index +0.3%

- US Conference Board: Dec Leading Index 109.5

- US Dec New Home Sales +1.6% To 842K; Consensus 875K

- US Nov New Home Sales Revised To 829K From 841K

- US Nov New Home Sales Supply At 4.3 Months

- U.S. JAN. KANSAS CITY FED MANUFACTURING ACTIVITY AT 17

- CANADIAN DEC BUILDING PERMITS -4.1% MOM

- CANADA RESIDENTIAL BUILDING PERMITS -0.9%; NON-RESIDENTIAL -10.8%

MARKET SNAPSHOT

Key late session market levels:

- DJIA up 488.06 points (1.61%) at 30792.1

- S&P E-Mini Future up 66.25 points (1.77%) at 3810.25

- Nasdaq up 193.7 points (1.5%) at 13463.81

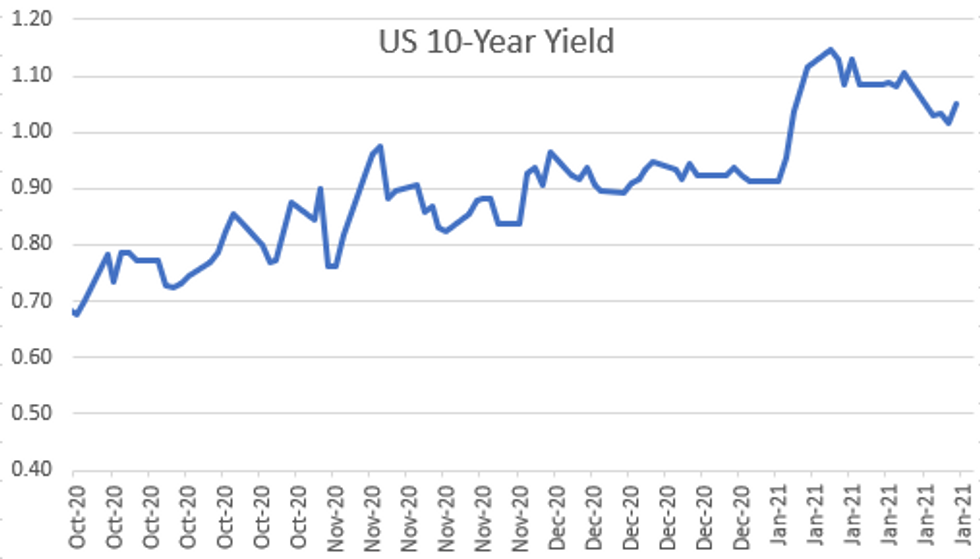

- US 10-Yr yield is up 4.4 bps at 1.0602%

- US Mar 10Y are down 10.5/32 at 137-6.5

- EURUSD up 0.0026 (0.21%) at 1.2138

- USDJPY up 0.08 (0.08%) at 104.19

- WTI Crude Oil (front-month) down $0.55 (-1.04%) at $52.29

- Gold is down $1.09 (-0.06%) at $1842.85

- EuroStoxx 50 up 20.66 points (0.58%) at 3557.04

- FTSE 100 down 41.22 points (-0.63%) at 6526.15

- German DAX up 45.47 points (0.33%) at 13665.93

- French CAC 40 up 50.9 points (0.93%) at 5510.52

US TSY SUMMARY

Rates finish broadly weaker after a stronger start, off late session lows after the bell. Story of tail wags dog. After a slight delay, Tsy futures pared gains in long end after weekly claims drops 67k to 847k, drew more selling on heels of Q4 GDP (+4.0 vs. +4.2% est), Advance Goods Trade Balance is a deficit ($82.5B vs. $84B est), Wholesale Inventories (+0.1% MoM vs. +0.5% est).

- But it wasn't until word that brokers Robinhood and Interactive Brokers would crack down on trading of high-flyer single lists that have seen massive surges in prices and volume this week that risk appetite surged, Tsys falling sharply as equity indexes rebounded from Wed's sharp rout (eminis +1.33% after falling more than 3% late Wed). "ROBINHOOD RESTRICTIONS APPLY TO GME, AMC, BB, BBBY, NOK, OTHERS" .. "ADDS AAL, CTRM, SNDL, OTHERS TO RESTRICTED TRADING," Bbg, Seante and House reps both to launch hearings.

- Futures continue to slide lower across the board, back near middle of range traded from Jan 14-22; 10YY +.0475 to 1.0636% day after breaching 1.0% (0.9992% low Wed; 30YY +.0565, 1.8305%. Yield curves back near early Jan/multi-year highs.

- Little react after decent 7Y Auction: Record US Tsy $62B 7Y Note auction (91282CBJ9) stopped through: draws high yield 0.754% (0.662% last month) vs. 0.757% WI; 2.30 bid/cover vs. 2.31 prior.

- The 2-Yr yield is unchanged at 0.1191%, 5-Yr is up 1.7bps at 0.4288%, 10-Yr is up 3.4bps at 1.05%, and 30-Yr is up 3.8bps at 1.8115%.

MONTH-END EXTENSIONS: FINAL Barclays/Bbg Extension Estimates

Forecast summary compared to the avg increase for prior year and the same time in 2020. TIPS -0.16Y; Govt inflation-linked, 0.23.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.09 | 0.10 | 0.07 |

| Agencies | 0.16 | 0.05 | -0.03 |

| Credit | 0.09 | 0.12 | 0.09 |

| Govt/Credit | 0.09 | 0.10 | 0.07 |

| MBS | 0.06 | 0.08 | 0.07 |

| Aggregate | 0.08 | 0.09 | 0.08 |

| Long Gov/Cr | 0.09 | 0.09 | 0.05 |

| Iterm Credit | 0.1 | 0.10 | 0.09 |

| Interm Gov | 0.09 | 0.09 | 0.07 |

| Interm Gov/Cr | 0.09 | 0.09 | 0.08 |

| High Yield | 0.11 | 0.12 | 0.09 |

US TSY FUTURES CLOSE

Tsy futures trading weaker after a firmer start -- yields rebound as equities recover slightly from Wed's rout. Yld curves bear steepening back near early January multi-year highs.

- 3M10Y +4.832, 99.088 (L: 91.977 / H: 100.704)

- 2Y10Y +3.198, 92.698 (L: 87.306 / H: 94.738)

- 2Y30Y +3.349, 168.571 (L: 163.223 / H: 171.305)

- 5Y30Y +1.417, 137.68 (L: 134.512 / H: 139.534)

- Current futures levels:

- Mar 2Y down 0.5/32 at 110-15.25 (L: 110-15.25 / H: 110-15.875)

- Mar 5Y down 3.25/32 at 125-29.5 (L: 125-27.75 / H: 126-01)

- Mar 10Y down 9/32 at 137-8 (L: 137-04 / H: 137-19)

- Mar 30Y down 25/32 at 169-21 (L: 169-06 / H: 170-29)

- Mar Ultra 30Y down 1-9/32 at 206-20 (L: 205-15 / H: 208-28)

US EURODOLLAR FUTURES CLOSE

Long end of strip underperforming steady to marginally higher levels at points in Whites-Reds, heavy volume session with Massive 59,660 EDH1 Block buy at 99.83, 8k 2Y bundles Blocked -0.0025. Lead quarterly EDH1 holds steady after the bell, bouncing after 3M LIBOR set -0.00650 to 0.20500% (-0.01025/wk) -- just off record Low 0.20488% from 11/20/20.

- Mar 21 steady at 99.825

- Jun 21 +0.005 at 99.840

- Sep 21 +0.005 at 99.830

- Dec 21 steady at 99.790

- Red Pack (Mar 22-Dec 22) -0.01 to +0.005

- Green Pack (Mar 23-Dec 23) -0.03 to -0.015

- Blue Pack (Mar 24-Dec 24) -0.045 to -0.03

- Gold Pack (Mar 25-Dec 25) -0.055 to -0.045

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N -0.00363 at 0.07925% (-0.00700/wk)

- 1 Month -0.00213 to 0.12288% (-0.00187/wk)

- 3 Month -0.00650 to 0.20500% (-0.01025/wk) ** 3M New record Low 0.20488% on 11/20/20

- 6 Month -0.00750 to 0.22013% (-0.01587/wk)

- 1 Year -0.00125 to 0.31075% (-0.00150/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $74B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $213B

- Secured Overnight Financing Rate (SOFR): 0.03%, $913B

- Broad General Collateral Rate (BGCR): 0.02%, $353B

- Tri-Party General Collateral Rate (TGCR): 0.02%, $325B

- (rate, volume levels reflect prior session)

- Tsy 20Y-30Y, $1.735B accepted vs. $5.779B submission

- Next scheduled purchase:

- Fri 1/29 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Fri 01/29 Next forward schedule release at 1500ET

PIPELINE: JP Morgan Launched

JP Morgan outpaces Cargill, Airport Authority HK combined.

- Date $MM Issuer (Priced *, Launch #)

- 01/28 $5B #JP Morgan $2B 6NC5 fix/FRN +62, $3B 11NC10 fix/FRN +90

- 01/28 $1.5B #Cargill $500M 3Y +25, $500M 5Y +40, $500M 10Y +65

- 01/28 $1.5B #Airport Authority HK $900M 10Y +65, $600M 30Y +80

- 01/?? $Benchmark IDB 5Y +5a

FOREX: USD Gives Up Early Gains, JPY Sinks To Lowest Since Early Dec

The greenback traded well for the first half of the Thursday session, before a short, sharp spell of risk-on worked against the USD, spurring the USD index to sink into negative territory ahead of the close. The USD sales spurred EUR/USD briefly back above 1.2140, despite further stressing from the ECB that a rate cut is not off the table if the circumstances change.

- JPY was comfortably the poorest performer Thursday, with USD/JPY cracking through major resistance at the bear channel top of 104.40 (drawn from the March 2020 high). This confirms a resumption of the uptrend that started at the beginning of January and opens levels not seen since November.

- Focus Friday turns to French, German and Canadian GDP releases and US personal income/spending figures for December. The first Fed speakers since Wednesday's FOMC decision are due, with Kaplan and Daly both on the docket.

EGBs-GILTS CASH CLOSE: Reversal Of Fortune

Another busy session Thursday, with risk appetite swinging from negative to positive from early afternoon onward. The German and UK curves went from bull flattening to bear steepening, while BTP spreads narrowed after initial widening.

- In data, Germany had an upside inflation shocker in January (on base effects/changing basket weighting); earlier, Eurozone confidence figures modestly beat expectations. Friday sees some key Eurozone Q4 prelim GDP figures.

- Some AstraZeneca vaccine headlines garnered attention (Germany potentially recommending shouldn't be given to over 65s).

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.4bps at -0.745%, 5-Yr is down 0.1bps at -0.752%, 10-Yr is up 0.7bps at -0.539%, and 30-Yr is up 1.5bps at -0.101%.

- UK: The 2-Yr yield is up 1.8bps at -0.113%, 5-Yr is up 1.3bps at -0.042%, 10-Yr is up 1.8bps at 0.287%, and 30-Yr is up 1.8bps at 0.85%.

- Italian BTP spread down 2.6bps at 117.5bps

- Spanish bond spread down 0.8bps at 61.2bps

- Portuguese PGB spread down 1bps at 55.7bps

- Greek bond spread down 0.3bps at 122.1bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.