Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: FOMC MINUTES: ECONOMY STILL FAR FROM FED'S GOALS

- FED: LIKELY SOME TIME FOR SUBSTANTIAL FURTHER PROGRESS ACHIEVED

- MNI BRIEF: Some Fed Members Flag More Balanced Inflation Risks

- MNI BRIEF: Fed to Rely On IOER, ONRRP to Control Rates-Minutes

- U.S. Attorney's Office and FBI Obtained Seizure Warrants Authorizing FBI to Seize Cryptocurrency Stolen by North Korean Hackers, DJ

US

FOMC MINUTES: Minutes from the Fed's January meeting showed "participants generally viewed the risks to the outlook for inflation as having become more balanced" even if most still see overall risks as tilted downward.

- "As an upside risk to inflation, several participants noted the potential for pandemic-related supply constraints to affect price inflation somewhat more than anticipated or for price increases among industries most adversely affected by the pandemic to be more pronounced than projected," the minutes said.

OVERNIGHT DATA

- US JAN FINAL DEMAND PPI +1.3%, EX FOOD, ENERGY +1.2%

- US JAN FINAL DEMAND PPI EX FOOD, ENERGY, TRADE SERVICES +1.2%

- US JAN FINAL DEMAND PPI Y/Y +1.7%, EX FOOD, ENERGY Y/Y +2.0%

- US JAN PPI: FOOD +0.2%; ENERGY +5.1%

- US JAN PPI: GOODS +1.4%; SERVICES +1.3%; TRADE SERVICES +1.0%

- US JAN RETAIL SALES & FOOD SVCS +5.3%; EX-MOTOR VEH +5.9%

- US DEC SALES REVISED -1.0%; EX-MV -1.8%

- US JAN RET SALES EX GAS & MTR VEH & PARTS DEALERS +6.1% V DEC -2.5%

- US JAN RET SALES EX MTR VEH & PARTS DEALERS +5.9% V US JAN -1.8%

- US JAN RET SALES EX AUTO, BLDG MATL & GAS +12.7% V DEC -2.7%

- US REDBOOK: FEB STORE SALES -0.9% V JAN THROUGH FEB 13 WK

- US REDBOOK: FEB STORE SALES +2.4% V YR AGO MO

- US REDBOOK: STORE SALES +4.0% WK ENDED FEB 13 V YR AGO WK

- US JAN INDUSTRIAL PROD +0.9%; CAP UTIL 75.6%

- US DEC IP REV TO +1.3%; CAP UTIL REV 74.9%

- US JAN MFG OUTPUT +1.0%

- US DEC BUSINESS INVENTORIES +0.6%; SALES +0.8%

- US DEC RETAIL INVENTORIES +1.2%

- US NAHB HOUSING MARKET INDEX 84 IN FEB

- US NAHB FEB SINGLE FAMILY SALES INDEX 90; NEXT 6-MO 80

- CANADIAN JAN CONSUMER PRICE INDEX INFLATION +1.0% YOY

- CANADA MOM CPI INFLATION WAS +0.6% IN JAN

MARKET SNAPSHOT

Key late session market levels:

- DJIA up 88.48 points (0.28%) at 31611.15

- S&P E-Mini Future down 4.5 points (-0.11%) at 3923.25

- Nasdaq down 110.4 points (-0.8%) at 13937.92

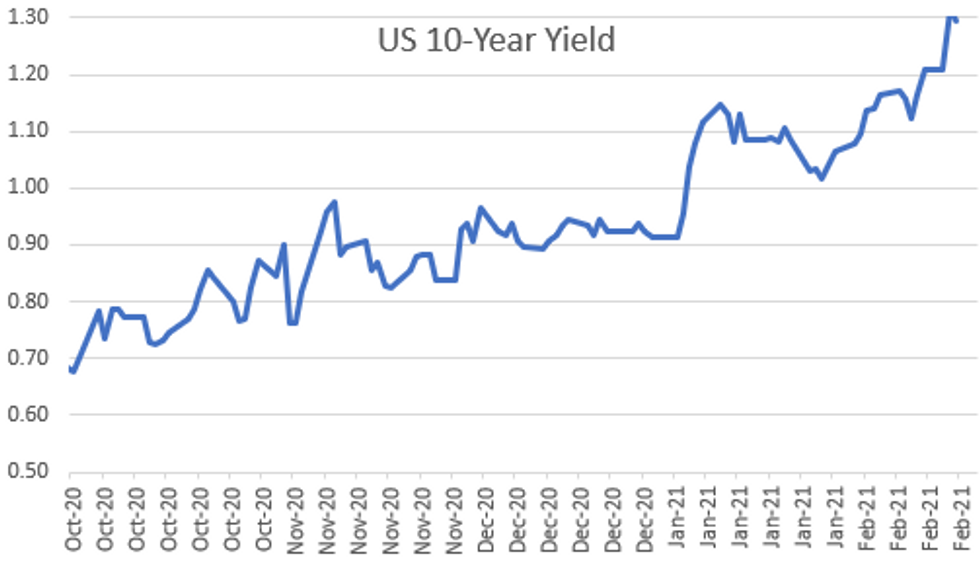

- US 10-Yr yield is down 2.2 bps at 1.2922%

- US Mar 10Y are down 0.5/32 at 135-24.5

- EURUSD down 0.0068 (-0.56%) at 1.2038

- USDJPY down 0.13 (-0.12%) at 105.91

- WTI Crude Oil (front-month) up $1.11 (1.85%) at $61.14

- Gold is down $21.72 (-1.21%) at $1772.48

- EuroStoxx 50 down 26.55 points (-0.71%) at 3699.85

- FTSE 100 down 37.96 points (-0.56%) at 6710.9

- German DAX down 155.33 points (-1.1%) at 13909.27

- French CAC 40 down 20.69 points (-0.36%) at 5765.84

US TSY SUMMARY: Good Data, Positive For Rates?

Tsy trading mostly higher, 10Y back to steady after the bell. Tsys sold off post minutes, back near post 20Y AND pre-early session data levels. After trading lower on better than expected data (aside from revisions, and taking yesterday's move into account) it appears sentiment is back to "good data is bad" as it lowers probability of $1.X trillion fiscal stimulus on the margins.- Quick takeaways, Fed remains accommodative as some see near term downside risks eco-outlook and conditions, Covid-19 metrics remain "important". Upside risks, fiscal policy could be more robust, financial market utilities could display greater propensity toward higher spending.

- Treasuries gap lower after WEAK US Tsy $27B 20Y bond auction (912810SW9) draws 1.920% vs. 1.897% WI, bid/cover 2.15% (2.28% previous).

- Choppy day for Tsy yld curves, mildly flatter after bear steepening Tue. Heavy session volumes in 2s-10s March/June rolls ahead Feb 26 first notice: TUH/TUM w/82k, FVH/FVM w/99k, TYH/TYM w/67k.

- TYH1 hit resistance: 135-30.5H (+5.5) just below initial resistance of 136-01, Jan 12 low -- trend remains down.

- The 2-Yr yield is down 1.2bps at 0.1069%, 5-Yr is down 1.4bps at 0.5593%, 10-Yr is down 2.2bps at 1.2922%, and 30-Yr is down 3.1bps at 2.0608%.

US TSY FUTURES CLOSE

Futures mostly higher after the bell, TYH1 steady after rejecting resistance (136-01) before 20Y auction tailed, spurring further selling. Not much of a react to Jan FOMC minutes.

- 3M10Y -2.02, 125.08 (L: 122.637 / H: 128.627)

- 2Y10Y -1.123, 117.987 (L: 115.597 / H: 121.001)

- 2Y30Y -1.916, 194.966 (L: 191.701 / H: 198.9)

- 5Y30Y -1.72, 149.935 (L: 147.536 / H: 152.595)

- Current futures levels:

- Mar 2Y up 0.75/32 at 110-16 (L: 110-15 / H: 110-16.25)

- Mar 5Y up 1.25/32 at 125-13.75 (L: 125-07.5 / H: 125-15.5)

- Mar 10Y up 1/32 at 135-26 (L: 135-15 / H: 135-30.5)

- Mar 30Y up 15/32 at 164-18 (L: 163-17 / H: 165-02)

- Mar Ultra 30Y up 1-0/32 at 196-25 (L: 194-28 / H: 197-31)

US EURODOLLAR FUTURES CLOSE

Short end remains well bid after 3M LIBOR fell to new record low: -0.00725 to 0.18138% (-0.01237/wk; prior: 0.18863% on 2/16/21), support extending through front half of Blues in second half.

- Mar 21 +0.010 at 99.840

- Jun 21 +0.015 at 99.850

- Sep 21 +0.015 at 99.835

- Dec 21 +0.010 at 99.790

- Red Pack (Mar 22-Dec 22) +0.020 to +0.015

- Green Pack (Mar 23-Dec 23) +0.015 to +0.010

- Blue Pack (Mar 24-Dec 24) +0.005 to -0.015

- Gold Pack (Mar 25-Dec 25) -0.02 to -0.03

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N -0.00087 at 0.08063% (+0.00100/wk)

- 1 Month +0.00275 to 0.11100% (+0.00362/wk)

- 3 Month -0.00725 to 0.18138% (-0.01237/wk) ** New Record Low (prior: 0.18863% on 2/16/21)

- 6 Month -0.00488 to 0.19775% (-0.00300/wk)

- 1 Year -0.00650 to 0.29613% (-0.00362/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $65B

- Daily Overnight Bank Funding Rate: 0.07%, volume: $201B

- Secured Overnight Financing Rate (SOFR): 0.06%, $934B

- Broad General Collateral Rate (BGCR): 0.04%, $372B

- Tri-Party General Collateral Rate (TGCR): 0.04%, $337B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, $1.201B accepted vs. $2.241B submission

- Next scheduled purchases:

- Thu 2/18 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Fri 2/19 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.825B

PIPELINE: Rabobank, NextEra Launched, Ontario Expected Thu

- Date $MM Issuer (Priced *, Launch #)

- 02/17 $1.65B #NextEra Energy Capital 2NC.5 FRN 3M LIBOR +27

- 02/17 $1B #Rabobank 6NC5 +55

- Rolled to Thursday:

- 02/18 $Benchmark Prov of Ontario 10Y +27a

FOREX: Sagging Sentiment Sees USD/JPY Sink Off 2021 Highs

JPY traded well, prompting USD/JPY to edge lower for the first session in five as the equity rally stalled and stock markets edged lower. Crosses including EUR/JPY and AUD/JPY saw decent momentum unwinds, but there are few signs yet of a meaningful bearish reversal.

- A combination of firm US retail sales and bearish technical signals sent EUR/USD to the lowest levels of the week. Bears watch Tuesday's candle pattern for confirmation of a bearish shooting star which, if confirmed could open declines toward the 100-dma, which crossed at 1.2000 Wednesday.

- Elsewhere, commodity-tied currencies slipped, with the NOK underperforming all others in G10 as oil prices were bumped lower. The WSJ reported that Saudi Arabia are to notify OPEC that they will reverse recent oil output cuts as soon as April given the recent recovery in prices. USD/NOK rallied smartly before stalling ahead of the 8.5604 50-dma.

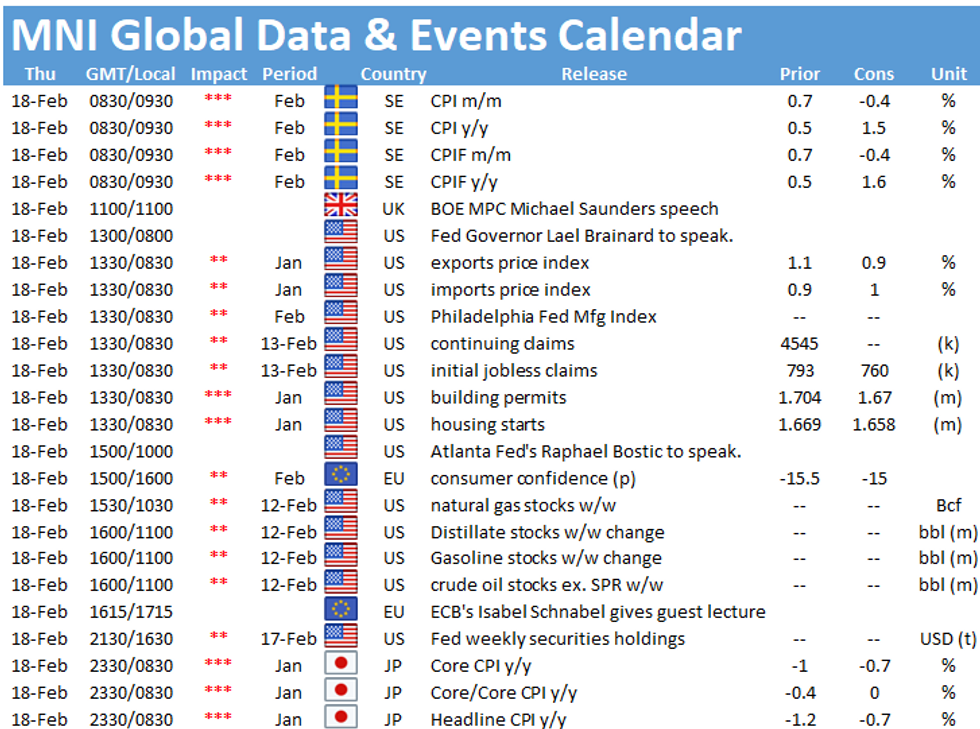

- Focus Thursday turns to weekly US jobless claims and housing starts/building permits, Australia's January jobs report and rate decisions from the Turkish and Indonesian central banks.

BONDS: EGBs-GILTS CASH CLOSE: Core Selloff Pauses; BTPs Fade

In direct contrast with Tuesday, Wednesday saw Gilt and Bund yields close at/near session lows, with global safe havens in favor as equities retreated and the US dollar strengthened. The German and UK curves bull flattened. Against that backdrop, BTP spreads headed to widest levels to Bunds in four sessions.

- Pre-open, UK CPI pushed higher in January and came in above expectations.

- Germany sold 30Yr Bund (E1.2bn allotted) at a positive yield for the first time since June; UK sold EGB2.5bn of Jul-35 Gilt. Toward the end of the session, BOE's Ramsden noted the BOE has room to increase QE further.

- Thursday's data fairly thin, including Eurozone consumer confidence. Meanwhile, the ECB publishes its policy meeting account, while BOE's Saunders speaks on a webinar. Spain and France hold auctions.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.8bps at -0.698%, 5-Yr is down 1.6bps at -0.65%, 10-Yr is down 2bps at -0.368%, and 30-Yr is down 2.6bps at 0.137%.

- UK: The 2-Yr yield is down 0.7bps at -0.044%, 5-Yr is down 2bps at 0.107%, 10-Yr is down 4.9bps at 0.572%, and 30-Yr is down 6.9bps at 1.154%.

- Italian BTP spread up 3.4bps at 95.4bps / Spanish spread up 1.4bps at 65.6bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.