Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

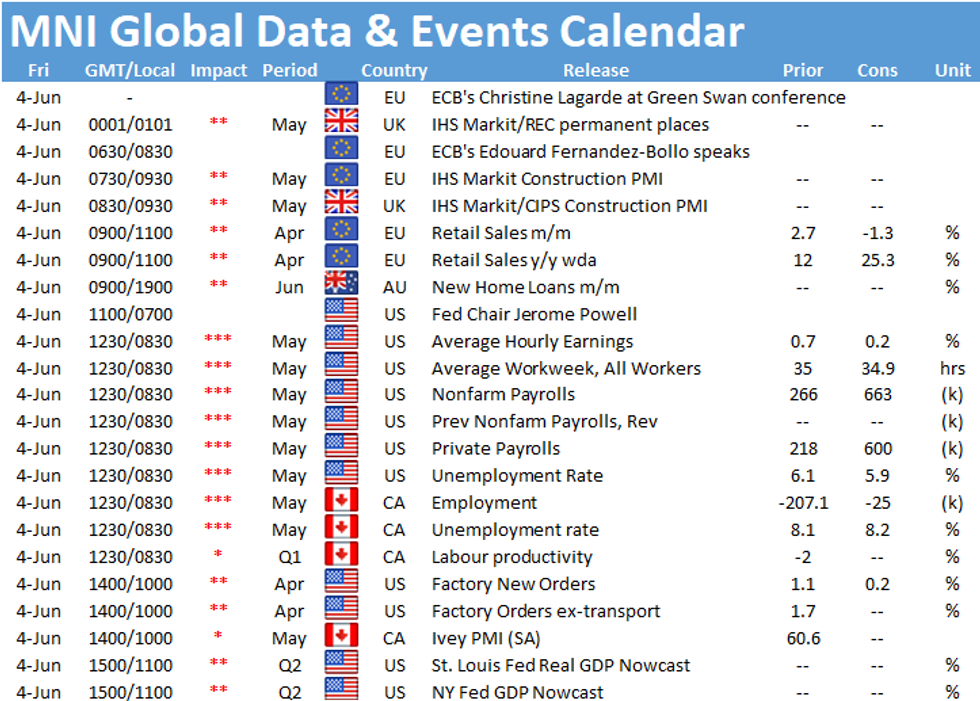

MNI INTERVIEW: Job Market Progress May Be Rocky -Fed Economist

MNI REALITY CHECK: US Labor Shortage Still Hampering Job Gains

MNI BRIEF: Fed's Quarles Rejects Call For CCyB

US

FED: The U.S. economy is more likely than not to have seen robust hiring in May, but another disappointing payrolls number Friday could indicate structural changes facing the labor market could pose a bigger challenge than thought, Richmond Fed senior adviser Thomas Lubik told MNI.

- At the moment Lubik remains "cautiously optimistic" of new jobs in the 600,000 to 700,000 range in May and that April's shockingly low 266,000 payrolls figure will be revised upward.

- But increased automation, a shift to e-commerce and decline in business travel are among forces reshuffling the types of jobs and skills in demand after the Covid-19 pandemic. They exacerbate existing challenges of matching workers who lost their jobs during the crisis to new vacancies, and could portend a more prolonged recovery, Lubik warned in an interview Wednesday. For more see MNI Policy main wire at 1250ET.

- The Fed's announcement Wednesday that it would begin winding down its Secondary Market Corporate Credit Facility (SMCFF) is a symbolic step toward post-pandemic policy normalization, but will have little significant broader market impact.

- The SMCFF (which provided liquidity for outstanding corporate bonds) and its primary market equiv PMCCF (which was designed to support new bond and loan issuance but was not used) had been closed to new purchases at end-2020.

- The latest Fed balance sheet report shows $26.0B in holdings, but note that this includes ~$13.7bln in actual assets (~$5.2B of corporate bonds and~$8.5B of ETFs as of a mid-May filing). The remaining $12.4bln in the balance sheet is accounted for by the equity provided by the US Treasury (a large chunk of which was paid back at end-2020, see chart below).

- The relatively small footprint of the facilities in the market, and the pledge to sell off the portfolio in "gradual and orderly" fashion beginning Jun 7 (NY Fed providing details this morning here: https://www.newyorkfed.org/newsevents/news/markets...), suggest little market impact. The entire portfolio should be off the balance sheet by end-year.

- Likewise, the withdrawal of reserves from the system represented by the $14B or so securities sold to the private sector is unlikely to make much difference to overnight funding rate pressures.

- "There were many calls from outside the Fed for us to activate the CCyB in the years before the COVID event," said Quarles. "It is clear now that those calls were mistaken." The Fed official said "by any measure" the bank regulatory system did "quite well" in the face of Covid, while still singling out runs on prime money funds and commercial paper as "particularly concerning," and adding that policymakers will also focus attention on non-banks. For more see MNI Policy main wire at 1508ET.

US TSY SUMMARY:

Rates and equities traded weaker while USD enjoyed strong gains (DXY topped 90.55) in the aftermath of stronger than expected ADP private employ data (+978K vs. +650 exp) Thu. Quiet sideways trade for rates and equities since before noon -- relative quiet ahead Fri's headline May employ data: mean estimate has been gaining: NFP +674k vs. +266k last month.- Signal For Nonfarms Remains Unclear: -88K revision to April's figure did little to take the sheen off a strong beat in May's ADP payrolls reading (+978k jobs vs +650k survey, and above the highest estimate of +900k).

- That said, the large discrepancy between ADP and the BLS nonfarms figure for April last month should be kept in mind, for another potential overestimation by the ADP's model for May. But perhaps we'll see some modest adjustments higher in the surveys for tomorrow's NFP (currently +655k, with BBG whisper.

- Eurodollar option trade consistently bearish on the day, hedging rate hikes via puts in 2- and 3Y midcurves.

- The 2-Yr yield is up 1.4bps at 0.1585%, 5-Yr is up 4.8bps at 0.8413%, 10-Yr is up 3.6bps at 1.6233%, and 30-Yr is up 2.3bps at 2.2946%.

OVERNIGHT DATA

ADP NATL EMPLOYMENT +978K MAY (+650 EXP., +654K REV. PRIOR); APR REVISED -88K TO 742K

U.S. Challenger Job-Cut Announcements Fell 93.8% Y/y in May "Employers announced 49,118 hiring plans in May, the lowest monthly total since last May, when 38,981 hiring plans were announced," report notes.

- US JOBLESS CLAIMS -20K TO 385K IN MAY 29 WK

- US PREV JOBLESS CLAIMS REVISED TO 405K IN MAY 22 WK

- US CONTINUING CLAIMS +0.169M to 3.771M IN MAY 22 WK

- US Q1 REV NONFARM PRODUCTIVITY +5.4%; Y/Y +4.1%

- US Q1 REV NONFARM PRODUCTIVITY +5.4%; Y/Y +4.1%

- US Q1 UNIT LABOR COSTS +1.7%; Y/Y +4.1%

- US DATA: ISM Services PMI Hits Record High In May

- US ISM SERVICES PMI 64.0 MAY VS 62.7 APR

- US ISM SERVICES BUSINESS INDEX 66.2 MAY VS 62.7 APR

- US ISM SERVICES EMPLOYMENT INDEX 55.3 MAY VS 58.8 APR

- US ISM SERVICES NEW ORDERS 63.9 MAY VS 63.2 APR

- US ISM SERVICES SUPPLIER DELIVERIES 70.4 MAY VS 66.1 APR (NSA)

- U.S. WEEKLY LANGER CONSUMER COMFORT INDEX AT 55.6 VS 53.8

MARKETS SNAPSHOT

Key late session market levels

- DJIA down 8.29 points (-0.02%) at 34593.17

- S&P E-Mini Future down 13.5 points (-0.32%) at 4193

- Nasdaq down 124.9 points (-0.9%) at 13631.9

- US 10-Yr yield is up 3.6 bps at 1.6233%

- US Sep 10Y are down 11.5/32 at 131-18.5

- EURUSD down 0.0085 (-0.7%) at 1.2126

- USDJPY up 0.73 (0.67%) at 110.29

- WTI Crude Oil (front-month) down $0.11 (-0.16%) at $68.72

- Gold is down $36.27 (-1.9%) at $1872.04

European bourses closing levels:

- EuroStoxx 50 down 9.26 points (-0.23%) at 4079.24

- FTSE 100 down 43.65 points (-0.61%) at 7064.35

- German DAX up 29.96 points (0.19%) at 15632.67

- French CAC 40 down 13.6 points (-0.21%) at 657.92

US TSY FUTURES CLOSE:

- 3M10Y +3.407, 160.127 (L: 155.619 / H: 160.81)

- 2Y10Y +2.026, 146.113 (L: 143.72 / H: 147.19)

- 2Y30Y +0.833, 213.344 (L: 211.942 / H: 214.957)

- 5Y30Y -2.513, 145.181 (L: 144.912 / H: 148.425)

- Current futures levels:

- Sep 2Y down 0.875/32 at 110-10.5 (L: 110-10.375 / H: 110-11.5)

- Sep 5Y down 7.5/32 at 123-19.75 (L: 123-19.5 / H: 123-28)

- Sep 10Y down 10.5/32 at 131-19.5 (L: 131-18 / H: 131-31.5)

- Sep 30Y down 13/32 at 156-3 (L: 155-27 / H: 156-23)

- Sep Ultra 30Y down 15/32 at 184-20 (L: 184-05 / H: 185-17)

US EURODOLLAR FUTURES CLOSE

- Jun 21 +0.002 at 99.877

- Sep 21 steady at 99.880

- Dec 21 steady at 99.825

- Mar 22 -0.010 at 99.830

- Red Pack (Jun 22-Mar 23) -0.02 to -0.005

- Green Pack (Jun 23-Mar 24) -0.03 to -0.05

- Blue Pack (Jun 24-Mar 25) -0.05

- Gold Pack (Jun 25-Mar 26) -0.05 to -0.055

Short Term Rates

US DOLLAR LIBOR: Latest Settles

- O/N -0.00037 at 0.05463% (-0.00650/wk)

- 1 Month -0.00550 to 0.08000% (-0.00588/wk)

- 3 Month -0.00325 to 0.13075% (-0.00062/wk) ** (Record Low 0.12850% on 06/01/21)

- 6 Month -0.00263 to 0.16475% (-0.00625/wk)

- 1 Year +0.00075 to 0.24563% (-0.00250/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $70B

- Daily Overnight Bank Funding Rate: 0.05% volume: $250B

- Secured Overnight Financing Rate (SOFR): 0.01%, $953B

- Broad General Collateral Rate (BGCR): 0.01%, $408B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $371B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $2.001B accepted vs. $5.650B submission

- Next scheduled purchase:

- Fri 6/04 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

PIPELINE: $5.3B High-Grade Corporate Issuance

- Date $MM Issuer (Priced *, Launch #)

- 06/03 $1.5B *Consolidated Edison $750M each: 10Y +80, 40Y +130

- 06/03 $850M Ares Capital 7Y +165

- 06/03 $750M #Travelers 30Y +75

- 06/03 $700M *Blue Owl Fnc 10Y +165

- 06/03 $500M *Puget Energy 7Y +108

- 06/03 $500M *IADB 10Y FRN SOFR+36

- 06/03 $500M *Council of Europe Development Bank (CoE) 3Y -4

- $18.4B Priced Wednesday

- 06/02 $5.5B *ADB $4B 3Y -3, $1.5B 7Y +10

- 06/02 $3.15B #Citigroup $2.75B 6NC5 +67, $400M 6NC5 FRN SOFR+77

- 06/02 $3B #Indonesia $1.25B 5Y 1.5%, $1B 10Y +2.55%, $ 750M 30Y 3.55% Sukuk

- 06/02 $2.5B #Societe Generale $1.25B each: 6NC5 +100, 11NC10 +130

- 06/02 $2B #Truist Fncl $1B each: 4NC3 FRN SOFR+40, 8NC7 +63

- 06/02 $1.5B #Petrobras 30Y 5.75%

- 06/02 $750M NY Life Ins $400M 5Y +37, $350M 5Y FRN SOFR+48

EGBs-GILTS CASH CLOSE: Service Sector Recovery Helps Set Bearish Tone

EGBs and Gilts weakened Thursday amid strong European and US service sector data, and ahead of US nonfarm payrolls Friday.

- We saw fairly strong bear steepening in the Gilt curve, not helped by yet another weak BOE APF operation; 10-Yr BTP yields rose for the first session in five, though spreads remain relatively contained due to Bund weakness.

- Italy and Spain Services PMIs beat expectations to the upside, while the Eurozone and moreso the UK saw upward revisions in final readings vs flash.

- With no key European data (with the possible exception of Eurozone Apr retail sales), speakers or supply Friday, attention is almost entirely on the US employment report.

Closing German/UK Yields And 10-Yr Spreads To Germany

- Germany: The 2-Yr yield is down 0.5bps at -0.668%, 5-Yr is unchanged at -0.579%, 10-Yr is up 1.5bps at -0.183%, and 30-Yr is up 1.6bps at 0.379%.

- UK: The 2-Yr yield is up 2.7bps at 0.087%, 5-Yr is up 3.4bps at 0.371%, 10-Yr is up 4.2bps at 0.841%, and 30-Yr is up 4.3bps at 1.371%.

- Italian BTP spread up 0.5bps at 108.1bps / Spanish spread up 0.1bps at 65.3bps

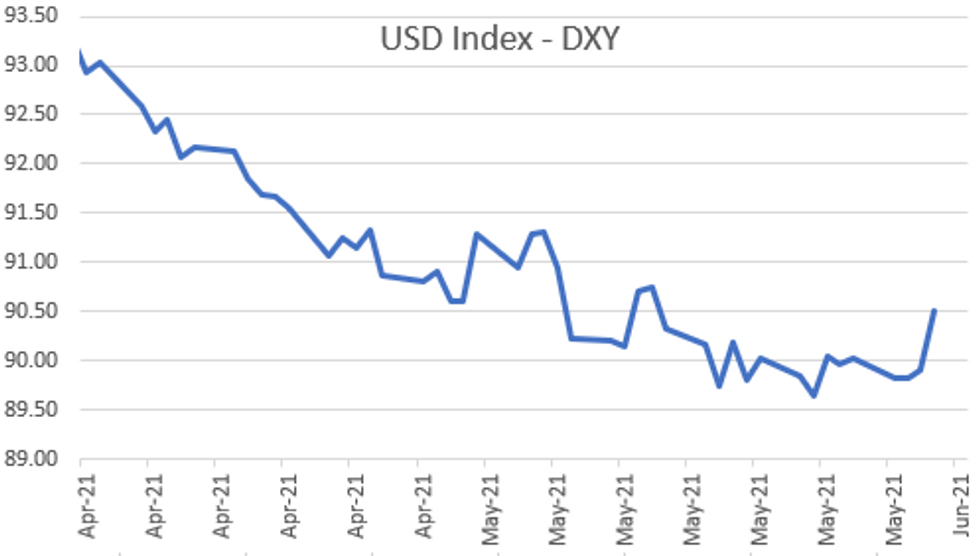

FOREX: Strong Dollar Squeeze As Markets Await Friday's NFP Report

- The Dollar Index Reached its best levels since May 14th as the greenback consistently extended gains throughout the US session, following a firm ADP Employment Reading.

- Risk tied currencies were the hardest hit as equity markets started the US session poorly. Despite a late bounce on the Biden tax headlines, the more realistic prospect of legislation passing in the US continued to buoy the dollar.

- AUD and NZD lost around 1.5% compared to the 0.7% gains in broad dollar indices. Further relative underperformers were seen in the EM space with MXN, TRY and ZAR all retreating over 1%.

- Most other G10 currencies fell a proportional amount, with EUR, JPY, GBP, CAD and CHF all lower by between 0.5-0.7%.

- Recent fresh multi month/year highs made in both GBP and CAD represent interesting potential technical turning points. GBPUSD lies right at initial firm support of 1.4092, May 27 low where a break would suggest scope for a deeper corrective pullback.

- The focus for markets turns to Friday's release of US May Non-Farm Payrolls. Fed's Daly tweeted a reminder that the data for the 'next few months will likely be volatile…We have work to do to get to full employment and price stability.'

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.