Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI BRIEF: U.S. Jobless Claims Rise For 1st Time Since April

- MNI INTERVIEW: Big-Spending Trudeau Seen Calling Snap Election

- FED Reverse Repo: New Record High: USAGE SURGES TO RECORD $756B AFTER RATE TWEAK, Bbg

- ECB's WEIDMANN: PEPP MUST END WHEN PANDEMIC IS OVER: HANDELSBLATT

- WEIDMANN: GERMAN INFLATION SPIKE TEMPORARY: HANDELSBLATT, Bbg

US TSY SUMMARY: Curves Crater

Post-FOMC: Reflation unwinds, slow to get underway but inexorable bull curve flattening into the second half. Little post-claims chop as Bonds started climb higher after weekly claims climb (+37k to 412K vs. +360k exp), continuing claims +3.518M vs. +3.425M exp.- Thu's bull flattening largely result of Wed's FOMC, upping DOTS to pencil in two rate hikes by late 2023. Some technical buying while shorts caught wrong-footed, forced to unwind, exacerbating the move. Long end Tsy Bonds clawed higher, 30YY fell to 2.0468% low (mid-Feb level), 10YY around 1.5% after slipping to 1.4702% low -- stable by comparison.

- Aside from tight stops getting triggered on the rally in long end, curve steepener unwinds contributed: TD Securities reports they are taking off a 5s30s steepener as well as 9Y TIPS BE position. TD explained "reflation trades suffered a significant setback after the Fed delivered a hawkish message at the June FOMC — raising the 2023 dots, upgrading the SEP, and sending a message that tapering discussions had begun. This more hawkish message has led to a significant paring of reflation trades, with short covering exacerbating the moves.

- TD added the "initial curve steepening was driven by a selloff in the 5y sector as the market pulled forward tapering and hike expectations. However, the flattening has been replaced by short-covering buying, exacerbating the move."

- The 2-Yr yield is up 0.6bps at 0.2113%, 5-Yr is down 2.1bps at 0.8744%, 10-Yr is down 6.6bps at 1.5091%, and 30-Yr is down 10.9bps at 2.0982%.

US

DATA: U.S. weekly jobless claims rose by 37,000 to 412,000 in the latest week, the first increase since April and a break from what has been a gradual but steady improvement.

- The Federal Reserve on Wednesday indicated it needs to see further gains in employment before tapering QE. Economists say claims numbers are getting harder to read as the expiration of extended pandemic benefits in some states is now muddying the data.

US: No unexpected close Friday: Market chatter over Juneteenth becoming a Federal holiday -- though would fall on Saturday -- chatter that banks may have to scramble if the Federal Reserve follows suit. Bubble burst: According to the Fed:

- "In anticipation of President Biden signing into law the Juneteenth National Independence Day Act, we are notifying our customers that Federal Reserve Financial Services will remain open on Friday, June 18, 2021, and Monday, June 21, 2021. This conforms to our standard practice for any federal holiday that falls on a Saturday".

- "In the event the bill is signed into law, the Federal Reserve will determine how to adjust our schedule to reflect the new federal holiday in the years to come".

CANADA

CANADA: Canada's Liberal Prime Minister Justin Trudeau may use a debate over a post-Covid reconstruction package to force an early election in the fall in a bid to secure a parliamentary majority for a big-spending third term in office, a top adviser to former Conservative Prime Minister Stephen Harper, told MNI.

- While major new policies have re-energized Trudeau, the opposition Conservatives have struggled to present a clear message, said Sean Speer, a senior economic adviser to Harper during his 2006-2015 government. Trudeau, who became prime minister in 2015 before winning again in 2019, may pounce, saying he needs a fresh mandate for a post Covid rebuild, Speer said. For more see MNI Policy main wire at 1135ET.

OVERNIGHT DATA

- US JOBLESS CLAIMS +37K TO 412K IN JUN 12 WK

- US PREV JOBLESS CLAIMS REVISED TO 375K IN JUN 05 WK

- US CONTINUING CLAIMS +0.001M to 3.518M IN JUN 05 WK

- US Conference Board: May Leading Index 114.5

- US Conference Board May Leading Index +1.3%

- US Conference Board: May Lagging Index -2.2%

- US Conference Board: May Coincident Index +0.4%

- US JUN PHILADELPHIA FED MFG INDEX 30.7

- U.S. WEEKLY LANGER CONSUMER COMFORT INDEX AT 56.2 VS 55.4

- FOREIGN HOLDINGS OF CANADA SECURITIES +10.0B CAD IN APR

- CANADIAN HOLDINGS OF FOREIGN SECURITIES +18.6B CAD IN APR

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 246.38 points (-0.72%) at 33789.71

- S&P E-Mini Future down 3.25 points (-0.08%) at 4210.5

- Nasdaq up 124.1 points (0.9%) at 14164.99

- US 10-Yr yield is down 6.6 bps at 1.5091%

- US Sep 10Y are up 8.5/32 at 132-0.5

- EURUSD down 0.0077 (-0.64%) at 1.1918

- USDJPY down 0.48 (-0.43%) at 110.23

- WTI Crude Oil (front-month) down $1.09 (-1.51%) at $71.06

- Gold is down $32.76 (-1.81%) at $1778.75

European bourses closing levels:

- EuroStoxx 50 up 6.38 points (0.15%) at 4158.14

- FTSE 100 down 31.52 points (-0.44%) at 7153.43

- German DAX up 17.1 points (0.11%) at 15727.67

- French CAC 40 up 13.61 points (0.2%) at 6666.26

US TSY FUTURES CLOSE

- 3M10Y -6.375, 147.615 (L: 143.472 / H: 154.505)

- 2Y10Y -6.736, 129.682 (L: 125.888 / H: 137.552)

- 2Y30Y -10.436, 189.174 (L: 183.617 / H: 200.191)

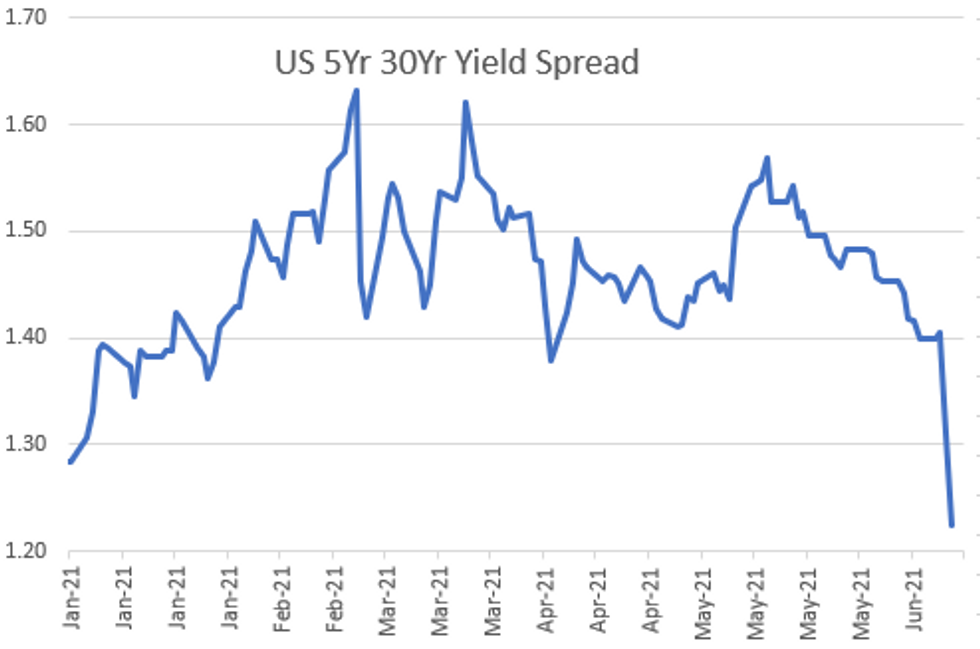

- 5Y30Y -8.762, 122.265 (L: 116.755 / H: 131.712)

- Current futures levels:

- Sep 2Y down 0.875/32 at 110-6.375 (L: 110-06.375 / H: 110-07.625)

- Sep 5Y down 2.25/32 at 123-10.75 (L: 123-07.25 / H: 123-14)

- Sep 10Y up 6.5/32 at 131-30.5 (L: 131-14 / H: 132-05)

- Sep 30Y up 1-25/32 at 159-19 (L: 157-16 / H: 160-24)

- Sep Ultra 30Y up 3-17/32 at 191-12 (L: 187-15 / H: 193-17)

US EURODOLLAR FUTURES CLOSE

- Sep 21 +0.010 at 99.865

- Dec 21 +0.010 at 99.810

- Mar 22 +0.005 at 99.820

- Jun 22 steady at 99.760

- Red Pack (Jun 22-Mar 23) -0.055 to steady

- Green Pack (Jun 23-Mar 24) -0.065 to -0.04

- Blue Pack (Jun 24-Mar 25) -0.02 to +0.040

- Gold Pack (Jun 25-Mar 26) +0.060 to +0.105

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00775 at 0.06325% (+0.00788/wk)

- 1 Month +0.01088 to 0.09338% (+0.02050/wk)

- 3 Month +0.01000 to 0.13450% (+0.01562/wk) ** (New Record Low: 0.11800% on 6/14)

- 6 Month +0.00675 to 0.15863% (+0.00612/wk)

- 1 Year +0.01063 to 0.24513% (+0.00575/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $62B

- Daily Overnight Bank Funding Rate: 0.04% volume: $242B

- Secured Overnight Financing Rate (SOFR): 0.01%, $900B

- Broad General Collateral Rate (BGCR): 0.01%, $375B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $352B

- (rate, volume levels reflect prior session)

- Tsys 22.5Y-30Y, $2.001B accepted vs. $4.419B submission

- Next scheduled purchase:

- Fri 6/18 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

PIPELINE: $1B Kenya 2034-Bond Launched

- Date $MM Issuer (Priced *, Launch #)

- 06/17 $1B #Kenya 2034 Bond 6.3%

- 06/17 $800M GXO Logistics 5Y +85a, 10Y +120a

- 06/17 $750M #Eagle Materials 10Y +110

- 06/17 $600M #Sun Communities 10Y +125

FOREX: Greenback and JPY Firmer As Risk Sentiment Wanes

- The dollar index edged consistently higher throughout Thursday's session, extending the post-fed renewed optimism for the greenback. The advance was aided by a sharp move lower in precious and industrial metals as well as oil finally ending it's winning streak.

- Gains were broad based as EUR, GBP, AUD, NZD, CAD and CHF all retreated between 0.6-1%.

- EURUSD continued to fall sharply, taking out multiple short term supports to fall 2% from yesterday's highs, finally pausing for breath at a noted support of 1.1893, 2.0% 10-dma envelope.

- The standout performer against the dollar was the resilient Japanese Yen as the reversal in US yields and the initial drop in equity indices soured risk sentiment. Additionally, strong resistance headed into the March high of 110.97 also slowed down proceedings following the overnight rally.

- JPY strength and softer risk led to some sizeable declines in cross-JPY. AUDJPY, CADJPY and EURJPY the notable movers, all shedding over 1% for Thursday as of writing and unable to bounce despite a late recovery in US indices

- These moves come ahead of the Bank of Japan due overnight. The June meeting should ultimately prove to be a very bland affair, with no changes in monetary policy expected. There are also no expectations for tweaks to the Bank's overarching economic view and forward guidance, as it continues to fight the well-documented disinflationary forces in play in Japan. UK Retail Sales rounds off the week's data calendar.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok