Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI INTERVIEW: EU Trade Committee VP Seeks New Dawn With China

- MNI: Jackson Hole Too Soon For QE Taper Nod, Ex-Officials Say

- MNI BRIEF: Fed's Bowman - More Needed to Get on Strong Footing

US

FED: This month's Jackson Hole conference comes too early for Federal Reserve Chair Jerome Powell to announce or hint at the timing and pace of a reduction in the pace of central bank bond purchases, former officials told MNI.

- Some investors read Powell's optimism on the economy during his last press conference as a hawkish signal. However, ex-policymakers highlighted the chair's emphasis on the need for additional job gains as a sign that a tapering announcement is not imminent.

- "With regards to tapering I think what he was saying is you're not going to hear anything soon," said Dennis Lockhart, former Atlanta Fed President, in an interview. "You're certainly not going to hear anything at Jackson Hole. And they're going to deliberate for another couple of meetings in all likelihood." For more see MNI Policy main wire at 1300ET.

- "Despite the encouraging pace of recent hiring, employment is still far below where it was," Bowman said in opening remarks at the Fed's first event in a new series called "Toward an Inclusive Recovery." "I am hopeful that we will continue to build on this recent positive momentum, since there is more work to be done to get the economy back on strong footing, as it was before the public health emergency."

EUROPE

EU: The EU's review of relations with China this autumn should aim for a new dialogue and even a "gradual rapprochement" between the two trading powers to unfreeze an investment deal, European Parliament International Trade Committee Vice President and MEP Iuliu Winkler told MNI.

- EU leaders are due to discuss the erosion in bilateral relations in an informal meeting under the Slovenian presidency in October – after the EU-China Comprehensive Investment Agreement (CAI) was put on the shelf by Brussels following EU sanctions imposed on China in May and subsequent tit for tat action by Beijing.

- Winkler, a Romanian member of the European People's Party, says he doesn't expect the EU to change its 2019 China Strategy description of the country as a "partner, economic competitor and systemic rival", but adds that the aim should be to at least start a fresh dialogue.

OVERNIGHT DATA

- US REDBOOK: JUL STORE SALES +15.5% V YR AGO MO

- US REDBOOK: STORE SALES +17.2% WK ENDED JUL 31 V YR AGO WK

- US REDBOOK: WILL RESUME MONTH-TO-MONTH DATA COMPARISON IN FEB 2022

- US JUN FACTORY ORDERS +1.5%; EX-TRANSPORT NEW ORDERS +1.4%

- US JUN DURABLE ORDERS +0.9%

- US JUN NONDEFENSE CAP GOODS ORDERS EX AIRCRAFT +0.7%

- Durable goods orders revised up to +0.9% in the final reading (vs 0.8% prior). Core capital goods orders revised up too, to +0.7% (vs +0.5% prior). * The initial June release had been a little tricky to read, coming in well below expectations, but with higher revisions to prior months. At this stage though it looks like core cap goods orders (ex-aircraft, ex-defense, which correlate well with future months' business investment) has performed more strongly than expected over the past couple of months.

- That said, we're well off the 1+% M/M growth figures in core seen in March and April.

- Treasuries a few ticks off session highs following the release, but nothing remarkable. The bigger data tests await later in the week (namely nonfarm payrolls Friday).

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 223.47 points (0.64%) at 35067.86

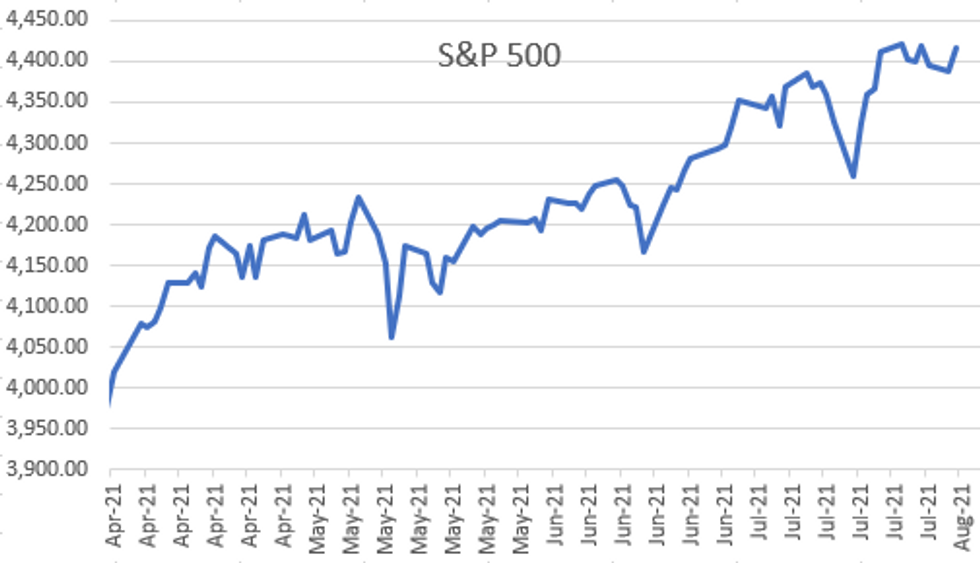

- S&P E-Mini Future up 28.25 points (0.65%) at 4409

- Nasdaq up 49.3 points (0.3%) at 14729.97

- US 10-Yr yield is down 0 bps at 1.1772%

- US Sep 10Y are down 1.5/32 at 134-30.5

- EURUSD down 0.0006 (-0.05%) at 1.1864

- USDJPY down 0.16 (-0.15%) at 109.15

- WTI Crude Oil (front-month) down $0.76 (-1.07%) at $70.53

- Gold is down $3.08 (-0.17%) at $1810.71

- EuroStoxx 50 up 1.33 points (0.03%) at 4117.95

- FTSE 100 up 24 points (0.34%) at 7105.72

- German DAX down 13.65 points (-0.09%) at 15555.08

- French CAC 40 up 47.91 points (0.72%) at 6723.81

US TSY SUMMARY: Modest Risk-On

Tsys traded marginally mixed into Tuesday's close, off midmorning highs as risk appetite improved with equities posting decent late gains (ESU1 +29.0), US$ gains.

- Rather modest volumes (TYU1 <925k) after solid beat on June factory orders (+1.5% vs +1.0% expected); ex-transport +1.4%, and with strong upward revisions to May.

- Otherwise rather subdued trade ahead Wednesday's ADP Private employ data (690k est vs. 692k prior) and Friday's headline July employment data (+875k est vs. +850k fin June).

- The 2-Yr yield is unchanged at 0.1722%, 5-Yr is down 0.2bps at 0.6521%, 10-Yr is down 0bps at 1.1772%, and 30-Yr is down 0bps at 1.8497%.

US TSY FUTURES CLOSE

- 3M10Y -0.763, 112.149 (L: 110.327 / H: 114.805)

- 2Y10Y -0.516, 99.799 (L: 98.371 / H: 101.668)

- 2Y30Y -0.457, 167.106 (L: 165.521 / H: 168.948)

- 5Y30Y +0.027, 119.476 (L: 118.234 / H: 120.339)

- Current futures levels:

- Sep 2Y up 0.125/32 at 110-11.5 (L: 110-10.87 / H: 110-12)

- Sep 5Y up 0.5/32 at 124-22.75 (L: 124-19.25 / H: 124-26)

- Sep 10Y up 0.5/32 at 135-0.5 (L: 134-25 / H: 135-06)

- Sep 30Y up 3/32 at 166-3 (L: 165-17 / H: 166-14)

- Sep Ultra 30Y up 4/32 at 201-14 (L: 200-18 / H: 202-06)

US EURODOLLAR FUTURES CLOSE

- Sep 21 +0.005 at 99.880

- Dec 21 +0.010 at 99.835

- Mar 22 +0.010 at 99.860

- Jun 22 +0.010 at 99.825

- Red Pack (Sep 22-Jun 23) +0.005 to +0.010

- Green Pack (Sep 23-Jun 24) +0.010 to +0.015

- Blue Pack (Sep 24-Jun 25) +0.010 to +0.015

- Gold Pack (Sep 25-Jun 26) +0.005

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00188 at 0.08138% (+0.00450/wk)

- 1 Month +0.00075 to 0.09038% (-0.00013/wk)

- 3 Month -0.00237 to 0.12138% (+0.00362/wk) ** (Record Low: 0.11800% on 6/14)

- 6 Month -0.00150 to 0.15513% (+0.00200/wk)

- 1 Year -0.00025 to 0.23213% (-0.00300/wk)

- Daily Effective Fed Funds Rate: 0.10% volume: $74B

- Daily Overnight Bank Funding Rate: 0.08% volume: $246B

- Secured Overnight Financing Rate (SOFR): 0.05%, $986B

- Broad General Collateral Rate (BGCR): 0.05%, $398B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $360B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $3.506B submission

- Next scheduled purchases

- Wed 8/04 1100-1120ET: Tsy 7Y-10Y, appr $3.225B

- Thu 8/05 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 8/06 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

FED: Reverse Repo Operations -- Record High, Over $1T

NY Fed reverse repo usage recedes to $909.442B from 72 counterparties vs. $921.317B on Monday. Compares to last Friday's new record high of $1.039.394B

PIPELINE: Starting to Launch

Still waiting for JP Morgan, National Bank of Canada- Date $MM Issuer (Priced *, Launch #)

- 08/03 $2B #UBS 3Y +60a, 3Y FRN/SOFR+60a, 6NC5 +105a

- 08/03 $1.5B #Rockwell Automation $600M 2NC1 +20, $450M 10Y +60, $450M 40Y +95

- 08/03 $1.3B #Ashtead Capital $550M 5Y +90, $750M 10Y +130

- 08/03 $650M #Invitation Homes 10Y +100

- 08/03 $Benchmark National Bank of Canada 3Y +45, 3Y FRN/SOFR

- 08/03 $Benchmark JP Morgan 4NC3 fix to FRM +65a

- 08/03 $Benchmark Bank of China 2Y FRN

EGBs-GILTS CASH CLOSE: Short End Notably Weaker

German and UK yields finished a little off session lows after what appeared to be late-afternoon (1500BST onward) profit-taking into the close Tuesday as equities bounced.

- Curves flattened, with short-end weakening (Gilts notably so ahead of BoE decision Thursday). 10Y Bund yields touched a fresh 6-month low at -0.492%; Gilts went as low as 0.50% (near the Jul low). Periphery EGB spreads edged lower.

- Today, Austria sold E1.3bln of 4-/10-Yr RAGBs, and the UK sold E2.0bln of Jul-51 Gilt. Wednesday sees Germany sell E4bln of Bobl.

- Little in data / speakers; Weds sees final Services PMIs, with first/only readings for Spain and Italy.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.4bps at -0.771%, 5-Yr is up 0.7bps at -0.748%, 10-Yr is up 0.5bps at -0.482%, and 30-Yr is unchanged at -0.011%.

- UK: The 2-Yr yield is up 2.3bps at 0.057%, 5-Yr is up 0.5bps at 0.23%, 10-Yr is down 0.1bps at 0.52%, and 30-Yr is down 1.2bps at 0.946%.

- Italian BTP spread down 1bps at 104.8bps / Spanish down 0.5bps at 71.5bps

FOREX: Antipodean FX Hold onto Gains

- Despite the greenback recovering losses throughout US hours, AUD (+0.40%) and NZD (0.53%) have held onto the majority of overnight gains. These strong performances were inspired by marginally hawkish central bank rhetoric.

- The RBNZ released a statement outlining their intention to step up efforts to reign the roaring housing market by tightening mortgage lending standards. The RBA then defied market consensus and chose to stick with its tapering plan, despite the ongoing resurgence of Covid-19 in Australia.

- NOK had been the strongest currency in G10 heading into the start of US trade. However, a sharp move lower in crude futures prompted a reversal from these elevated levels, with both EURNOK and USDNOK reverting to unchanged on the week.

- Echoing this move in oil, USDCAD found fresh impetus, extending on gains above the 1.25 handle to reach 1.2552 as of writing. On the topside, initial resistance is at 1.2607, Jul 23 high. A break of this level would signal the resumption of bullish activity.

- Elsewhere, activity was limited in the currency space. USDJPY briefly traded below 109 to fresh lows of 108.88 before bouncing back above the figure, where volatility subsided. Attention is on 108.47, a Fibonacci retracement as a technically bearish focus continues to dominate the outlook.

- Kiwi Unemployment will kick off Wednesday's APAC session, shortly followed by Aussie Retail Sales. The US docket will include ADP employment change followed by ISM Services PMI.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.