Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Fed's Daly Says Against Preemptive Rate Hikes

- MNI: BOC Sees Major Labor Slack And Calls Inflation Transitory

- Tsy Sec Yellen Update Debt Limit Guidance in Near Term

- FED BULLARD: I HAVE TWO 2022 RATE HIKES MARKED, DEPENDING ON DATA, Bbg

- U.S. TO DIPLOMATICALLY BOYCOTT BEIJING OLYMPICS: WAPO COLUMNIST, Bbg

US

FED: The Federal Reserve should gain more clarity about the inflation outlook before raising interest rates rather than acting preemptively on fears around lasting price pressures, San Francisco Fed President Mary Daly said Tuesday.

- "I come down on the side of waiting to gain greater clarity," Daly said in prepared remarks for the Commonwealth Club of California. "The Fed is well positioned to act should inflation begin to look more persistent. It's much harder to unwind a preemptive action that turns out to be wrong."

- Fed officials are coming under increasing pressure to raise official borrowing costs as inflation has proven less transitory -- and substantially higher -- than policymakers had anticipated. U.S. consumer prices surged 6.2% in the year to October. For more see MNI Policy main wire at 1530ET.

US: Tsy Sec Janet Yellen speaking on NPR's 1A re: making an annc on debt limit guidance in the near term. No transcript or alert from Tsy as yet, below from Bbg:

- REITERATES U.S. DOWNGRADE RISK IF NO DEBT-LIMIT HIKE

- 'CAN'T IMAGINE' CONGRESS WOULD LET DEFAULT HAPPEN

- NEW GUIDANCE COMING ON TIMING FOR DEBT LIMIT

- `NOT GREAT DEAL OF TIME' LEFT FOR DEBT PAST DEC. 3

- REITERATES DEBT LIMIT PROCESS IS `SELF INFLICTED WOUND'

FED: BULLARD: PROMISING U.S. COULD MOVE TO HIGHER PRODUCTIVITY GROWTH, Bbg

- BULLARD: I WOULDN'T MESS AROUND WITH THE INFLATION TARGET, Bbg

- BULLARD: I HAVE TWO 2022 RATE HIKES MARKED, DEPENDING ON DATA, Bbg

- BULLARD: COULD ALLOW BALANCE-SHEET RUNOFF AT END OF TAPER, Bbg

CANADA

BOC: Bank of Canada Deputy Governor Larry Schembri said Tuesday there is still a lot of job market slack and called recent elevated price gains transitory, saying the pandemic makes it tougher for policy makers to figure out relationships between the economy's full potential and inflation.

- "The labour market has recovered the pandemic-induced job losses, but considerable excess capacity remains," Schembri said. "We still see areas of slack, notably the high share of long-term unemployed and the elevated unemployment rates of older workers. Wage growth also continues to lag." For more see MNI Policy main wire at 1200ET.

US TSYS: Retail Sales Beat Estimates, Tsy Yields Climb Higher

Tsys extend session lows late after early see-saw trade. Post-Data Pressure:

Rates reversed early gains/extended lows after better than ests' Retail Sales gained +1.7% (+1.4% est), control group +1.6% M/M (+0.9%).- Major contributors to sales gains: electronics & appliances and building materials & garden, marrying up nicely with the stronger Home Depot /WMT earnings earlier today.

- After some initial two way, yield curves added to Monday's steepening as early long end support evaporated by late morning.

- Large Eurodollar Block: -30,000 EDZ2 99.070 (+0.010), sold through 99.075 post time bid at 111407ET, 99.055 last, sporadic offer picked-up as futures extended lows.

- Early heads up on the lead quarterly Dec'21 futures roll to March'22: rolling has begun with First Notice (when March'22 futures take lead) only two weeks away on November 30. That said, percentage of Dec'21 rolled remains in low single digits.

- On tap Wednesday: Building Permits (1.586M rev, 1.630M) and Housing Starts (1.555M, 1.580M). Multiple Fed Speakers and Tsy 20Y Bond Sale.

- Current 2-Yr yield is up 0.2bps at 0.5179%, 5-Yr is up 1.3bps at 1.2653%, 10-Yr is up 1.9bps at 1.6335%, and 30-Yr is up 2.5bps at 2.0207%.

OVERNIGHT DATA

- US OCT RETAIL SALES +1.7%; EX-MOTOR VEH +1.7%

- US SEP RETAIL SALES REVISED +0.8%; EX-MV +0.7%

- US OCT RET SALES EX GAS & MTR VEH & PARTS DEALERS +1.4% V SEP +0.5%

- US OCT RET SALES EX MTR VEH & PARTS DEALERS +1.7% V US OCT +0.7%

- US OCT RET SALES EX AUTO, BLDG MATL & GAS +1.3% V SEP +0.5%

- US OCT IMPORT PRICES +1.2%

- US OCT EXPORT PRICES +1.5%; NON-AG +1.5%; AGRICULTURE +1.0%

- US REDBOOK: NOV STORE SALES +15.2% V YR AGO MO

- US REDBOOK: STORE SALES +14.7% WK ENDED NOV 13 V YR AGO WK

- US REDBOOK: WILL RESUME MONTH-TO-MONTH DATA COMPARISON IN FEB 2022

- US OCT INDUSTRIAL PROD +1.6%; CAP UTIL 76.4%

- US SEP IP REV TO -1.3%; CAP UTIL REV 75.2%

- US OCT MFG OUTPUT +1.2%

- US SEP BUSINESS INVENTORIES +0.7%; SALES +0.9%

- US SEP RETAIL INVENTORIES -0.2%

MARKET SNAPSHOT

Key late session market levels:

- DJIA up 151.82 points (0.42%) at 36238.7

- S&P E-Mini Future up 25.75 points (0.55%) at 4704.75

- Nasdaq up 118.4 points (0.7%) at 15972.27

- US 10-Yr yield is up 1.9 bps at 1.6335%

- US Dec 10Y are down 4/32 at 130-5.5

- EURUSD down 0.0044 (-0.39%) at 1.1324

- USDJPY up 0.56 (0.49%) at 114.68

- WTI Crude Oil (front-month) down $0.07 (-0.09%) at $80.81

- Gold is down $11.91 (-0.64%) at $1850.93

- EuroStoxx 50 up 15.3 points (0.35%) at 4401.49

- FTSE 100 down 24.89 points (-0.34%) at 7326.97

- German DAX up 99.22 points (0.61%) at 16247.86

- French CAC 40 up 23.97 points (0.34%) at 7152.6

US TSY FUTURES CLOSE

- 3M10Y +1.808, 158.444 (L: 153.23 / H: 159.043)

- 2Y10Y +1.535, 111.016 (L: 107.315 / H: 111.533)

- 2Y30Y +2.094, 149.511 (L: 144.661 / H: 150.151)

- 5Y30Y +1.087, 75.132 (L: 71.578 / H: 75.8)

- Current futures levels:

- Dec 2Y steady at at 109-18.75 (L: 109-17.5 / H: 109-20)

- Dec 5Y down 1.5/32 at 121-11.5 (L: 121-08 / H: 121-17.25)

- Dec 10Y down 3/32 at 130-6.5 (L: 130-03.5 / H: 130-17)

- Dec 30Y down 8/32 at 160-0 (L: 159-28 / H: 160-23)

- Dec Ultra 30Y down 10/32 at 193-8 (L: 193-02 / H: 194-25)

US EURODOLLAR FUTURES CLOSE

- Dec 21 -0.0025 at 99.790

- Mar 22 steady at 99.745

- Jun 22 +0.005 at 99.555

- Sep 22 steady at 99.325

- Red Pack (Dec 22-Sep 23) -0.01 to +0.005

- Green Pack (Dec 23-Sep 24) -0.025 to -0.02

- Blue Pack (Dec 24-Sep 25) -0.035 to -0.025

- Gold Pack (Dec 25-Sep 26) -0.03 to -0.025

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00075 at 0.07425% (-0.00050/wk)

- 1 Month -0.00225 to 0.08888% (-0.00025/wk)

- 3 Month +0.00212 to 0.16000% (+0.00500/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00237 to 0.22775% (+0.00175/wk)

- 1 Year +0.00488 to 0.39913% (+0.00062/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $77B

- Daily Overnight Bank Funding Rate: 0.07% volume: $283B

- Secured Overnight Financing Rate (SOFR): 0.05%, $9568B

- Broad General Collateral Rate (BGCR): 0.05%, $349B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $333B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $4.010B submission

- Tsy 4.5Y-7Y, $5.251B accepted vs. $15.666B submission

- Next scheduled purchases

- Thu 11/18 1010-1030ET: Tsy 22.5Y-30Y, appr $1.600B

- Fri 11/19 1010-1030ET: TIPS 1Y-7.5Y, appr $1.775B

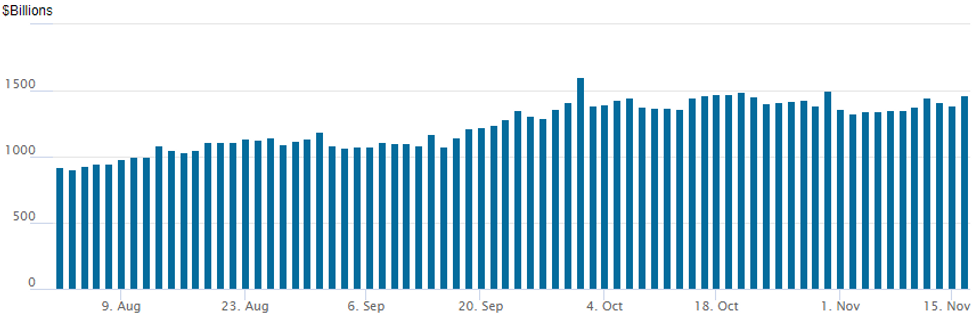

FED Reverse Repo Operation, November High

NY Federal Reserve

NY Fed reverse repo usage climbs to month high of $1,466.857B from 80 counterparties vs. $1,391.657B on Monday. Record high remains at $1,604.881B from Thursday, September 30.

PIPELINE: $7.8B Baxter Int 8Pt Jumbo Lead Tuesday Issuance

- Date $MM Issuer (Priced *, Launch #)

- 11/16 $7.8B #Baxter Int 8pt: $800M 2Y +35, $300M 2Y SOFR+26, $1.4B 3Y +45, $300M 3Y SOFR+44, $1.45B 5Y +65, $1.25B 7Y +75, $1.55B 10Y +90, $750M 30Y +110

- 11/16 $2B JBS Finance Luxembourg $1B 5Y +150a, $B +10Y +155a

- 11/16 $2B #Global Payments $500M 3Y +65, $750M 5Y +90, $750M 10Y +130

- 11/16 $1B #British Telecom $500M 60NC5.5 4.25%, $500M 60NC10 4.875%

- 11/16 $1.5B *StanChart $1B 4NC3 +95, $500M 4NC3 FRN/SOFR+93

- 11/16 $1.2B #Florida Power and Light 30Y +85

- 11/16 $1B #DBS Group $700M 3Y +30, $300M 3Y FRN/SOFR+30

- 11/16 $Benchmark Tapestry Inc 10Y +175a

- 11/16 $600M Primerica WNG 10Y +125a

- 11/16 $500M #Welltower WNG 10Y +115

- 11/16 $500M #Leggett and Platt WNG 30Y +150

- 11/16 $500M #Arrow Electronics WNG 10Y +135

- 11/16 $500M US Foods 8.5NC3.5

- Later in week:

- 11/17 $Benchmark Italy 3.875% 2051 tap/Bond reopen, +190a

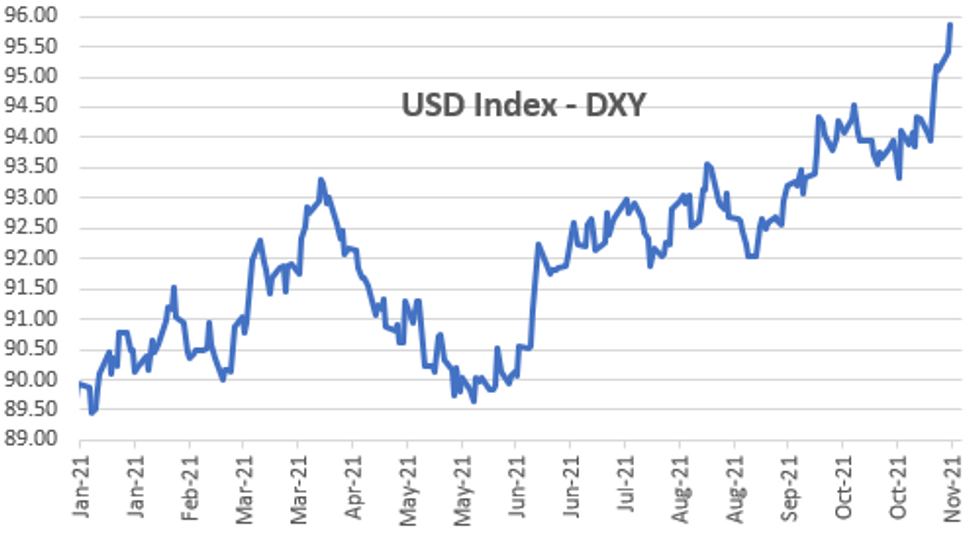

FOREX: Greenback Strength Extends Amid Strong US Data

- The US Dollar extended its strong recent form, emphasised by the dollar index printing a fresh year-to-date high for a fifth consecutive session. The index rose 0.5% during the trading session and the rally was aided by firm US retail sales and production data.

- EURUSD remains pinned to the lows and has weakened another 0.45% on Tuesday, narrowing the gap with touted support at the 1.1305 bear channel base drawn off the Jun 1st high.

- Additionally, supportive price action in USDJPY (+0.50%) has seen the pair creep up to significant horizontal resistance at 11470/73, threatening to break to the best levels since November 2017.

- The worst performers on Tuesday were NZD and AUD, losing 0.75 and 0.6% respectively.

- GBP, however, outperformed after some solid jobs data bolstered bets for a December rate hike, keeping the pound buoyant throughout European hours. This kept EURGBP firmly on the backfoot, and today's sell-off has resulted in a break of support at 0.8463, Nov 3 low. The move lower has exposed the key support at 0.8403, Oct 26 low, where a break would confirm a resumption of the broader downtrend.

- Plenty of action in emerging markets where USDTRY surged to new all-time highs at 10.4426, up well over 3% at one point. Despite a 1.3% reversal from this high print, price action continues to be very aggressive as we approach the CBRT decision on Thursday, with touted local demand exacerbating the price spike. USDZAR and USDCLP also rose over 1.5% amid the continued dollar strength.

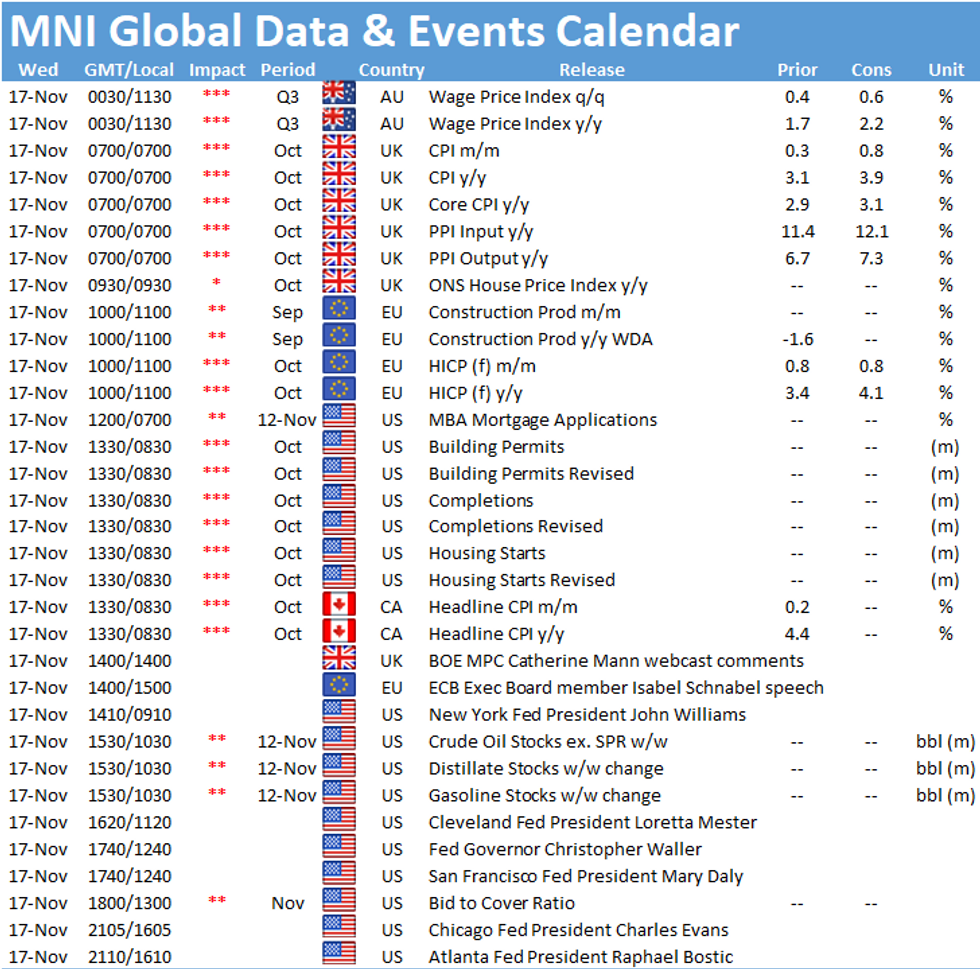

- Wednesday's data focus will be on UK and Canadian October CPI data. Markets will also be alert for crude oil inventories and another slew of Fed speakers throughout the US session.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.