Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Fed SEP To Show 5 Or More Hikes For 2022, More Inflation

- MNI: Fed's Daly Sees Some Caution After March Liftoff

- Biden To Prepare USD$1 Billion Aid To Ukraine In Event Of War

- BIDEN TO EXPAND RUSSIA SANCTIONS TO MORE ELITES, NORD STREAM 2, Bbg

US

FED: The Federal Reserve's upcoming quarterly economic forecasts are likely to show an increase in the number of rate hikes officials are penciling in for this year to at least five, up from three in December, several former central bank staffers told MNI.

- “The dots will show a median expectation of five 25-basis-point rate increases for 2022, but with some skew towards the upside,” said Peter Ireland, a former Richmond Fed staffer and now a consultant at Boston College.

- This would not be aggressive as the six rises in the federal funds priced in by rate market participants, and there are questions about the pace and sequencing policymakers will choose.

- Some of the dots could show six or seven 25-bp increases, putting the year-end funds rate at around 1.25%, though possibly as high as 1.75% or even 2%, Ireland said. For more see MNI Policy main wire at 1201ET.

- Lee: "If Putin continues to choose aggression over diplomacy, then we must also be prepared to help lead a humanitarian effort to support Ukrainians fleeing the conflict."

The Fed's improvements in communications since the stubborn inflation of the 1970s will keep price gains more stable and suggest that kind of price spiral won't return, she said in the text of a speech.

"It is time to move away from the extraordinary support that the Fed has been providing during the pandemic and bring monetary policy in line with the challenges of today," and that's likely in March, Daly said. "The timing and magnitude of future funds rate and balance sheet adjustments will depend on how the economy and the data evolve."

US TSYS: Risk Appetite Sours As Russia/Ukraine Tensions Heat Up

Tsys holding weaker across the board after the bell -- near the middle of the NY session range after some mid-morning whip-saw action. Yield curves mostly steeper, off early flatter levels w/ 5s30s just over 39.0 (+1.80). Heavy volumes driven by spike in Mar/Jun futures roll (Jun takes lead on Feb 28).- No market react to late SF Fed president Daly comments supporting liftoff in March absent "significant negative surprise" for economy, with as many as four hikes for the year.

- Session opened with a false risk-on tone despite building tensions over Russia threat to Ukraine, Tsys weaker vs. modest rally in stocks (ESH2 tapped 4345.5 high). Tsys sold off/extended session low midmorning (30YY 2.2927% high) with trading desks citing rate lock hedging vs. surge in corporate debt issuance (near $11B on day not exceptionally large however).

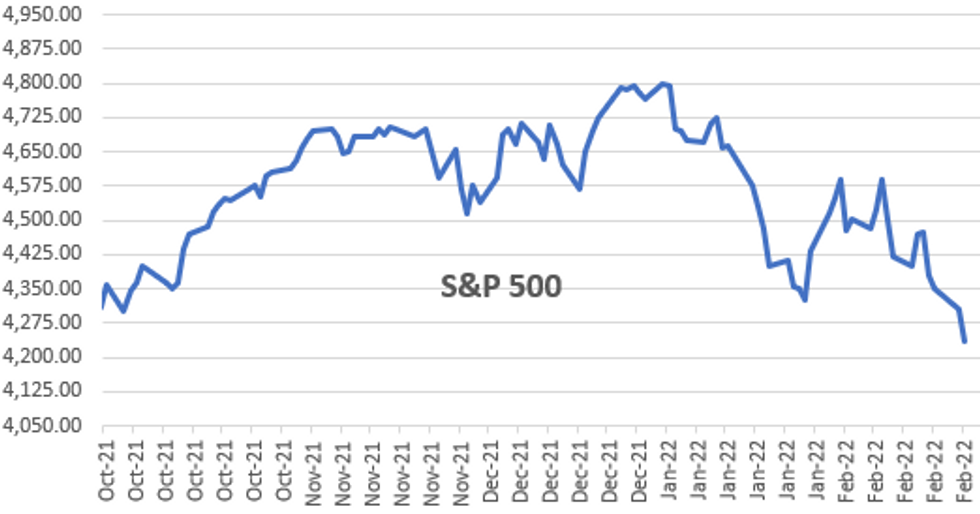

- Tsys reversed course, bouncing on headlines that Russia is within 48 hours of full-scale invasion of Ukraine. Equities sold off sharply into the close, SPX emini taps 4216.75 low.

- White House annc'd expanded sanctions on Russia elites and Nordstream 2 pipeline.

- Futures moderated through the second half holding modestly weaker after $53B 5Y note auction (91282CEC1) small stop: 1.880% high yield vs. 1.882% WI; 2.49x bid-to-cover vs. 2.50x last month.

- Limited option volumes focused on building downside (rate hike) put positions.

- The 2-Yr yield is up 4.7bps at 1.5956%, 5-Yr is up 2.4bps at 1.8864%, 10-Yr is up 3.1bps at 1.9703%, and 30-Yr is up 3bps at 2.2666%.

OVERNIGHT DATA

- US MBA: REFIS -16% SA; PURCH INDEX -10% SA THRU FEB 18 WK

- US MBA: UNADJ PURCHASE INDEX -6% VS YEAR-EARLIER LEVEL

- US MBA: 30-YR CONFORMING MORTGAGE RATE 4.06% VS 4.05% PREV

- US REDBOOK: FEB STORE SALES +14.4% V YR AGO MO

- US REDBOOK: STORE SALES +14.5% WK ENDED FEB 19 V YR AGO WK

- US REDBOOK: WILL RESUME MONTH-TO-MONTH DATA COMPARISON IN MARCH

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 424.36 points (-1.26%) at 33183.91

- S&P E-Mini Future down 70 points (-1.63%) at 4231.5

- Nasdaq down 288 points (-2.2%) at 13101.31

- US 10-Yr yield is up 3.3 bps at 1.972%

- US Mar 10Y are down 4.5/32 at 126-10.5

- EURUSD down 0.0017 (-0.15%) at 1.1308

- USDJPY down 0.13 (-0.11%) at 114.95

- Gold is up $8.59 (0.45%) at $1907.14

- EuroStoxx 50 down 12.06 points (-0.3%) at 3973.41

- FTSE 100 up 3.97 points (0.05%) at 7498.18

- German DAX down 61.64 points (-0.42%) at 14631.36

- French CAC 40 down 6.93 points (-0.1%) at 6780.67

US TSY FUTURES CLOSE

- 3M10Y +4.777, 162.398 (L: 155.078 / H: 162.572)

- 2Y10Y -0.306, 38.063 (L: 33.436 / H: 39.284)

- 2Y30Y -0.069, 68.108 (L: 63.121 / H: 68.907)

- 5Y30Y +1.45, 38.557 (L: 35.325 / H: 38.771)

- Current futures levels:

- Mar 2Y down 1/32 at 107-18.875 (L: 107-17 / H: 107-21.125)

- Mar 5Y down 4.25/32 at 117-23.5 (L: 117-20 / H: 117-29.5)

- Mar 10Y down 8/32 at 126-7 (L: 126-03 / H: 126-19.5)

- Mar 30Y down 19/32 at 152-12 (L: 152-02 / H: 153-12)

- Mar Ultra 30Y down 1-11/32 at 181-12 (L: 181-06 / H: 183-19)

(H2) Trend Needle Still Points South

- RES 4: 128-22+ High Jan 24

- RES 3: 128-01+ 50-day EMA

- RES 2: 127-24 High Feb 4

- RES 1: 127-09 High Feb 22

- PRICE: 126-09+ @ 11:42 GMT Feb 23

- SUP 1: 125-17+ Low Feb 10 and the bear trigger

- SUP 2: 125-06+ Low May 30 2019 (cont)

- SUP 3: 125-04+ 2.00 proj of the Jan 13 - 19 - 24 price swing

- SUP 4: 123-23+ 2.0% 10-dma envelope

Treasuries on Tuesday, faded off levels just above the 20-day EMA (126-12). The trend outlook remains bearish and recent gains are considered corrective. Moving average studies point south and a price sequence of lower lows and lower highs remains intact. The bear trigger is unchanged 125-17+, the Feb 10 low. On the upside, a resumption of gains would expose the 50-day EMA at 128-01+.

US EURODOLLAR FUTURES CLOSE

- Mar 22 +0.015 at 99.330

- Jun 22 +0.005 at 98.765

- Sep 22 -0.010 at 98.365

- Dec 22 -0.025 at 98.040

- Red Pack (Mar 23-Dec 23) -0.045 to -0.035

- Green Pack (Mar 24-Dec 24) -0.05

- Blue Pack (Mar 25-Dec 25) -0.05 to -0.04

- Gold Pack (Mar 26-Dec 26) -0.05 to -0.045

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00086 at 0.07743% (+0.00186/wk)

- 1 Month +0.01100 to 0.18686% (+0.01615/wk)

- 3 Month +0.00971 to 0.49757% (+0.01800/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.04486 to 0.82629% (+0.04500/wk)

- 1 Year +0.04829 to 1.33686% (+0.05100/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.08% volume: $72B

- Daily Overnight Bank Funding Rate: 0.07% volume: $257B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.05%, $930B

- Broad General Collateral Rate (BGCR): 0.05%, $345B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $332B

- (rate, volume levels reflect prior session)

NY Fed Purchase Operation: The Desk plans to purchase approximately $20 billion, ending Thu, March 9.

- Next scheduled purchases:

- Thu 02/24 1010-1030ET: Tsy 0Y-22.5Y, appr $6.225B steady

- Tue 03/01 1100-1120ET: TIPS 7.5Y-30Y, appr $0.625B vs. $1.225B prior

- Thu 03/03 1100-1120ET: Tsy 7Y-10Y, appr $1.625B vs. $3.225 prior

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

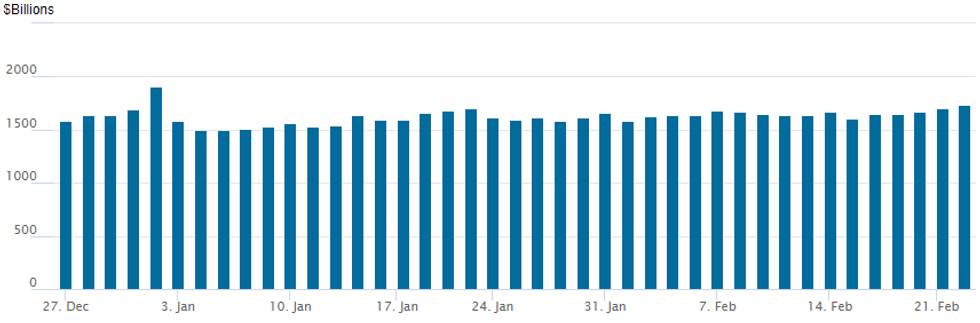

FED Reverse Repo Operation, Highest of Year

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $1,738.322B -- highest of year w/ 77 counterparties vs. $1,699.432B prior session -- remains well off all-time high of $1,904.582B on Friday, December 31.

PIPELINE: $3.5B Wells Fargo Debt Launched

Total $10.7B high-grade debt to price on the session.

- Date $MM Issuer (Priced *, Launch #)

- 02/23 $3.5B #Wells Fargo 11NC10 +138

- 02/23 $1.5B #Aon Corp $600M +5Y +97, $900M 30Y +170

- 02/23 $1.2B #Bio-Rad $400M 5Y +145, $800M 10Y +175

- 02/23 $1B #Prudential Fncl 30NC10 5.125%

- 02/23 $900M #Weyerhaeuser $450M 11Y +145, $450M 30Y +180

- 02/23 $800M #Centerpoint $300M 10Y +107, $50M 30Y +137

- 02/23 $700M #AutoNation10Y +190

- 02/23 $600M *PSP Capital 3Y FRN/SOFR +24

- 02/23 $500M Archer-Daniels Midland 10Y +100a

- 02/23 $1B Twitter 8NC investor calls

- 02/23 $Benchmark Rep of Chile investor calls

EGBs-GILTS CASH CLOSE: Long-End German Rally Stands Out

UK short-end yields easily outperformed German counterparts Wednesday, though it was a different story further down the curve.

- BoE speakers in focus throughout the session, first with Treasury Committee hearing including Bailey which was taken as marginally dovish; in the afternoon the short-end saw a modest rally on Tenreyro (dove)'s call for a "small amount of policy tightening".

- Bund / Buxl stood out for afternoon outperformance of Gilts and Tsys. While Ukraine-Russia escalation headlines were at least partly responsible, the lack of movement in the short-end (and UK long-end) stood in stark relief.

- Periphery spreads widened on renewed geopolitical risk-off.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4bps at -0.359%, 5-Yr is up 0.7bps at 0.008%, 10-Yr is down 1.5bps at 0.228%, and 30-Yr is down 2.9bps at 0.467%.

- UK: The 2-Yr yield is down 4.2bps at 1.296%, 5-Yr is down 3.1bps at 1.331%, 10-Yr is up 0.8bps at 1.479%, and 30-Yr is up 1.6bps at 1.564%.

- Italian BTP spread up 3.2bps at 171.3bps / Spanish up 1.3bps at 103.3bps

FOREX: FX Majors Exhibit Narrow Ranges Despite Weakness In Equities/Ruble

- The US dollar index is around 0.20% firmer as renewed weakness in equity indices has seen haven-tied FX be supported. With that said, major currency pairs are largely taking a back seat to the broader moves in global markets.

- EURUSD has traded on the backfoot, in line with the stronger dollar, however, still remains above the 1.1300 mark and has struggled to gather any momentum to the downside. Similarly, USDJPY has remained pegged to the 115.00 level, clocking just a 27-pip range on Wednesday.

- Slightly more in play with the risk-off dynamics has been the Swiss Franc, rising just over 0.5% against the Euro, outshone only by NZD which has retained a good portion of the RBNZ induced gains earlier on Wednesday.

- Naturally, the pain has been most evident in the Russian Ruble, declining 2.95% as of writing. USDRUB has extended above the November 2020 highs north of the 81.00 mark.

- Gains this week have resulted in a break of resistance at 80.4155, Jan 26 high. This confirmed a resumption of the underlying uptrend and signals scope for a climb towards 81.5675 and 82.3602, the 2.00 and 2.236 projection of the Feb 10 - 11 - 16 price swing.

- BoE Governor Bailey is due to deliver pre-recorded opening remarks at the BOE's First Annual BEAR Conference tomorrow at 1315GMT/0815ET. The US data docket is headlined by the second reading of Q4 US GDP. Also, potential comments from Fed’s Mester due to speak about economic outlook and monetary policy at an online event hosted by the University of Delaware. Q&A is expected.

Thursday Data Roundup

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/02/2022 | 0030/1130 | * |  | AU | Private New Capex and Expected Expenditure |

| 24/02/2022 | 0700/0800 | ** |  | SE | Unemployment |

| 24/02/2022 | 0745/0845 | ** |  | FR | Consumer Sentiment |

| 24/02/2022 | 0900/1000 | * |  | IT | industrial orders |

| 24/02/2022 | 1100/1100 | ** |  | UK | CBI Distributive Trades |

| 24/02/2022 | 1315/1315 | | UK | BOE Bailey Intro at BEAR Research Conference | |

| 24/02/2022 | 1330/0830 | ** |  | US | Jobless Claims |

| 24/02/2022 | 1330/0830 | *** | | US | GDP (2nd) |

| 24/02/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 24/02/2022 | 1330/0830 | * |  | CA | Payroll employment |

| 24/02/2022 | 1500/1000 | *** | | US | new home sales |

| 24/02/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 24/02/2022 | 1600/1100 | ** | | US | DOE weekly crude oil stocks |

| 24/02/2022 | 1600/1700 |  | EU | ECB Schnabel panels BOE BEAR conference on Unwinding QE | |

| 24/02/2022 | 1600/1600 | | UK | BOE Broadbent moderates panel at BEAR Conference on QE | |

| 24/02/2022 | 1600/1100 | | US | San Francisco Fed's Mary Daly | |

| 24/02/2022 | 1610/1110 | | US | Atlanta Fed's Raphael Bostic | |

| 24/02/2022 | 1630/1130 | ** | | US | NY Fed Weekly Economic Index |

| 24/02/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 24/02/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 24/02/2022 | 1700/1200 | | US | Cleveland Fed's Loretta Mester | |

| 24/02/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 25/02/2022 | 2330/0830 | ** |  | JP | Tokyo CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.