Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Bullard Sees Fed Less Behind The Curve Than Critics Say

- MNI BRIEF: Fed’s Bullard Sees Rates As High As 3.5% This Year

- MNI BRIEF: Yellen - CBDC Would Be Major Challenge Taking Years

- EU BACKS RUSSIAN COAL EMBARGO IN FIFTH ROUND OF SANCTIONS, Bbg

- FED BULLARD: CURRENT FED POLICY IS TOO LOW BY ABOUT 300 BASIS POINTS, Bbg

US

FED: The Federal Reserve is less behind the curve than many observers think, St. Louis Fed President James Bullard said Thursday, because the central bank's enhanced credibility since the 1970s Great Inflation means markets adjust faster to forward guidance.

- The recent rise in two-year note yields to around 2.5% leaves a narrower gap between market expectations for tightening and traditional Taylor rule models than Fed critics believe, Bullard said in prepared remarks to the University of Missouri.

- “Credible forward guidance means market interest rates have increased substantially in advance of tangible Fed action," he said. "This provides another definition of ‘behind the curve,’ and the Fed is not as far behind based on this definition.” For more see MNI Policy main wire at 0905ET.

- "We have a strong interest in ensuring that innovation does not lead to a fragmentation in international payment architectures," she said. "I don’t yet know the conclusions we will reach, but we must be clear that issuing a CBDC would likely present a major design and engineering challenge that would require years of development, not months," she said, adding she shares President Biden's urgency to pull forward research to understand the challenges and opportunities a CBDC could present to American interests.

- More government regulation is needed for "responsible innovation" and to police the proliferation of cryptocurrency and other digital assets and to ward off fraudulent and illicit transactions, Yellen said at American University, in her first speech about cryptocurrency since President Joe Biden signed an executive order on digital assets in March.

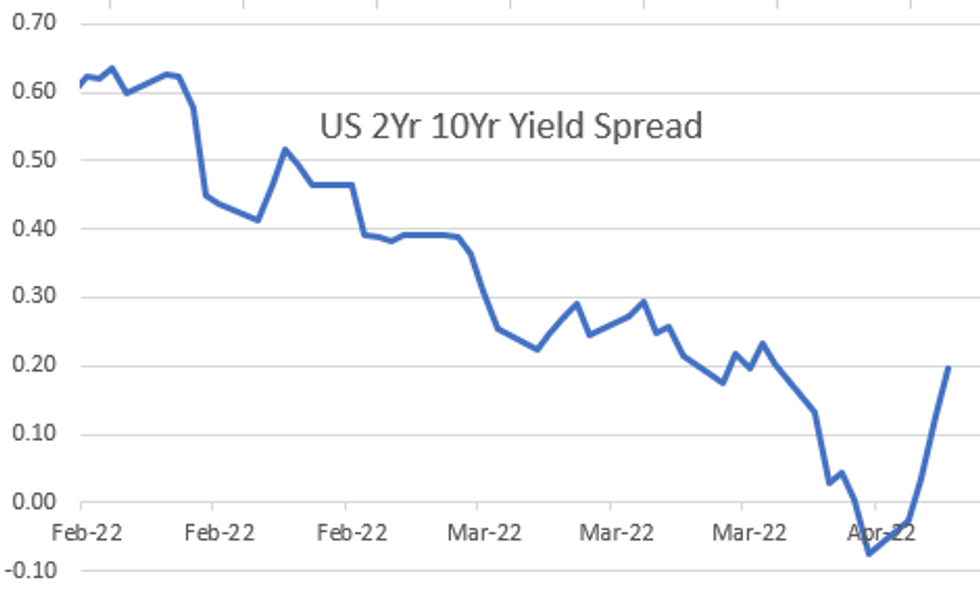

US TSYS: 2s10s Yield Curve Appr 30Bp Steeper on Wk

Tsys holding mixed levels after the bell, curves steeper with long end underperforming -- 10s-30s holding narrow range/near lows since noon.

- Nothing really new from StL Fed Bullard comments on economy/monetary policy this morning, save perhaps that current policy is "about 300bp too low", and stresses importance of taking recession red flag yield curve inversions seriously.

- Currently, 2s10s nearly 30bp off Sunday evening inverted low of -9.531 at +19.708 while 3s, 5s and 7s remain inverted or near inversion vs. 10s (+0.208, -4.370, -7.347 respectively).

- At 120-16 (-6) June 10Y futures remain above key support of 120-04+ (Low Dec 12/13 2018, cont); if yields continue to rise -- next key psychological support of 120-00.

- Limited data, no scheduled Fed speakers or Treasury supply:

- Apr-8 1000 Wholesale Trade Sales MoM (2.1%, 2.1%)

- Apr-8 1000 Wholesale Inventories MoM (4.0%, 0.8%)

- The 2-Yr yield is down 0.8bps at 2.4636%, 5-Yr is up 1.9bps at 2.7008%, 10-Yr is up 6bps at 2.6578%, and 30-Yr is up 5.9bps at 2.6847%.

OVERNIGHT DATA

- U.S. WEEKLY JOBLESS CLAIMS AT 166,000 LAST WEEK; EST. 200,000

- U.S. CONTINUING CLAIMS ROSE TO 1,523K LAST WEEK; EST. 1,302K

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 155.41 points (0.45%) at 34649.88

- S&P E-Mini Future up 34 points (0.76%) at 4509.5

- Nasdaq up 68.5 points (0.5%) at 13955.77

- US 10-Yr yield is up 6 bps at 2.6578%

- US Jun 10Y are down 7.5/32 at 120-14.5

- EURUSD down 0.0023 (-0.21%) at 1.0872

- USDJPY up 0.19 (0.15%) at 124

- WTI Crude Oil (front-month) up $0.46 (0.48%) at $96.69

- Gold is up $5.86 (0.3%) at $1931.15

- EuroStoxx 50 down 22.68 points (-0.59%) at 3802.01

- FTSE 100 down 35.89 points (-0.47%) at 7551.81

- German DAX down 73.54 points (-0.52%) at 14078.15

- French CAC 40 down 37.15 points (-0.57%) at 6461.68

US TSY FUTURES CLOSE

- 3M10Y +5.844, 197.04 (L: 185.899 / H: 198.04)

- 2Y10Y +7.038, 19.237 (L: 11.618 / H: 21.622)

- 2Y30Y +6.984, 22.034 (L: 14.851 / H: 27.126)

- 5Y30Y +4.085, -1.686 (L: -6.118 / H: 3.104)

- Current futures levels:

- Jun 2Y up 2.625/32 at 105-20.25 (L: 105-19.125 / H: 105-23.875)

- Jun 5Y up 2.5/32 at 113-14.5 (L: 113-13.25 / H: 113-25.5)

- Jun 10Y down 6.5/32 at 120-15.5 (L: 120-12.5 / H: 121-06.5)

- Jun 30Y down 1-8/32 at 144-06 (L: 143-28 / H: 146-04)

- Jun Ultra 30Y down 1-25/32 at 169-04 (L: 168-06 / H: 172-05)

US 10Y FUTURES TECH: (M2) Downtrend Intact

- RES 4: 125-01 50-day EMA

- RES 3: 124-18 High Mar 21

- RES 2: 123-04 High Mar 31 and a key resistance

- RES 1: 122-10 High Apr 5

- PRICE: 120-16+ @ 1530ET Apr 7

- SUP 1: 120-04+ Low Dec 12/13 2018 (cont)

- SUP 2: 120.00 Low Dec 6 2018 (cont) and psychological support

- SUP 3: 119-22 Low Dec 12 2018 (cont)

- SUP 4: 119-04+ Low Dec 3 2018 (cont)

Treasuries traded to a fresh contract low Wednesday. The move lower this week confirms a resumption of the primary downtrend and marks an extension of the bearish price sequence of lower lows and lower highs. Moving average studies are also pointing south and attention is on the 120.00 handle next. Key short-term trend resistance has been defined at 123-04, the Mar 31 high.

US EURODOLLAR FUTURES CLOSE

- Jun 22 +0.005 at 98.355

- Sep 22 +0.020 at 97.665

- Dec 22 +0.030 at 97.150

- Mar 23 +0.045 at 96.845

- Red Pack (Jun 23-Mar 24) +0.055 to +0.055

- Green Pack (Jun 24-Mar 25) steady to +0.040

- Blue Pack (Jun 25-Mar 26) -0.045 to -0.015

- Gold Pack (Jun 26-Mar 27) -0.10 to -0.06

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00686 at 0.32114% (-0.00615/wk)

- 1 Month +0.03671 to 0.48814% (+0.05057/wk)

- 3 Month +0.00243 to 0.98886% (+0.02686/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00086 to 1.50257% (+0.01343/wk)

- 1 Year -0.02857 to 2.21486% (+0.04329/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $77B

- Daily Overnight Bank Funding Rate: 0.32% volume: $254B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.30%, $905B

- Broad General Collateral Rate (BGCR): 0.30%, $332B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $322B

- (rate, volume levels reflect prior session)

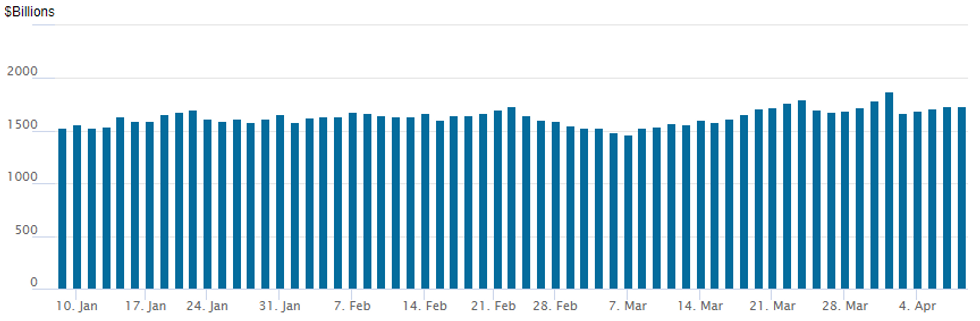

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage inches higher: 1,734.424B w/ 85 counterparties from prior session 1,731.472B. Compares to all-time high of $1,904.582B on Friday, December 31.

PIPELINE: $3B Keurig Dr Pepper Launched

- Date $MM Issuer (Priced *, Launch #)

- 04/07 $1.5B *JBIC 3Y SOFR+39

- 04/07 $3B #Keurig Dr Pepper $1B 7Y +125, $850M 10Y +145, $1.15B 30Y +185

- 04/07 $2.7B #Take-Two $1B 2Y +85, $600M 3Y +90, $600M 5Y +100, $500M 10Y +135

- 07/07 $1.75B *Republic of Angola 10Y 8.75%

- 07/07 $700M #South32 10Y +175

- 07/07 $Benchmark Royal Bank of Canada 3Y +75, 3Y SOFR, 5Y +95, 10Y +135

- 04/07 $Benchmark Freeport Indonesia 5Y +255a, 10Y +310a, 3Y +390a

EGBs-GILTS CASH CLOSE: Yield Ascent Continues

Bund and Gilt yields finished off session highs but continued their overall ascent Thursday.

- The accounts of the last ECB meeting were interpreted hawkishly, suggesting the GC may be more proactive than expected in tightening policy.

- Separate from the ECB-induced move for EGBs, 10Y Gilt yields underperformed hit another post-2016 high before pulling back slightly.

- A first poll to show Le Pen defeating Macron in the French election met with little market reaction.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.6bps at -0.014%, 5-Yr is up 3.7bps at 0.477%, 10-Yr is up 3.4bps at 0.681%, and 30-Yr is up 2.1bps at 0.811%.

- UK: The 2-Yr yield is up 0.8bps at 1.47%, 5-Yr is up 1.3bps at 1.517%, 10-Yr is up 2.7bps at 1.73%, and 30-Yr is up 4.5bps at 1.864%.

- Italian BTP spread unchanged at 165.3bps / Spanish down 0.7bps at 98.3bps

FOREX: Greenback Edges Higher As G10 FX Ranges Remain Contained

- The greenback has edged slightly higher (DXY +0.15%) on Thursday, however, G10 currency ranges were narrow and price action much more subdued amid a light data calendar.

- Following yesterday’s weakness, the likes of AUD, NZD and CAD extended their short-term downward bias and are bottom of the G10 pile on Thursday, all shedding between 0.35-0.50%.

- USDCAD has recovered from its recent lows and maintains a firmer tone. Tuesday’s price action, in Japanese candlestick terms, is a long-legged doji and a potential short-term reversal signal, suggesting potential for a correction near-term. The small continuation higher has narrowed the gap with the 50-day EMA that intersects at 1.2632 today.

- EURUSD traded either side of unchanged despite printing fresh lows for the week at 1.0865 during early European trade. $6.36 billion of option expiries between 1.0875/1.0936, including 2.13bn of 1.0900 strikes acted as a magnet for the pair.

- USDJPY remains towards the upper end of the days range, hovering just below 124.00. On the upside, clearance of 125.09, the Mar 28 high and bull trigger, is required to confirm a resumption of the primary uptrend.

- RBA Financial Stability Review features in a quiet APAC schedule. Friday’s highlight is March employment data for Canada.

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/04/2022 | 0001/0101 | ** |  | UK | IHS Markit/REC Jobs Report |

| 08/04/2022 | 0600/0800 | ** |  | NO | Norway GDP |

| 08/04/2022 | 0700/0900 | ** |  | ES | Industrial Production |

| 08/04/2022 | 0800/1000 | * |  | IT | Retail Sales |

| 08/04/2022 | 1115/1315 |  | EU | ECB Panetta at IESE Business School Conference | |

| 08/04/2022 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 08/04/2022 | 1400/1000 | ** |  | US | Wholesale Trade |

| 08/04/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.