Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI US: NY Fed Research On Import Price Passthrough

- MNI FED: Two Regional Feds Voted For 100bp Discount Rate Hike

- MNI US: US To Host Indo-Pacific Economic Framework Ministerial In Sept

- MNI US: ADP To Include Pay Details In New Methodology

- AP: US To Announce USD$3B Ukr Arms Package To Mark Independence Day

US

FED: Minutes of the discount-rate meetings in July show directors at two regional Federal Reserve banks (St Louis and Minneapolis Fed) favored a 100bp July rate hike in the discount rate to further tighten the cost of borrowing for banks from the discount window, whilst directors at the Kansas City Fed favored a 50bp increase.

- This pushed the discount rate to 2.5%, in line with the 75bp hike in the Fed Funds range to 2.25-2.5% on Jul 27.

- The pick-up in core goods inflation in the current expansion is the strongest across all expansions since the 1970s. The pick-up in service prices meanwhile is more modest, but has accelerated recently. The pattern is a reversal of the typical inflation dynamics over the last twenty years. * Against that backdrop, the impact is unsurprisingly larger for the traded sector: a 10% increase in import prices and wages is associated with a 7.4% increase in PPI in 2021, compared to only a 3% increase in 2013-20. Around 70% of the effect flows through the marginal cost channel.

- That compares with an increase from 1.6% in the pre-pandemic period to 3.4% for the non-trade sector.

- The event, co-hosted by Trade Representative Katherine Tai and Commerce Secretary Gina Raimondo, will be the first in-person Ministerial of the group and take place in Los Angeles, California.

- A Commerce Department Statement says the event, "builds on the constructive virtual meetings with 13 Indo-Pacific partners held this year before and after President Biden officially launched the IPEF to develop a high-standard and inclusive economic framework that will fuel economic activity and investment, promote sustainable and inclusive economic growth, and benefit workers and consumers across the region."

- It will helpfully capture pay as well: "Pay Insights - ADP's new pay measure uniquely captures the salaries of the same cohort of almost 10 million individual employees over a 12-month period. The new monthly measure will report median annual pay growth by industry, business establishment size, U.S. region, gender, and age. Quarterly reports focused on pay will expand on key areas of interest, such as bonuses, benefits, and gender gaps."

- According to AP sources, the new package will be focused on long-term defense strategies rather than servicing immediate military needs - a departure from previous arms packages suggesting that Ukraine may soon be in a position to undertake a long planned counterattack in the south-east of the country.

- AP: "U.S. officials told The Associated Press that the package is expected to be announced Wednesday, the day the war hits the six-month mark and Ukraine celebrates its independence day. The money will fund contracts for drones, weapons and other equipment that may not see the battlefront for a year or two, they said."

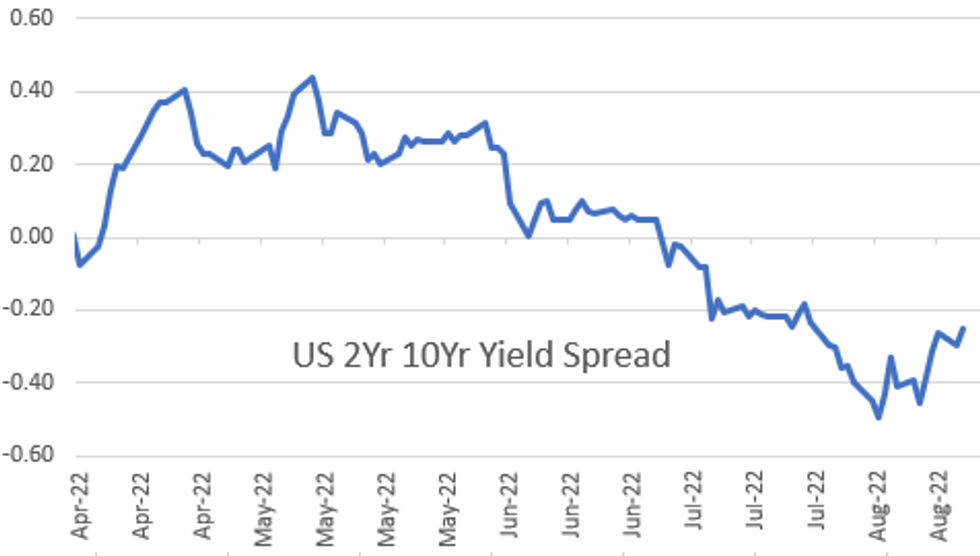

US TSYS: Curve Consistently Steeper

Inside range for Tsys after the bell, curves steeper (2s10s +5.282 at -24.663) with bonds weaker but off early session lows (30YY currently 3.2584% vs. 3.2840% high / 3.1995% low).- Steeper curves the consistent theme on the day as futures see-sawed on the day, heavier volumes (TYU2>1.7M) more tied to Sep/Dec rolls rather than data that kicked things off.

- Tsys extended highs overnight after soft European PMIs (France, Germany, EU in line or better than estimated but still sub-50, mixed UK w/ Mfg 46.0 vs. 51.0 est, Services 52.5 vs. 51.6 est) - only to extend session lows (no obvious headline driver) in the lead-up to US PMIs.

- Tsys have rebounded back near overnight highs, yield curves bull steepening (2s10s +3.648 at -26.297) after US PMIs come out weaker than estimated, particularly Services (44.1 vs. 49.8 est). Further impetus from slump in New Home Sales for July: 511k vs. 575k est, and 590k prior.

- Tsy futures pare gains yest again after $44B 2Y note auction (91282CFG1) tailed: 3.307% high yield vs. 3.290% WI; 2.49x bid-to-cover vs. 2.58x prior.

- Focus remains on KC Fed's annual Jackson Hole Economic Symposium: Reassessing Constraints on the Economy and Policy, starts Friday w/ Chairman Powell speaking at 1000ET (0800 local), text is expected but no Q&A. Markets keen on pivot after cooling data or will the Fed maintain hawkish stance to squelch inflation.

- Currently, The 2-Yr yield is down 1.2bps at 3.2975%, 5-Yr is up 1.8bps at 3.1753%, 10-Yr is up 3.2bps at 3.0461%, and 30-Yr is up 2.5bps at 3.2508%.

OVERNIGHT DATA

- US FLASH AUG MANUF PMI 51.3 (FCST 51.8); JUL 52.2

- US FLASH AUG SERVICES PMI 44.1 (FCST 49.8); JUL 47.3

- US FLASH AUG COMPOSITE PMI 45.0; JUL 47.7

- US JUL NEW HOME SALES -12.6% TO 0.511M SAAR

- US JUN NEW HOME SALES REVISED TO 0.585M SAAR

- US AUG. RICHMOND FED FACTORY INDEX AT -8 (-2 expected, 0 prior)

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 124.42 points (-0.38%) at 32939.88

- S&P E-Mini Future down 3.5 points (-0.08%) at 4137.5

- Nasdaq up 34.9 points (0.3%) at 12417.05

- US 10-Yr yield is up 3.2 bps at 3.0461%

- US Sep 10Y are down 1/32 at 117-22

- EURUSD up 0.0023 (0.23%) at 0.9965

- USDJPY down 0.69 (-0.5%) at 136.79

- Gold is up $10.29 (0.59%) at $1746.60

- EuroStoxx 50 down 5.7 points (-0.16%) at 3652.52

- FTSE 100 down 45.68 points (-0.61%) at 7488.11

- German DAX down 36.34 points (-0.27%) at 13194.23

- French CAC 40 down 16.72 points (-0.26%) at 6362.02

US TSY FUTURES CLOSE

- 3M10Y +1.21, 27.909 (L: 16.776 / H: 29.78)

- 2Y10Y +4.59, -25.355 (L: -33.091 / H: -24.175)

- 2Y30Y +3.968, -4.884 (L: -12.933 / H: -1.559)

- 5Y30Y +0.771, 7.378 (L: 3.6 / H: 11.998)

- Current futures levels:

- Sep 2Y up 3.375/32 at 104-18.5 (L: 104-14.75 / H: 104-22.25)

- Sep 5Y up 1.75/32 at 111-12.5 (L: 111-07 / H: 111-24)

- Sep 10Y down 1.5/32 at 117-21.5 (L: 117-14.5 / H: 118-07)

- Sep 30Y down 12/32 at 137-17 (L: 137-03 / H: 138-22)

- Sep Ultra 30Y down 5/32 at 149-28 (L: 148-29 / H: 151-07)

US 10YR FUTURE TECHS: (U2) Bear Cycle Still In Play

- RES 4: 122-02 High Aug 2 and key resistance

- RES 3: 120-29 High Aug 4

- RES 2: 119-31/120-22 High Aug 15 / 10

- RES 1: 118-14/119-04+ Intraday high / 20-day EMA

- PRICE: 118-05 @ 16:23 BST Aug 23

- SUP 1: 117-14+ Low Jul 21 & Aug 23 and key near-term support

- SUP 2: 117-07 61.8% retracement of the Jun 14 - Aug 2 bull cycle

- SUP 3: 116-26+ Low Jun 29

- SUP 4: 116-11 Low Jun 28

Treasuries maintain a softer tone and the contract has traded lower Monday. 118-05, 50.0% of the Jun 14 - Aug 2 bull cycle, has been cleared and this signals scope for an extension towards 117-14+ next, the Jul 21 low. Price has recently cleared a trendline support drawn from the Jun 14 low and this reinforces the current bearish theme. Initial firm resistance is at 119-31, the Aug 15 high.

US EURODOLLAR FUTURES CLOSE

- Sep 22 +0.013 at 96.640

- Dec 22 +0.005 at 96.025

- Mar 23 +0.030 at 95.985

- Jun 23 +0.045 at 96.055

- Red Pack (Sep 23-Jun 24) +0.040 to +0.065

- Green Pack (Sep 24-Jun 25) -0.02 to +0.025

- Blue Pack (Sep 25-Jun 26) -0.035 to -0.03

- Gold Pack (Sep 26-Jun 27) -0.035 to -0.035

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00457 to 2.31257% (-0.00857/wk)

- 1M +0.01628 to 2.44371% (+0.05700/wk)

- 3M +0.01715 to 2.99686% (+0.03915/wk) * / **

- 6M +0.00000 to 3.56557% (+0.01800/wk)

- 12M +0.05900 to 4.09114% (+0.07528/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 2.99686% on 8/23/22

- Daily Effective Fed Funds Rate: 2.33% volume: $91B

- Daily Overnight Bank Funding Rate: 2.32% volume: $284B

- Secured Overnight Financing Rate (SOFR): 2.28%, $994B

- Broad General Collateral Rate (BGCR): 2.26%, $393B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $384B

- (rate, volume levels reflect prior session)

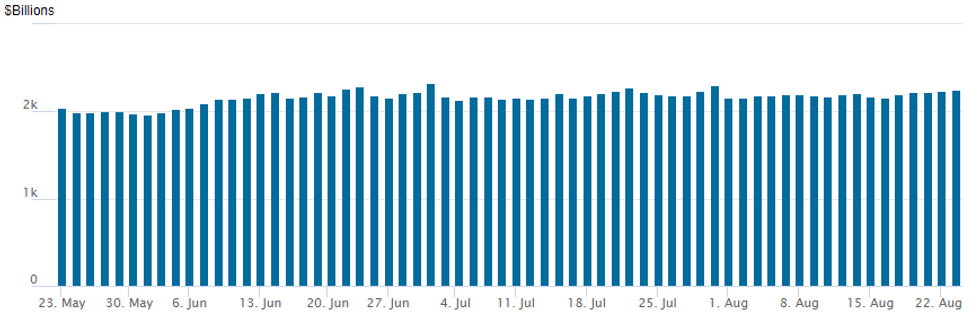

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage inches higher to $2,250.718B w/ 97 counterparties vs. $2,235.665B prior session. Record high still stands at $2,329.743B from Thursday June 30.

PIPELINE: $600M MassMutual 3Y Launched, SEK Rolled to Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 08/23 $4B *EIB 5Y Sustainability Awareness bond SOFR+38

- 08/23 $600M #MassMutual 3Y +83

- Rolled to Wednesday:

- 08/24 $Benchmark Swedish Export Cr Corp (SEK) 2Y SOFR+23a

EGBs-GILTS CASH CLOSE: UK Underperformance Continues

A weak set of U.S. data dragged German yields back down Tuesday afternoon, but UK yields kept marching higher - with 10Y vs Bund spreads reaching their widest since March.

- A weak French flash PMI initially set a dovish tone for the day, pushing core yields to session lows, though a more encouraging German reading more than reversed the drop. UK services PMI held up well, though manufacturing disappointed.

- While the German curve twist steepened, Gilts bear flattened once again: 2Y yields set their 5th consecutive new post-2008 high close, off 4bp from session highs. UK 5Y underperformed on the curve, piercing the 2.50% mark for the first time since 2011.

- Greece notably underperformed its periphery peers with a double-digit spread widening.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 4.1bps at 0.854%, 5-Yr is down 1.7bps at 1.104%, 10-Yr is up 1.3bps at 1.319%, and 30-Yr is up 3.6bps at 1.487%.

- UK: The 2-Yr yield is up 8.9bps at 2.719%, 5-Yr is up 11.9bps at 2.5%, 10-Yr is up 6.2bps at 2.576%, and 30-Yr is up 4.4bps at 2.883%.

- Italian BTP spread up 0.6bps at 233.3bps / Greek up 11.6bps at 261.9bps

FOREX: USD Index Set To End Winning Streak Following Softer US Data

- A trifecta of weaker-than-expected data from the US weighed on the greenback during the US session prompting the dollar index to post 0.45% declines on Tuesday. This looks set to end a significant winning streak that has seen the index rise close to 4.5% in less than two weeks, with today’s pre-data high just two pips shy of the July/cycle highs at 109.29.

- US Manufacturing and Services PMI, Richmond Fed Manufacturing and New Home Sales data all fell below median surveyed estimates, sparking a strong kneejerk reaction lower for the USD. As has been the case over most recent US data releases, USDJPY was extremely volatile and had a steep selloff, falling roughly 150 pips to intra-day lows of 135.81. The pair has since bounced back to around 136.70 but remains down 0.57% on Tuesday.

- With major equity indices in more of a consolidation mode on Tuesday, the likes of AUD, NZD and CAD were able to capture near 0.75% gains. SEK and NOK are the strongest G10 performers as ~4% gains for crude futures have underpinned the 1.3% advance for the Norwegian Krone.

- EURUSD weakness did extend heading into the start of European trading, however, 0.9900 proved firm support following slightly better than expected European Flash PMI’s. Potential short covering took EURUSD back above yesterday’s breakdown point of 0.9952 shortly before the US data, however, the poor US prints fuelled a quick spike back above parity to 1.0018 highs. Given the short-term bearish technical developments and the ongoing concerns regarding the European energy crisis, the pair fell quickly back below 1.0000 and remains just 0.25% higher on the day, relatively underperforming it’s G10 peers and the magnitude of the DXY adjustment.

- US Durable Goods and Pending Home Sales are the only data points on Wednesday. Thursday will bring the minutes of the ECB's July policy meeting and the German IFO business survey. Focus remains on Fed Chair Powell’s remarks from Jackson Hole, scheduled for Friday.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/08/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 24/08/2022 | 1230/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 24/08/2022 | 1230/0830 | ** | | US | durable goods new orders |

| 24/08/2022 | 1400/1000 | ** | | US | NAR pending home sales |

| 24/08/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 24/08/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 24/08/2022 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.