Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

US

US: Employment data insight.

- Non-farm payrolls surged in January, rising 517k vs consensus 189k, whilst the annual benchmark revision left a notably stronger than first thought trend through 2H22 and with strong revisions for hours worked.

- The unemployment rate fell to the lowest since 1969, an even more hawkish surprise than analyst survey skew had indicated, despite population control-adjusted household employment was notably softer.

- Against that backdrop, AHE was one of the weaker areas of the report, recording a monthly pace in January that could be consistent with Powell’s abating a little bit, but even that came with upward revisions.

- Fed terminal pricing closed 12bps higher at 5.02% and has since continued to push onto 5.09%, whilst 2H23 cuts have been trimmed significantly to 34bps from 50bps prior to the release.

- A US Treasury Department official said that Europe's response to the IRA, the Green Deal Industrial Plan, would also be subject to discussions.US Treasury Dept Official: "We look forward to working with our European allies on accelerating investments in green technologies.

- The U.S. is committed to partnering with counterparts in Europe and globally on building resilient clean energy supply chains."

US TSYS: No React to Atlanta Fed Bostic, Focus on Fed Chair Talk on Tuesday

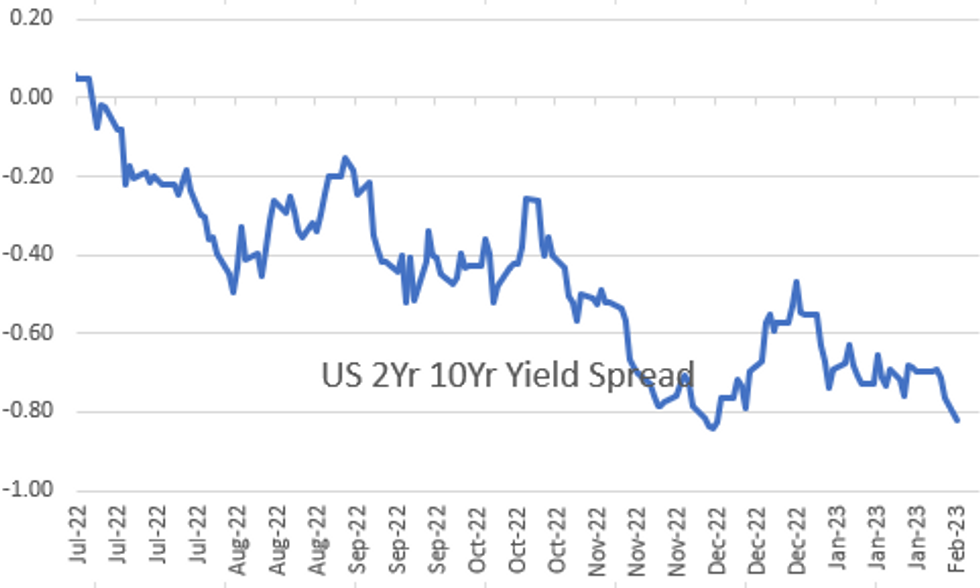

Still weaker, off opening levels - while yield curves extend inversion back near mid-Dec's multi decade lows: 2s10s currently -83.160 (-6.163) vs. Dec 7, 2022 low of -85.240 - last seen late 1981.

- Heavy volumes, TYH3 over 1.7M (two-thirds of which occurred in the first half) as FI markets continue to price in higher rates for long following last Fri's blowout January jobs surge (+517k vs. +189k est) while annual benchmark revision left a notably stronger than first thought trend through 2H22 and with strong revisions for hours worked.

- FED'S BOSTIC SAYS HIS BASE CASE IS STILL FOR TWO MORE HIKES

- FED’S BOSTIC SAYS MAIN JOB IS TO CONTROL INFLATION

- BOSTIC: NEED TO STUDY IF JAN. JOBS REPORT WAS ANOMALOUS

- Fed Chair Powell expected Tue at Economic Club of Washington interview (no text) time adjustment to Chairman Powell event to 1230ET, though Fed site has 1240ET. Link to Economic Club of DC..

- Fed VC Barr on financial inclusion (text and moderated Q&A) at 1400ET.

- Massive option volumes, particularly in SOFR derivatives favoring low delta puts and put spds on net.

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 94.34 points (-0.28%) at 33831.68

- S&P E-Mini Future down 31.25 points (-0.75%) at 4116

- Nasdaq down 140.1 points (-1.2%) at 11865.74

- US 10-Yr yield is up 11.3 bps at 3.638%

- US Mar 10-Yr futures are down 30/32 at 113-15.5

- EURUSD down 0.007 (-0.65%) at 1.0725

- USDJPY up 1.46 (1.11%) at 132.65

- WTI Crude Oil (front-month) up $1.01 (1.38%) at $74.41

- Gold is up $1.16 (0.06%) at $1866.15

- EuroStoxx 50 down 52.53 points (-1.23%) at 4205.45

- FTSE 100 down 65.09 points (-0.82%) at 7836.71

- German DAX down 130.52 points (-0.84%) at 15345.91

- French CAC 40 down 96.84 points (-1.34%) at 7137.1

US TSY FUTURES CLOSE

- 3M10Y +11.731, -102.773 (L: -114.932 / H: -102.586)

- 2Y10Y -4.974, -81.971 (L: -82.995 / H: -77.681)

- 2Y30Y -10.623, -78.502 (L: -79.539 / H: -69.487)

- 5Y30Y -9.923, -14.599 (L: -15.646 / H: -5.373)

- Current futures levels:

- Mar 2-Yr futures down 9.5/32 at 102-11.625 (L: 102-11 / H: 102-21.25)

- Mar 5-Yr futures down 22.75/32 at 108-12 (L: 108-10.75 / H: 109-02)

- Mar 10-Yr futures down 30/32 at 113-15.5 (L: 113-14 / H: 114-11.5)

- Mar 30-Yr futures down 1-03/32 at 128-31 (L: 128-24 / H: 130-02)

- Mar Ultra futures down 1-09/32 at 141-17 (L: 141-08 / H: 143-00)

(H3) Clears Key Short-term Support

- RES 4: 116-00 High Feb 2

- RES 3: 115-22+ High Feb 3

- RES 2: 114-21+ 20-day EMA

- RES 1: 114-11+ Intraday high

- PRICE: 113-17+ @ 1520ET Feb 6

- SUP 1: 113-17+ Feb 6 Low & 61.8% retracement of the Dec 30 - Jan 19 bull run

- SUP 2: 112-29 76.4% retracement of the Dec 30 - Jan 19 bull run

- SUP 3: 112-18+ Low Jan 5

- SUP 4: 112-09 Trendline support drawn from the Oct 21 low

A sharp pullback in Treasury futures Friday and a bearish start to this week’s activity, highlights a downward cycle and signals scope for continuation lower. The contract has breached 114-05+, the Jan 30 low and a short-term bear trigger. Note that price has also breached the 50-day EMA. This opens 113-17+ next - a level tested on Monday - a Fibonacci retracement. On the upside, initial firm resistance is seen at 114-21+, the 20-day EMA.

US EURODOLLAR FUTURES CLOSE

- Mar 23 -0.030 at 94.950

- Jun 23 -0.120 at 94.70

- Sep 23 -0.160 at 94.695

- Dec 23 -0.180 at 95.005

- Red Pack (Mar 24-Dec 24) -0.21 to -0.20

- Green Pack (Mar 25-Dec 25) -0.185 to -0.125

- Blue Pack (Mar 26-Dec 26) -0.12 to -0.105

- Gold Pack (Mar 27-Dec 27) -0.10 to -0.09

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.01186 to 4.56457% (+0.24800 total last wk)

- 1M +0.01643 to 4.58829% (-0.00701 total last wk)

- 3M +0.00900 to 4.84314% (+0.00885 total last wk)*/**

- 6M +0.08228 to 5.13971% (-0.04486 total last wk)

- 12M +0.15329 to 5.40443% (-0.06500 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.84314% on 2/6/23

- Daily Effective Fed Funds Rate: 4.58% volume: $104B

- Daily Overnight Bank Funding Rate: 4.57% volume: $284B

- Secured Overnight Financing Rate (SOFR): 4.55%, $1.216T

- Broad General Collateral Rate (BGCR): 4.52%, $470B

- Tri-Party General Collateral Rate (TGCR): 4.52%, $459B

- (rate, volume levels reflect prior session)

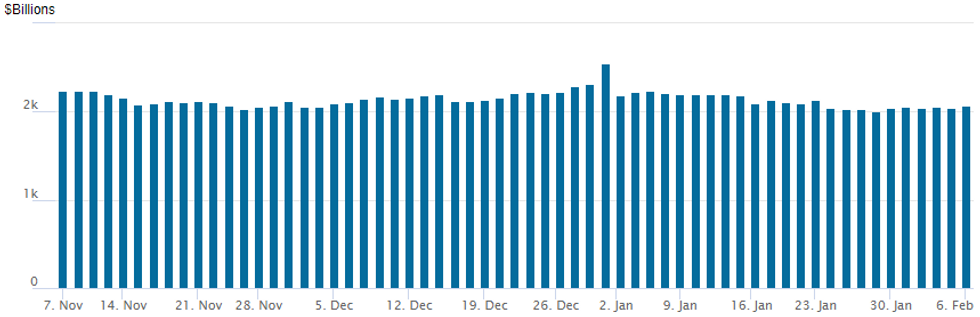

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,072.261B w/ 103 counterparties vs. prior session's $2,041.217B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

PIPELINE: $4B Nextera 4Pt Launched, Total Issuance Monday at $12.5B

- Date $MM Issuer (Priced *, Launch #)

- 02/06 $4B #Nextera $1.25B 5Y +110, $600M 7Y +125, $1B 10Y +140, $1.15B 30Y +155

- 02/06 $3B #T-Mobile $1B 5Y +118, $1.25B +10Y +143, $750M 30Y tap +165a

- 02/06 $2B #Northrop Grumman $1B 10Y +108, $1B 30Y +128

- 02/06 $1.5B #Deutsche Bank 11NC10 +345

- 02/06 $1.2B #Micron Technology 7Y tap +210a, 10Y +225a

- 02/06 $800M #Becton Dickinson 5Y +188

- 02/06 $Benchmark Comcast investor calls

- 02/06 $Benchmark Intel investor calls

- Expected Tuesday:

- 02/07 $Benchmark Export Development bank Canada (EDC) 5Y SOFR+41a

- 02/07 $Benchmark Swedish Export Bank (SEK) 7Y SOFR +48a

- 02/07 $Benchmark World Bank (IBRD) 7Y SOFR +49a

- 02/07 $Benchmark CDP Fncl 3Y +60a

- 02/07 $Benchmark EIB 10Y SOFR+50a

- 02/07 $1.25B Alliant Holdings 5NC2

- Chatter for new supply in near future:

- 02/-- $Benchmark OPT Bank (Hungary)

FOREX: USD Grinds Higher Extending Friday’s Sentiment, JPY & EMFX Underperform

- Currency markets had a similar feel to the end of last week on Monday as the post-payrolls relief rally for the greenback extended which sees the USD index registering gains of around 0.6% approaching the APAC crossover.

- With little data on the docket and an vacant speaker slate, the price action was uneventful as the USD steadily climbed throughout US trade. With core fixed income continuing to drift lower in the as markets reassess terminal rate pricing higher, the Japanese yen is among the worst performers in G10.

- This comes alongside overnight reports in the Nikkei that cited current BoJ deputy governor Amamiya as the name-in-the-frame to take over from Kuroda in a few months' time. Despite very swift denials from government spokespeople, markets have taken the prospect of an Amamiya adminstration as a signal of continuity for ultra-easy policy. USDJPY climbed as high as 132.90, within close proximity of touted resistance at 132.96, the 50-day exponential moving average.

- While other major currencies declined with a similar magnitude to the USD move, emerging market currencies were notable victims of the greenback squeeze.

- In CEEMEA, USDHUF (+2.20%) and USDZAR (+1.00%) are standouts and in LatAm, both the Mexican and Colombian pesos have come under further pressure. USDMXN is now roughly 4% above last Thursday’s low, which notably was a new marginal low from February 2020. Today’s break of 19.11 strengthens a bullish theme and signals scope for a stronger short-term recovery, towards the 19.40 handle initially with the December highs around 19.90 marking a more significant chart point.

- The RBA kicks off Tuesday’s overnight docket where it is widely expected to hike rates 25bp to 3.35% given the elevated Q4 CPI data. Thus, the focus is likely to be on any change in tone of the statement and indications of how the RBA's forecasts have changed.

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/02/2023 | 0001/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 07/02/2023 | 0030/1130 | ** |  | AU | Trade Balance |

| 07/02/2023 | 0330/1430 | *** | | AU | RBA Rate Decision |

| 07/02/2023 | 0645/0745 | ** |  | CH | Unemployment |

| 07/02/2023 | 0700/0800 | ** |  | DE | Industrial Production |

| 07/02/2023 | 0745/0845 | * |  | FR | Foreign Trade |

| 07/02/2023 | 0800/0900 | ** |  | ES | Industrial Production |

| 07/02/2023 | 0900/0900 | | UK | BOE Ramsden Intro at UK Women in Economics Event | |

| 07/02/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 07/02/2023 | 1015/1015 | | UK | BOE Pill Chairs UK Women in Economics Panel | |

| 07/02/2023 | 1330/0830 | ** |  | US | Trade Balance |

| 07/02/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 07/02/2023 | 1430/1430 | | UK | BOE Cunliffe Speech at UK Finance | |

| 07/02/2023 | 1500/1000 | ** | | US | IBD/TIPP Optimism Index |

| 07/02/2023 | 1700/1800 |  | EU | ECB Schnabel in Finanzwende e.V. Webinar | |

| 07/02/2023 | 1730/1230 |  | CA | BOC Governor Macklem speech/press conference in Quebec City | |

| 07/02/2023 | 1740/1240 | | US | Fed Chair Jerome Powell | |

| 07/02/2023 | 1800/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 07/02/2023 | 1900/1400 | | US | Fed Vice Chair Michael Barr | |

| 07/02/2023 | 2000/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.