Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI FED: Fed Gov Bowman Still Willing To Hike If Needed

- MNI US INTERVIEW: Lagging Fed To Cut 100BP This Year- LaVorgna.

- MNI US DATA: House Price Growth Continued To Fade In December

- MNI US DATA: Consumer Confidence Misses Whilst Labor Differential Reverses Gain

- MNI US DATA: Core Durable Goods Orders See Softer Trend With Downward Revision

US

FED BRIEF (MNI): Fed Gov Bowman Still Willing To Hike If Needed. Federal Reserve Governor Michelle Bowman reiterated her openness Tuesday to raising interest rates again if progress on inflation stalls or reverses, though she judges that current policy is restrictive and will bring inflation back to 2% over time.

- "I remain willing to raise the federal funds rate at a future meeting should the incoming data indicate that progress on inflation has stalled or reversed," she said.

US INTERVIEW (MNI): Lagging Fed To Cut 100BP This Year- LaVorgna. The Federal Reserve is likely to cut interest rates by one percentage point this year and officials should already be lowering rates given that inflation has fallen sharply and is set to continue declining, former White House economist Joseph LaVorgna told MNI.

NEWS

US (MNI) White House Meeting On Government Shutdown Underway Shortly.

President Biden is shortly due to meet with the four Congressional leaders – House Speaker Mike Johnson (R-LA), Senate Majority Leader Chuck Schumer (D-NY), Senate Minority Leader Mitch McConnell (R-KY), and House Minority Leader Hakeem Jeffries (D-NY) - at the White House.

SECURITY (MNI): Hezbollah Likely To Halt Fighting In Event Of Israel-Hamas Ceasefire

Reuters reportingthat, according to two sources, Lebanon-based Hezbollah, "will halt fire on Israel" if Hamas agrees to a ceasefire with Israel in Gaza, "unless Israeli forces keep shelling Lebanon."

US (MNI): Johnson Says House Will "Address" Ukraine But Border Is Priority

House Speaker Mike Johnson (R-LA) has told reporters that he "bought up the border issue repeatedly," in a recently concluded White House meeting with President Biden and Congressional leaders. The meeting also included national security officials and CIA Director Bill Burns, likely to increase pressure on Johnson to move on Ukraine aid.

US TSYS Yields Resume Climb Ahead Midweek GDP/PCE Metrics

- Tsys holding near session lows after the bell, extending session lows in the second half after briefly posting gains on decent $42B 7Y note auction (91282CKC4) stop: 4.327% high yield vs. 4.330% WI; 2.58x bid-to-cover vs. 2.57x last month.

- Additional factors helping rise in Tsy yields (10Y +.0296 at 4.3091%), month end extensions (0.11%), and stocks making a late session comeback (SPX Eminis at 5090.25).

- Fast two-way trade reported after lower than expected Durable Goods Orders (-6.1% vs. -5.0% est); ex-Trans (-0.3% vs. 0.2% est, prior down revised to -0.1% from 0.5%). Cap Goods Orders Nondef Ex Air in line with 0.1% est while prior was down-revised to -0.6% from 0.2%.

- Additional data: FHFA house prices increased by less than expected in Dec, 0.1% M/M (cons 0.3) after 0.31% M/M, its softest monthly print since Jan’23. Conf. Board consumer confidence saw a sizeable miss in February, falling to 106.7 (cons 115.0) after a downward revised 110.9 (initial 114.8).

- Mar'24 10Y futures currently -2 at 109-17.5 vs. 109-15 low. The trend direction in Treasuries is unchanged and remains down with the contract trading closer to its recent lows. Price has pierced 109-17, 50.0% of the Oct - Dec bull cycle. A clear break of this retracement would strengthen the bearish condition and signal scope for an extension towards 108-19+, the 61.8% Fibonacci level. On the upside, initial firm resistance is seen at 110-24+, the 50-day EMA.

- Look ahead, Wednesday data calendar includes GDP, PCE, Wholesale/Retail Inv, Fed Speak.

OVERNIGHT DATA

US DATA (MNI): Core Durable Goods Orders See Softer Trend With Downward Revision. Durable goods orders fell by more than expected in preliminary January data, -6.1% M/M (cons -5.0%) after a downward revised -0.3% (initial 0.0%).

- As is nearly always the case, it’s down to non-defense aircraft orders (-59%).

- Core durable goods orders meanwhile were as expected with 0.1% M/M but it followed a sizeable downward revision to -0.6% (initial 0.2) in Dec.

- Core shipments saw a decent beat, increasing 0.8% M/M (cons 0.1) after an upward revised 0.1% (initial 0.0), which at least bodes well for early Q1 momentum even forward-looking orders were on net softer.

- Core orders are up 0.4% and shipments 0.1% on a 3M/3M annualized basis. As we have noted before, both hold up well compared to business surveys in contraction territory.

US DATA (MNI): Consumer Confidence Misses Whilst Labor Differential Reverses Gain. Conf. Board consumer confidence saw a sizeable miss in February, falling to 106.7 (cons 115.0) after a downward revised 110.9 (initial 114.8).

- The present situation drove the latest decline and downward revision, but expectations also softened slightly – both are at lows since Nov.

- Within the details, the labor differential declined after a notable downward revision to Jan, falling to 27.8 after 31.7 (initial 35.7).

- Recall that the jump to 35.7 had left it at the highest since April, and preceded a bumper payrolls report which also included a surprise decline in the u/e rate.

- It’s still relatively elevated compared to the 25 averaged through Aug-Dec, but far less so than appeared this time last month.

US DATA (MNI): House Price Growth Continued To Fade In December. FHFA house prices increased by less than expected in Dec, 0.1% M/M (cons 0.3) after 0.31% M/M, its softest monthly print since Jan’23.

- The S&P CoreLogic 20-city index meanwhile was in line as it increased 0.21% M/M (cons 0.2) after an upward revised 0.24% (initial 0.15).

- The two combined have cooled in the past two to three months after growing strongly from early 2023 to Q3.

- FHFA prices are 48% higher than pre-pandemic levels vs 45% for the S&P CoreLogic 20-city.

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 88 points (-0.23%) at 38982.18

- S&P E-Mini Future up 4.75 points (0.09%) at 5085.5

- Nasdaq up 52.4 points (0.3%) at 16029.31

- US 10-Yr yield is up 2.8 bps at 4.3072%

- US Mar 10-Yr futures are down 1.5/32 at 109-18

- EURUSD down 0.0005 (-0.05%) at 1.0846

- USDJPY down 0.23 (-0.15%) at 150.47

- WTI Crude Oil (front-month) up $1.14 (1.47%) at $78.73

- Gold is down $1.32 (-0.07%) at $2029.77

- European bourses closing levels:

- EuroStoxx 50 up 21.45 points (0.44%) at 4885.74

- FTSE 100 down 1.28 points (-0.02%) at 7683.02

- German DAX up 133.26 points (0.76%) at 17556.49

- French CAC 40 up 18.58 points (0.23%) at 7948.4

US TREASURY FUTURES

- 3M10Y +5.219, -108.726 (L: -117.335 / H: -107.541)

- 2Y10Y +4.456, -39.647 (L: -45.322 / H: -39.44)

- 2Y30Y +6.228, -26.509 (L: -33.552 / H: -26.122)

- 5Y30Y +4.076, 12.189 (L: 7.934 / H: 12.401)

- Current futures levels:

- Mar 2-Yr futures down 0.125/32 at 101-25.375 (L: 101-24.5 / H: 101-27.875)

- Mar 5-Yr futures down 0.5/32 at 106-9 (L: 106-07.25 / H: 106-15.25)

- Mar 10-Yr futures down 2/32 at 109-17.5 (L: 109-15 / H: 109-28)

- Mar 30-Yr futures down 7/32 at 118-12 (L: 118-06 / H: 119-09)

- Mar Ultra futures down 14/32 at 124-19 (L: 124-15 / H: 125-28)

US 10Y FUTURE TECHS: (H4) Trend Direction Remains Down

- RES 4: 111-16+ High Feb 7

- RES 3: 111-07 High Feb 13

- RES 2: 110-24+ 50-day EMA

- RES 1: 110-13 20-day EMA

- PRICE: 109-17 @ 1445 ET Feb 27

- SUP 1: 109-09 Low Feb 23

- SUP 2: 109-05+ Low Nov 28

- SUP 3: 108-19+ 61.8% of the Oct 19 - Dec 27 bull phase

- SUP 4: 108-14 Low Nov 15

The trend direction in Treasuries is unchanged and remains down with the contract trading closer to its recent lows. Price has pierced 109-17, 50.0% of the Oct - Dec bull cycle. A clear break of this retracement would strengthen the bearish condition and signal scope for an extension towards 108-19+, the 61.8% Fibonacci level. On the upside, initial firm resistance is seen at 110-24+, the 50-day EMA.

SOFR FUTURES CLOSE

- Mar 24 +0.008 at 94.678

- Jun 24 +0.005 at 94.865

- Sep 24 steady00 at 95.145

- Dec 24 -0.005 at 95.455

- Red Pack (Mar 25-Dec 25) -0.005 to +0.005

- Green Pack (Mar 26-Dec 26) +0.005 to +0.010

- Blue Pack (Mar 27-Dec 27) -0.01 to +0.005

- Gold Pack (Mar 28-Dec 28) -0.02 to -0.01

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00226 to 5.32626 (+0.00213/wk)

- 3M +0.00535 to 5.34316 (+0.01259/wk)

- 6M +0.01353 to 5.29249 (+0.01898/wk)

- 12M +0.02286 to 5.09384 (+0.02141/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.739T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $670B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $658B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $98B

- Daily Overnight Bank Funding Rate: 5.31% (+0.00), volume: $281B

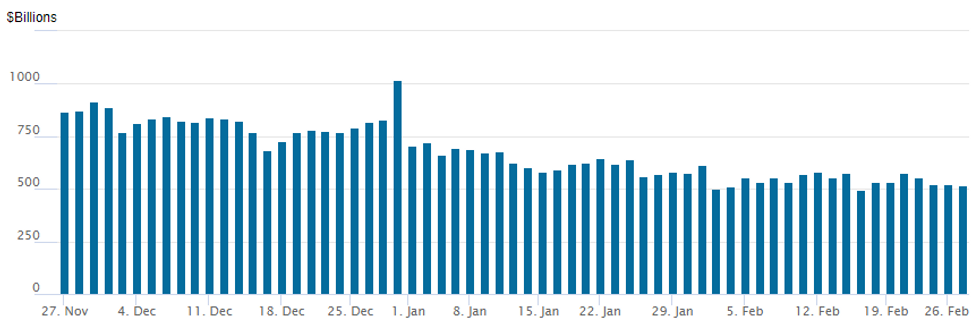

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage recedes to $519.725B vs. 524.959B Monday; compares to $493.065B on Thursday, Feb 15 -- the lowest since early June 2021 .

- Meanwhile, the latest number of counterparties at 84 from 81 Monday (compares to 65 on January 16, the lowest since July 7, 2021).

PIPELINE: Still Waiting For Rabobank to Launch

- At least $15.6B to price Tuesday, waiting for Rabobank 3-parter details:

- Date $MM Issuer (Priced *, Launch #)

- 2/27 $3.5B *Asian Development Bank (ADB) 5Y SOFR+38

- 2/27 $2B *Agence Francaise de Developpement (AFD) 5Y +52

- 2/27 $2B #Public Inv Fund (PIF; SA wealth fund) Sukuk 7+85

- 2/27 $2B *Bank of England 3Y +10

- 2/27 $1.75B #SEB $650M 3Y +73, $350M 3Y SOFR+89, $750M 5Y +117

- 2/27 $1.6B #SoCal Edison $600M 2Y +62, $600M 5Y +83, $400M 30Y +135

- 2/27 $1B *KommuneKredit WNG 3Y SOFR+32

- 2/27 $1B #SMFG PerpNC10.25 6.6%

- 2/27 $750M #Willis NA 30Y +150

- 2/27 $Benchmark Rabobank 3Y +55, 3Y SOFR+71, 6NC5 +112

- May price Wednesday

- 2/27 $500M Kommunalbanken 4Y SOFR+40a

- 2/28 $1B NRW Bank WNG 3Y SOFR+34a

EGBs-GILTS CASH CLOSE: Weakness Continues As Supply Weighs Again

UK and German yields rose for a second consecutive session Tuesday, with Gilts underperforming Bunds.

- Supply was again the theme, capping nascent gains throughout the morning, with early trade subdued and well within prior sessions' ranges.

- Hedging activity associated with EGB syndications (Slovenia 10Y for E3bln, France 30Y for E8bln, both on the high end of expectations) priced by early afternoon saw Gilts and Bunds head to session lows, recovering only briefly as US consumer confidence data came in weaker than expected.

- BoE's Ramsden gave away little on his monetary policy outlook in a speech today ("looking for more evidence about how entrenched [key indicators of inflation] persistence will be and therefore about how long the current level of Bank Rate will need to be maintained"

- Yields closed on the highs (10Y Gilts at the highest closing yield since late November). The German curve finished bear steeper, with the UK's bear flattening. Periphery spreads closed mixed, with BTPs and GGBs outperforming with modest tightening to Bunds, and Spanish/Portuguese spreads unchanged.

- Wednesday's schedule includes Eurozone confidence data, with central bank appearances including ECB's Muller and BOE's Mann. The focus remains on Euro inflation Thursday and Friday, however.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.4bps at 2.928%, 5-Yr is up 1.9bps at 2.472%, 10-Yr is up 2.4bps at 2.464%, and 30-Yr is up 3.3bps at 2.607%.

- UK: The 2-Yr yield is up 3.7bps at 4.349%, 5-Yr is up 3.8bps at 4.082%, 10-Yr is up 3.4bps at 4.196%, and 30-Yr is up 2.1bps at 4.658%.

- Italian BTP spread down 1.4bps at 143.8bps / Spanish down 0.1bps at 89.2bps

FOREX G10 Currencies Registering Minimal Adjustments As US PCE Awaited

- Very narrow ranges for major currency pairs on Tuesday, with the likes of EURUSD and GBPUSD continuing to operate in the middle of their 30 pip daily ranges. The early shift lower for US yields moderately weighed on the greenback and saw USDJPY try lower towards session lows of 150.12. However, a 5bp retracement for the US 2-year saw USDJPY rise back above 150.55 as we approach the APAC crossover.

- No change for the USDJPY trend outlook which remains bullish, and the latest pause appears to be a bull flag formation. A resumption of the trend would pave the way for a climb towards 151.91/95, the Nov 13 ‘23 high and the Oct 1 ‘22 high and major resistance. On the downside, initial firm support lies at 149.41, the 20-day EMA. A break would signal scope for a correction towards 148.01, the 50-day EMA.

- Plenty of focus on the overnight RBNZ decision and potential impact on NZD. The Bank’s mandate change coupled with NZ domestic data flow has led to some calling for a resumption of the hiking cycle, although this isn’t our Asia-Pac team’s base case.

- The NZD is marginally less susceptible to a hawkish ‘surprise’ than NZ rates given already long positioning (per CFTC data), although there has seemingly been some reduction in longs ahead of the event.

- NZD/USD levels to watch: Resistance: 22 Feb high ($0.6218), Support: 15 Feb low ($0.6080).

- AUD/NZD levels to watch: Support: ’24 low/’23 low (NZD1.0570/60), Resistance: Feb 20 high/20-day EMA (NZD1.0649/1.0655).

- Wednesday’s APAC session is also highlighted by Australian CPI which precedes the RBNZ decision. In the US, focus turns to the second reading of Q4 GDP on Wednesday before Thursday’s January PCE deflator. European inflation readings will start to cross from Thursday.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/02/2024 | 0030/1130 | *** |  | AU | CPI Inflation Monthly |

| 28/02/2024 | 0030/1130 | *** | | AU | Quarterly construction work done |

| 28/02/2024 | 0100/1400 | *** |  | NZ | RBNZ official cash rate decision |

| 28/02/2024 | 0700/0800 | ** |  | SE | PPI |

| 28/02/2024 | 0700/1500 | ** |  | CN | MNI China Liquidity Index (CLI) |

| 28/02/2024 | 0900/1000 | ** |  | IT | ISTAT Consumer Confidence |

| 28/02/2024 | 0900/1000 | ** | | IT | ISTAT Business Confidence |

| 28/02/2024 | 1000/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 28/02/2024 | 1000/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 28/02/2024 | 1100/1200 | | EU | ECB's Lagarde and Cipollone in G20 and CB Governors meeting | |

| 28/02/2024 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 28/02/2024 | 1330/0830 | * |  | CA | Current account |

| 28/02/2024 | 1330/0830 | * | | CA | Payroll employment |

| 28/02/2024 | 1330/0830 | *** | | US | GDP |

| 28/02/2024 | 1330/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 28/02/2024 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 28/02/2024 | 1530/1530 |  | UK | BOE's Mann at FT future forum event 'The economic outlook..' | |

| 28/02/2024 | 1700/1200 | | US | Atlanta Fed's Raphael Bostic | |

| 28/02/2024 | 1715/1215 | | US | Boston Fed's Susan Collins | |

| 28/02/2024 | 1745/1245 | | US | New York Fed's John Williams | |

| 29/02/2024 | 2350/0850 | * |  | JP | Retail sales (p) |

| 29/02/2024 | 2350/0850 | ** | | JP | Industrial production |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.