Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Bond-Lead Rally, Stocks Strong Too

Tsys see-sawed higher Thursday, partially driven by same factors pushing equities back to early Tuesday levels: improved market sentiment over COVID curbs on China travel as testing has not revealed new variants while "European health officials called screenings and restrictions on travelers from China unjustified" Bbg.

- Knee-jerk post-data (weekly claims in-line at 225k, continuing claims higher than est at 1.710M) 30Y Bond sale quickly reversed, 30YY falling back to 3.9479% from 3.9773% post-data high.

- Futures see-sawed higher as risk sentiment for stocks improved. Note, yield curves reversed Wed's steepening, 2s10s currently -6.416 at -53.885.

- Tsys pare gains briefly after $35B 7Y note auction (91282CGB1) tailed: 3.921% high yield vs. 3.907% WI; 2.45x bid-to-cover vs. 2.33x last month. Indirect take-up climbs to 68.08% vs. 61.89% prior; Direct take-up: 16.17% vs. 16.57% prior; Primary dealer take-up falls to 15.75% vs. 21.35% prior auction.

- Friday -- quiet end to the last trading day of 2022 w/ MNI Chicago PMI (40.0 est) release at 0945ET. FI/FX trading floor closes at 1300ET, but GLOBEX closes at 1700ET. LINK

OVERNIGHT DATA

- US JOBLESS CLAIMS +9K TO 225K IN DEC 24 WK

- US PREV JOBLESS CLAIMS REVISED TO 216K IN DEC 17 WK

- US CONTINUING CLAIMS +0.041M to 1.710M IN DEC 17 WK

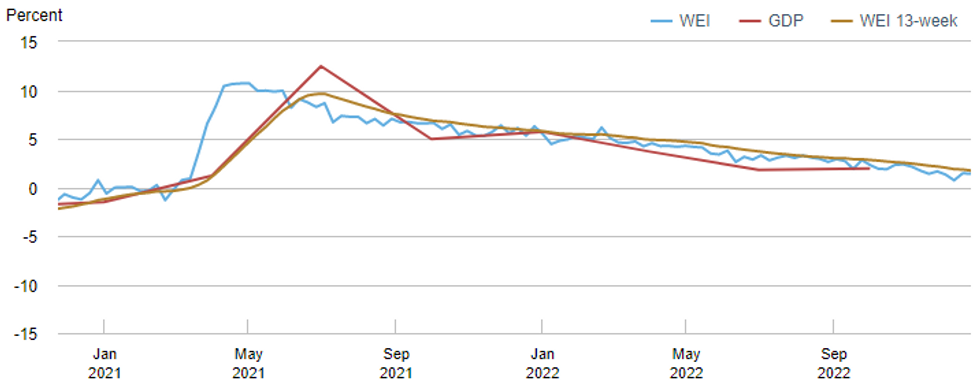

NY Fed: Weekly Economic Index (WEI)

NY Federal Reserve/MNI

NY Fed explains the latest WEI decline to 1.42% from 1.43% the week prior is tied to "to a decrease in steel production, and a rise in initial unemployment insurance claims, which more than offset rises in retail sales, tax withholding, consumer confidence, and railroad traffic. Electricity output was not updated due to data unavailability. Fuel sales were not released this week due to the Christmas Day holiday."

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 376.46 points (1.15%) at 33254.09

- S&P E-Mini Future up 68 points (1.79%) at 3876

- Nasdaq up 261.3 points (2.6%) at 10475.11

- US 10-Yr yield is down 4.4 bps at 3.8391%

- US Mar 10-Yr futures are up 6.5/32 at 112-12.5

- EURUSD up 0.0062 (0.58%) at 1.0674

- USDJPY down 1.49 (-1.11%) at 132.98

- WTI Crude Oil (front-month) down $0.64 (-0.81%) at $78.33

- Gold is up $12.43 (0.69%) at $1816.86

- EuroStoxx 50 up 41.25 points (1.08%) at 3850.07

- FTSE 100 up 15.53 points (0.21%) at 7512.72

- German DAX up 146.12 points (1.05%) at 14071.72

- French CAC 40 up 62.98 points (0.97%) at 6573.47

US TSY FUTURES CLOSE

3M10Y -3.79, -60.429 (L: -64.719 / H: -56.004)2Y10Y -6.434, -53.903 (L: -54.774 / H: -47.725)

2Y30Y -6.61, -45.331 (L: -46.971 / H: -38.7)

5Y30Y -3.766, -3.715 (L: -5.486 / H: 0.595)

Current futures levels:

Mar 2-Yr futures down 1.25/32 at 102-19.25 (L: 102-18.875 / H: 102-22)

Mar 5-Yr futures up 1.75/32 at 107-31.5 (L: 107-28.75 / H: 108-03.75)

Mar 10-Yr futures up 6.5/32 at 112-12.5 (L: 112-05 / H: 112-17.5)

Mar 30-Yr futures up 15/32 at 125-12 (L: 124-20 / H: 125-24)

Mar Ultra futures up 31/32 at 134-22 (L: 133-13 / H: 135-12)

US 10YR FUTURE TECHS: (H3) Trading At Its Recent Lows

- RES 4: 115-26 2.00 proj of the Oct 21 - 27 - Nov 3 price swing

- RES 3: 115-14 50% Aug - Oct Downleg

- RES 2: 114-23/115-11+ High Dec 19 / 13 and the bull trigger

- RES 1: 113-16 20-day EMA

- PRICE: 112-15 @ 1400ET Dec 29

- SUP 1: 112-04 Low Dec 28

- SUP 2: 111-27+ 61.8% retracement of the Nov 3 - Dec 13 rally

- SUP 3: 111-01 76.4% retracement of the Nov 3 - Dec 13 rally

- SUP 4: 110-22 Low Nov 10

Treasury futures remain soft and the contract traded lower Wednesday, extending the pullback from 115-11+, the Dec 13 high and key resistance. The move lower has resulted in a print below support at 112-11+, the Nov 21 low. A clear break of this level would open 111-27+, a Fibonacci retracement level. On the upside, the 20-day EMA, at 113-16, marks a firm resistance. A break is required to ease the current bearish pressure.

US EURODOLLAR FUTURES CLOSE

- Mar 23 +0.010 at 94.950

- Jun 23 steady at 94.870

- Sep 23 -0.010 at 94.960

- Dec 23 -0.015 at 95.240

- Red Pack (Mar 24-Dec 24) -0.015 to -0.005

- Green Pack (Mar 25-Dec 25) +0.005 to +0.020

- Blue Pack (Mar 26-Dec 26) +0.015 to +0.020

- Gold Pack (Mar 27-Dec 27) +0.025 to +0.040

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00457 to 4.31186% (-0.00485/wk)

- 1M -0.01486 to 4.36871% (-0.01815/wk)

- 3M +0.02490 to 4.75386% (+0.02833/wk)*/**

- 6M -0.01357 to 5.13757% (-0.01557/wk)

- 12M -0.02772 to 5.44257% (-0.00129/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.77857% on 11/30/22

- Daily Effective Fed Funds Rate: 4.33% volume: $99B

- Daily Overnight Bank Funding Rate: 4.32% volume: $255B

- Secured Overnight Financing Rate (SOFR): 4.30%, $1.005T

- Broad General Collateral Rate (BGCR): 4.26%, $379B

- Tri-Party General Collateral Rate (TGCR): 4.26%, $362B

- (rate, volume levels reflect prior session)

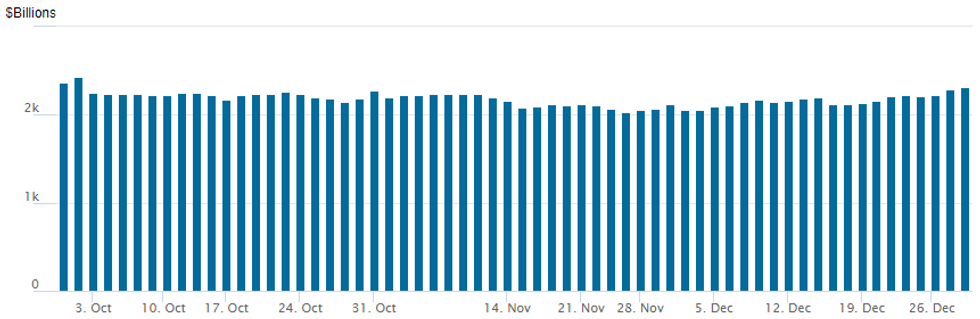

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,308.319B w/ 104 counterparties vs. $2,293.003B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/12/2022 | 0800/0900 | *** |  | ES | HICP (p) |

| 30/12/2022 | 0800/0900 | * |  | CH | KOF Economic Barometer |

| 30/12/2022 | 1330/0830 | ** |  | US | WASDE Weekly Import/Export |

| 30/12/2022 | 1445/0945 | ** | | US | MNI Chicago PMI |

| 30/12/2022 | 1600/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 31/12/2022 | 0130/0930 | *** |  | CN | CFLP Manufacturing PMI |

| 31/12/2022 | 0130/0930 | ** | | CN | CFLP Non-Manufacturing PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.