Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Executive Summary:

- ECB Slows PEPP; Big Decisions In December

- U.S. Jobless Claims Fall to New Pandemic Low

- Fed's Bowman Says Appropriate to Taper This Year

- BOC Will Reinvest QE Assets At Least Until it Hikes Rates

- MNI: Fed's Poor Fiscal Modeling Risks Inflation

US 10y30y Yield Spread Resumes Flattening Post-Auction:

Source: MNI/Bloomberg

NORTH AMERICA NEWS:

MNI BRIEF: Fed's Bowman Says Appropriate to Taper This Year

Federal Reserve Governor Michelle Bowman said Thursday she is optimistic about growth of the U.S. economy despite some "noise in the data" such as last week's jobs figures, and signaled that she is likely to support pulling back on some of the central bank's extraordinary measures later this year.

MNI BRIEF: Slowing US Retail Imports Highlight Inventory Woes

Retail imports disappointed in August, suggesting sales growth slipped through the month as pandemic-related supply chain disruptions capped inventories, the National Retail Federation said Thursday. Twenty-Foot Equivalent Units rose to an estimated 2.27 million in August, according to the NRF's monthly Global Port Tracker. That would still be the strongest August on record, but would fall short of the 2.37 million TEU forecast by the NRF last month.

MNI BRIEF: Fed's Kaplan Sees 2.6% 2022 PCE 'With Upside Risk'

Dallas Fed President Robet Kaplan said Thursday he sees inflation hitting 4% this year and 2.6% next year. "I would guess the risk is to the upside," he said.

MNI: BOC Will Reinvest QE Assets At Least Until it Hikes Rates

The Bank of Canada is looking to eventually scale back QE purchases to a pace of CAD4 billion to CAD5 billion a month to stabilize the size of its balance sheet against maturing assets, Governor Tiff Macklem said Thursday, and remain in a reinvestment mode at least until policy makers decide to raise the record low policy interest rate.

MNI INTERVIEW: Fed's Poor Fiscal Modeling Risks Inflation

The Federal Reserve's failure to fully incorporate fiscal developments into its monetary policy analysis risks a return to a 1970s-style capture of the central bank that could cement higher inflation or even generate a loss of confidence in U.S. debt, Eric Leeper, a former Atlanta Fed and Fed board economist, told MNI.

EUROPE NEWS:

MNI STATE OF PLAY: ECB Slows PEPP; Big Decisions In December

The European Central Bank announced a "moderately lower" pace of bond buying under its pandemic emergency purchase programme on Thursday, with President Christine Lagarde indicating that a decision on what will follow PEPP could be announced in December.

MNI: EU Debt Pact Review To Resume After German Elections

The European Commission will move quickly to relaunch its review of the bloc's rules on debt and borrowing once the German elections are out of the way, but negotiations will last until the end of 2022 at the earliest, officials told MNI.

MNI: Norwegian House Prices To Cool Fast As Norges Tightens

Norwegian house price inflation, cited as a factor by Norges Bank as it prepares to hike rates for the first time in the cycle this month, looks set to slow sharply as monetary policy tightens, experts including a former Norges Bank researcher told MNI.

DATA

MNI DATA BRIEF: U.S. Jobless Claims Fall to New Pandemic Low

U.S. jobless claims dropped by another 35,000 in the latest week to 310,000, the lowest level since the start of the Covid pandemic, suggesting the labor market is on a steady improvement path.

US TSYS SUMMARY: Solid 30y Auction Sees Yields Slide, Curve Flatten

- Throughout European and early US hours, Treasury futures traded inside the minor uptrend posted off the week's Tuesday lows, with a firm EGB market adding some upside impetus. This move accelerated following the 30yr re-opening, which saw solid demand evident in the higher-than-average bid/cover and a steep decline in dealer takedown at just 13.1% against an 18% average.

- 10y yields slid sharply on release of the results, pressing below 1.30% to narrow the gap with last Friday's NFP-induced 1.2617%.

- The solid showing from the 30yr line saw the longer-end outperform, resulting in a flatter curve from the belly outwards.

- PPI data takes focus Friday, with markets expecting factory gate prices to bump up to 8.2% on a final demand basis, and 6.6% ex-food & energy.

EGBs-GILTS CASH CLOSE: Bunds And BTPs Rally As Lagarde "Isn't Tapering"

Bunds rallied and BTPs outperformed as the ECB decision came basically in line with expectations, with the Governing Council set to "moderately lower" the PEPP purchase pace.

- As Pres Lagarde put it in the press conference, "the lady isn't tapering" - and Bund and BTP yields fell the most in months. BTP 10Y spreads narrowed to tightest since Aug 16 (102.1bp).

- There was a mild retracement near the cash close as Reuters cited sources saying the agreed PEPP target was E60-70B, which was in line with expected but perhaps dashing some lingering dovish hopes.

- Gilts strengthened but underperformed eurozone bonds.

- Friday's docket includes UK July GDP and appearances by ECB's Lagarde and Villeroy.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.5bps at -0.711%, 5-Yr is down 2.9bps at -0.661%, 10-Yr is down 3.8bps at -0.361%, and 30-Yr is down 3.9bps at 0.128%.

- UK: The 2-Yr yield is up 1.4bps at 0.224%, 5-Yr is up 1.4bps at 0.411%, 10-Yr is down 0.8bps at 0.736%, and 30-Yr is down 1.7bps at 1.063%.

- Italian BTP spread down 4.4bps at 103.1bps / Spanish down 2.5bps at 66.4bps

FOREX: GBP and Haven FX Lead G10 Charge As Dollar Strength Abates

- The greenback's ascent this week was halted on Thursday as US yields slipped lower and risk sentiment waned. JPY and CHF were the biggest movers, rallying just over 0.5% as equities also took a knock. The dollar index retreated 0.2%.

- Equally buoyant was GBP, that took its lead from a technically induced move lower in EURGBP during European hours, breaking back below 0.8560. Late dollar weakness helped GBPUSD (+0.5%) regain some poise towards the best levels of the week.

- Notably narrow range for EURUSD (1.1805-1.1841) over the ECB statement and press conference. The single currency firmed slightly off the lows on reports that ECB to buy 60-70bln in PEPP per month (with flexibility), coinciding with Bund futures rolling off the session highs.

- The minor Thursday uptick does little to change the overarching outlook and need to top resistance at 1.1909, the Jul 30 and Sep 3 high to progress higher. The support to watch is 1.1735, Aug 27 low. A move through this support would instead suggest the recent rally is over.

- European industrial production data features in a quiet early calendar, however US PPI and Canadian August employment may prompt some action, headlining the US session data docket.

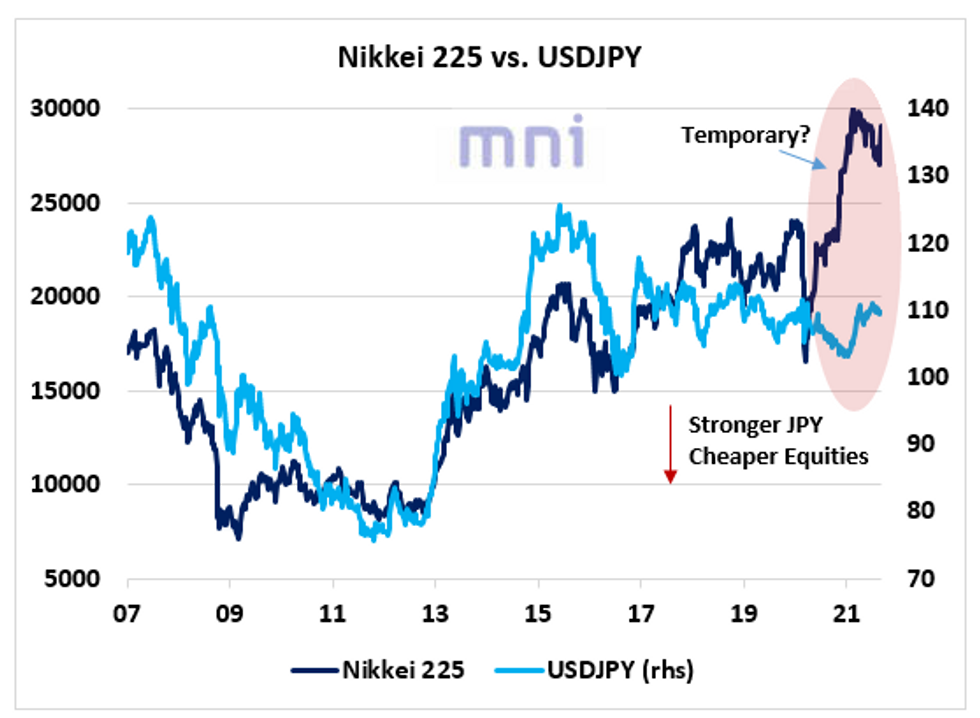

Can Equities Reach New Highs Without JPY 'Help'?

- In Japan, we have seen that the dynamics of the exchange rate (JPY) has had a significant impact on equities in the past 15 years; a cheaper currency has usually been associated with higher equities (and vise versa, 'Pavlovian' relationship).

- However, in the past year, while Japanese equities have experienced a significant recovery their March 2020 lows, the Yen has remained 'strong' against major crosses as investors have been constantly looking for 'hedges' due to rising uncertainty.

- As liquidity has been one of the major forces behind equities' strength, DM central banks' tapering poses a threat to risky assets.

- The chart below shows the significant divergence between USDJPY and the Nikkei 225 index in the past year.

- Can the divergence persists if DM starts tapering bond purchases?

Source: Bloomberg/MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.