Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI POLICY: Softer Trend Inflation Boosts Case For Fed Pause

- MNI INTERVIEW: BOC Needs Hawkish Footing - Ex Deputy Minister

- MNI WATCH: ECB Hikes 25Bp, Signals Peak May Be Near

- MNI Better Than Expected Jobless Claims Data, Ohio Partly Helps Initial

- MNI Core PPI Either Stronger Than Expected Or Line In August Depending On Measure

- MNI US Inflation Insight, Sep'23: CPI vs PCE Differences See Stronger Core Faded

US

FED: U.S. underlying inflation could be softer than official readings suggest, indicating the recent reduction of prices pressures is likely to persist and the Federal Reserve can achieve its mission of bringing inflation back to its 2% target over time without more interest rate increases.

- Fed officials arguing the central bank should stop raising interest rates are taking heart in the New York Fed's new Multivariate Core Trend inflation measure, which has declined for seven straight months to 2.76% in July. By comparison, the standard twelve-month headline PCE measure stood at 3.3% in July, while core PCE, seen by Fed officials as a better proxy for the underlying trend, was higher at 4.2%.

- An MCT reading below core PCE suggests a substantial part of core PCE is transitory while another significant portion reflects past inertia. Assuming there is no shock in the near future, core PCE could be expected to eventually converge with the MCT measure, which is already closer to the Fed's 2% inflation goal. For more see MNI Policy main wire at 1142ET.

US: Headline CPI accelerated to 0.6% M/M as expected in August on a surge in energy prices, but core CPI inflation was stronger than expected at 0.28% M/M (cons 0.2) after two months at 0.16% M/M.

- There were some large cross currents, but the broad takeaway was upside coming from increases in categories that might not be repeated in core PCE.

- There was a step back in the progress made in various dispersion and underlying metrics, but nevertheless the market reacted by seeing 2024 rate cuts increase by 7-8bps after a prior disinversion trend.

- Still, coming ahead of next week’s FOMC meeting and new dot plot, the ~100bp of cuts priced for 2024 is in line with the June dot plot, albeit from about a half hike lower starting point.

CANADA

BOC: Canada's central bank will remain focused on upside inflation risks so it is dangerous for investors to assume Governor Tiff Macklem is done hiking, former deputy finance minister Tim Sargent told MNI.

- “I don’t think the Bank can give them that certainty, and I don’t think the Bank ought to,” Sargent said Tuesday at the Canadian Association for Business Economics conference in Kingston, Ontario. “Is the Bank done? I think you can see why the governor doesn’t want to give hostages to fortune.”

- The Bank of Canada held its overnight rate at the highest since 2001 at 5% this month following increases at the prior two meetings. Many investors bet the cycle is done after 10 moves and a main reason Macklem didn't signal he could be done -- like he did early this year -- is to avoid a bond market rally that loosens financial conditions. For more see MNI Policy main wire at 1033ET.

EUROPE

ECB: Policymakers can both make clear their preference for holding policy rates flat-for-longer and stick to the line that they are data dependent, former Bank of England Deputy Governor for Monetary Policy and LSE professor Charles Bean told MNI.

- With central banks from the BOE to the Federal Reserve suggesting that they might hold rates at their peak for an extended period in a so-called “Table Mountain” approach, some including European Central Bank Executive Board Member Isabel Schnabel have pointed to a contradiction between committing to a flat rates stance whilst also promising policy will respond flexibly to incoming data.

- But Bean drew a distinction between maintaining rates at a high level and previous promises to keep them low. Low-for-long “is, if you like, committing to a period of excessive inflation in the future .. and is necessarily time-inconsistent as there is little incentive to go through with that bout of excessive future inflation once today’s lower-bound episode is past,” Bean said by email. For more see MNI Policy main wire at 0959ET.

US TSYS Rates Hold Lows After Stronger PPI, Stocks 1-Wk Highs

- Treasury futures trading sideways after quietly extending session lows in late trade, intermediates to bonds lead move off midmorning levels as curves rebounded: 3M10Y +6.674 at -118.025, 2Y10Y -.244 at -72.742 vs. -76.154 low.

- Current TYZ3 futures at 109.24 (-8.5) still above initial technical support of 109-03 (Sep 13 low) followed by 109-00 (round number support).

- No obvious headline driver for the drift lower in the second half (though markets await formal annc of a UAW strike, not to mention the impending shutdown as UIS Gov expected to run out of capital at the end of the month.

- Knock-on factors: stronger than expected PPI and lower than expected weekly claims reversed a post-ECB rate hike bid earlier (rally tied to policy statement that was less hawkish than expected).

- Stocks are grinding to new two week highs, ignoring for the moment projected rate hike increase in early 2024. Meanwhile, the US$ gains strength (BBDXY +3.4 to 1253.99), and crude prices forge higher: WTI +1.89 at 90.41.

- Friday focus: Import/Export Price index, Industrial Production/Capacity Utilization and UofM Sentiment.

OVERNIGHT DATA

- US JOBLESS CLAIMS +3K TO 220K IN SEP 09 WK

- US PREV JOBLESS CLAIMS REVISED TO 217K IN SEP 02 WK

- US CONTINUING CLAIMS +0.004M to 1.688M IN SEP 02 WK

- Initial claims fared better than expected in the week to Sep 9, only rising to 220k (cons 225k) from a marginally upward revised 217k (initial 216k).

- It saw another healthy decline in the four-week moving average to 225k from 230k, its lowest since early March and closing back in on the average level seen through 2019 having seen since March.

- The non-seasonally adjusted figure fell a sizeable -17k to 175k. There aren’t any particularly large contributions by state, although Ohio does lead the move lower with -3.5k as it continues a return to more typical levels after some unusually elevated levels in recent months.

- Continuing claims meanwhile also came in better than expected, only rising to 1688k (cons 1690k) from 1679k, holding below the 2019 average.

- US AUG FINAL DEMAND PPI +0.7%, EX FOOD, ENERGY +0.2%

- US AUG FINAL DEMAND PPI EX FOOD, ENERGY, TRADE SERVICES +0.3%

- US AUG FINAL DEMAND PPI Y/Y +1.6%, EX FOOD, ENERGY Y/Y +2.2%

- US AUG PPI: FOOD -0.5%; ENERGY +10.5%

- US AUG PPI: GOODS +2.0%; SERVICES +0.2%; TRADE SERVICES -0.3%

- In-line PPI final demand ex food & energy: 0.19% M/M (cons 0.2) in Aug after an upward revised 0.37% M/M (initial 0.31%) in July, but with downward revisions to the prior two months.

- Clearly stronger than expected PPI final demand ex food, energy & trade: 0.34% M/M (cons 0.2) after a strong upward revised 0.32% M/M initial 0.2) in July and less so 0.16% (initial 0.13) in June .

- The latter sees a strong beat for final demand ex food, energy & trade when looking in Y/Y terms, surprisingly accelerating to 3.0% Y/Y (cons 2.7) from 2.7%.

- See charts below for latest trends vs pre-revisions.

- US AUG RETAIL SALES +0.6%; EX-MOTOR VEH +0.6%

- US JUL RETAIL SALES REVISED +0.5%; EX-MV +0.7%

- US AUG RET SALES EX GAS & MTR VEH & PARTS DEALERS +0.2% V JUL +0.7%

- US AUG RET SALES EX MTR VEH & PARTS DEALERS +0.6% V US AUG +0.7%

- US AUG RET SALES EX AUTO, BLDG MATL & GAS +0.1% V JUL +0.8%

- US AUG RETAIL SALES CONTROL GROUP +0.1% V JUL +0.7%

- US JUL BUSINESS INVENTORIES +0.0%; SALES +0.6%

- US JUL RETAIL INVENTORIES +0.2%

- CANADA JUL WHOLESALE SALES +5.3%; EX-AUTOS -0.5%

- JUL WHOLESALE INVENTORIES +1.3%: STATISTICS CANADA

MARKETS SNAPSHOT

Key late session market levels:- DJIA up 385.53 points (1.12%) at 34962.26

- S&P E-Mini Future up 42.75 points (0.95%) at 4560.25

- Nasdaq up 140.7 points (1%) at 13953.78

- US 10-Yr yield is up 4 bps at 4.2883%

- US Dec 10-Yr futures are down 8.5/32 at 109-24

- EURUSD down 0.0093 (-0.87%) at 1.0637

- USDJPY down 0.02 (-0.01%) at 147.45

- WTI Crude Oil (front-month) up $1.74 (1.97%) at $90.27

- Gold is up $0.62 (0.03%) at $1908.73

- EuroStoxx 50 up 56.27 points (1.33%) at 4279.75

- FTSE 100 up 147.09 points (1.95%) at 7673.08

- German DAX up 151.26 points (0.97%) at 15805.29

- French CAC 40 up 86.1 points (1.19%) at 7308.67

US TREASURY FUTURES CLOSE

- 3M10Y +6.674, -118.025 (L: -128.253 / H: -117.428)

- 2Y10Y -0.244, -72.742 (L: -76.154 / H: -70.81)

- 2Y30Y -0.257, -63.264 (L: -67.111 / H: -59.885)

- 5Y30Y +0.425, -3.761 (L: -7.071 / H: -0.16)

- Current futures levels:

- Dec 2-Yr futures down 2.125/32 at 101-17.375 (L: 101-16.25 / H: 101-21.625)

- Dec 5-Yr futures down 4/32 at 106-3.75 (L: 106-01.5 / H: 106-13.25)

- Dec 10-Yr futures down 8.5/32 at 109-24 (L: 109-22.5 / H: 110-07.5)

- Dec 30-Yr futures down 20/32 at 119-1 (L: 118-28 / H: 120-00)

- Dec Ultra futures down 35/32 at 125-19 (L: 125-11 / H: 127-00)

US 10Y FUTURE TECHS: (Z3) Bullish Hammer Candle Formation

- RES 4: 112-24+ High Jul 27

- RES 3: 112-14 High Aug 10

- RES 2: 112-00 Round number resistance

- RES 1: 110-09 /111-12+ 20-day EMA / High Sep 1 key resistance

- PRICE: 109-23+ @ 1450 ET Sep 14

- SUP 1: 109-03 Low Sep 13

- SUP 2: 109-00 Round number support

- SUP 3: 108-20 1.000 proj of the Jul 18 - Aug 4 - Aug 10 price swing

- SUP 4: 107.23 1.236 proj of the Jul 18 - Aug 4 - Aug 10 price swing

The trend direction in Treasuries remains down and yesterday’s low print of 109-03 reinforces the bearish theme and signals a resumption of the downtrend. However, the recovery from yesterday’s low is a short-term bullish development. The strong daily close highlights a hammer candle formation - a reversal signal. If correct, yesterday’s price action suggests scope for a correction near-term. First resistance to watch is 110-09, the 20-day EMA.

SOFR FUTURES CLOSE

- Sep 23 +0.010 at 94.60

- Dec 23 +0.005 at 94.550

- Mar 24 -0.010 at 94.670

- Jun 24 -0.030 at 94.905

- Red Pack (Sep 24-Jun 25) -0.055 to -0.045

- Green Pack (Sep 25-Jun 26) -0.04 to -0.03

- Blue Pack (Sep 26-Jun 27) -0.035 to -0.03

- Gold Pack (Sep 27-Jun 28) -0.05 to -0.035

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00163 to 5.33057 (+0.00111/wk)

- 3M +0.00066 to 5.41009 (-0.00038/wk)

- 6M +0.00417 to 5.47767 (+0.00570/wk)

- 12M +0.00501 to 5.43665 (+0.01273/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $104B

- Daily Overnight Bank Funding Rate: 5.32% volume: $264B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.385T

- Broad General Collateral Rate (BGCR): 5.30%, $570B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $556B

- (rate, volume levels reflect prior session)

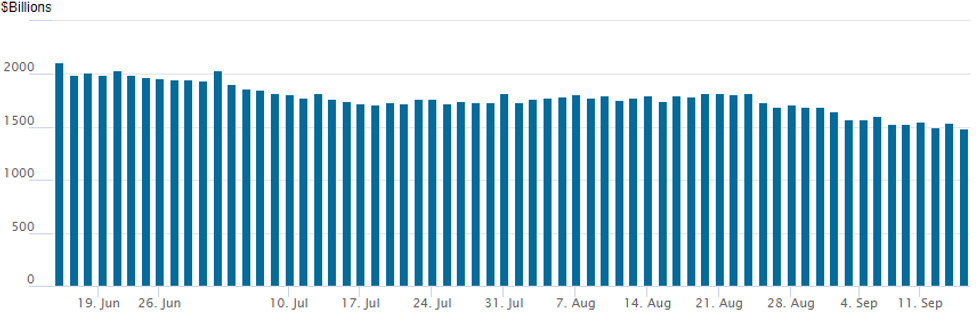

FED REVERSE REPO OPERATION: Back to Extending Lows

NY Federal Reserve/MNI

Repo operation falls back new lowest level since early March 2022: 1,492.427B w/97 counterparties, compared to $1,546.225B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE: $2.75B To Price THursday

- Date $MM Issuer (Priced *, Launch #)

- 09/14 $1.25B #Bangkok Bank $500M 5Y +125a, $750M 10Y +150a

- 09/14 $1B Energy Development Oman 10Y +190a

- 09/14 $500M #Corebridge 5Y +150

EGBs-GILTS CASH CLOSE: Belly Outperformance On Dovish ECB Hike

European yields fell Thursday, with curve bellies outperforming as the ECB was seen to have delivered a dovish hike.

- While the ECB's decision to hike its policy rates by 25bp was not fully priced (around 70% probability implied beforehand), leading to a knee-jerk jump in yields, a reversal swiftly followed.

- The accompanying statement implied that the Governing Council saw this as the last hike in the cycle ("rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to the target").

- The 2Y and 30Y segments lagged the rally across both the German and UK curves, with the policy-rate sensitive belly of the curve noticeably outperforming as European central banks are increasingly seen nearing the end of tightening.

- Periphery spreads fell sharply after the decision, helped by Lagarde brushing off talk of curtailing PEPP.

- Friday morning sees some final Aug inflation data and the Euro labour force survey, along with appearances by ECB's Villeroy and Lagarde.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.4bps at 3.166%, 5-Yr is down 6.2bps at 2.62%, 10-Yr is down 5.8bps at 2.593%, and 30-Yr is down 2.6bps at 2.727%.

- UK: The 2-Yr yield is down 3.5bps at 4.95%, 5-Yr is down 8.4bps at 4.481%, 10-Yr is down 6.6bps at 4.281%, and 30-Yr is down 5.6bps at 4.608%.

- Italian BTP spread down 4.9bps at 174.7bps / Spanish bond spread down 2.3bps at 104.8bps

FOREX Post-ECB Euro Weakness Extends, EURUSD Prints Six-Month Low

- Despite a very brief spike on the moderately surprising 25bp hike from the ECB, downgrades to Eurozone growth forecasts and a potentially dovish signal on rate guidance has prompted some significant weakness for the single currency on Thursday.

- Since the decision and President Lagarde’s press conference, any upticks for the single currency have been met with solid supply. EURUSD has continued to edge lower over the course of the US session, extending intra-day lows and most recently piercing a key support level from earlier this year.

- The May 31 low at 1.0635 has represented the key short-term support and a sustained breach will solidify the current downtrend in place. Below here we have 1.0611, the 38.2% Fibonacci retracement Sep’22 - Jul’23 upleg, before 1.0516 the Mar 15 low and a key medium-term support.

- EURJPY has now crossed below its 50-day EMA at 156.95 but more notably, the likes of EURAUD, EURCAD have extended losses to over 1%, as the more optimistic tone for equity markets adds particular weight to Euro crosses.

- Elsewhere, the USD index is rising 0.58% on the back of better-than-expected US August retail sales data, leaving little to support a bearish near-term US growth view. Higher US PPI figures are also underpinning the greenback resilience.

- In response, the trend needle in GBPUSD (-0.70%) continues to point south and the pair has traded to a fresh cycle low today, a few pips below the 124.00 handle. This confirms a resumption of the downtrend and maintains the bearish price sequence of lower lows and lower highs.

- Chinese industrial production and retail sales overnight will be the next important release for global risk sentiment. For the Eurozone, final French CPI and Italian trade balance data headline a relatively quiet regional docket. On the US side, empire state manufacturing, industrial production and UMich sentiment data will be released. ECB president Lagarde is also scheduled to speak again, due to hold a press conference at the Eurogroup meeting, in Spain.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/09/2023 | 0200/1000 | *** |  | CN | Fixed-Asset Investment |

| 15/09/2023 | 0200/1000 | *** | | CN | Retail Sales |

| 15/09/2023 | 0200/1000 | *** | | CN | Industrial Output |

| 15/09/2023 | 0200/1000 | ** | | CN | Surveyed Unemployment Rate M/M |

| 15/09/2023 | 0645/0845 | *** |  | FR | HICP (f) |

| 15/09/2023 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 15/09/2023 | 0830/0930 | ** |  | UK | Bank of England/Ipsos Inflation Attitudes Survey |

| 15/09/2023 | 0900/1100 | * |  | EU | Trade Balance |

| 15/09/2023 | 0900/1100 | | EU | Labour Force Survey (Q2) | |

| 15/09/2023 | 0945/1145 | | EU | ECB's Lagarde & Panetta speak in Spain | |

| 15/09/2023 | 1230/0830 | * |  | CA | International Canadian Transaction in Securities |

| 15/09/2023 | 1230/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 15/09/2023 | 1230/0830 | ** |  | US | Import/Export Price Index |

| 15/09/2023 | 1230/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/09/2023 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 15/09/2023 | 1315/0915 | *** | | US | Industrial Production |

| 15/09/2023 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 15/09/2023 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.