Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: Fed Holds Rates Steady But Points To Likely Future Hikes

- MNI US Inflation Insight, Jun'23: Core CPI Accelerates But Some Better Details

- MNI US DATA: PPI Adds To Non-Used Car Core Goods Disinflation Case

- MNI INTERVIEW:ECB Dilemma As German Inflation Outruns Eurozone

- MNI BRIEF: BOE To Formally Review Its Forecasting Processes

US

FED: The Federal Reserve kept interest rates on hold Wednesday for the first time since March of last year as it tries to gauge the full effect of its aggressive hiking campaign on the economy and credit conditions, but officials suggested more rises to come as they boosted their forecasts for where borrowing costs will peak.

- FOMC members raised their projections for where the federal funds rate will end the cycle to a median 5.6% from 5.1% at the March meeting, implying at least two more quarter-point hikes may be forthcoming this year.

- "Holding the target range steady at this meeting allows the committee to assess additional information and its implications for monetary policy," the FOMC said after leaving official rates in a target range of 5%-5.25%, the highest level in 15 years. The FOMC repeated that it would take policy lags into account in determining the “extent of additional policy firming.”

- The Fed is now at its most divided since it started raising rates in March 2022, with some officials arguing further tightening is needed in the face of stubborn inflation, while others, more keenly focused on the traditional lag time of monetary policy effects on growth and inflation, would prefer to take a breather on rate increases for now. Two of 18 officials would prefer no further changes in rates this year. Still, the decision to hold rates for now was unanimous. For more see MNI Policy main wire at 1400ET.

US: MNI US Inflation Insight, Jun'23: Core CPI Accelerates But Some Better Details. Core CPI inflation was modestly stronger than expected in May as it increased 0.44% M/M vs a consensus average of 0.36%, but the surprise was heavily driven by another strong increase in used car prices.

- Underlying figures generally continued to show signs of some moderation, with confirmation of April’s softer supercore service inflation and core goods prices ex used vehicles flat on the month.

- Core PCE estimates currently track little progress from April though, perhaps just 1-2 hundredths below April’s 0.38% M/M (post-PPI tweaks aside).

EUROPE

ECB: Inflation in Germany is set to remain higher than in other core eurozone countries for some time, raising the risk that the European Central Bank could push rates to levels which are too tight for other parts of the bloc, Markus Demary, senior monetary policy and financial markets economist at the German Economic Institute (IW), told MNI.

- The ECB could continue hiking into 2024, possibly increasing rates once or twice more in the first half of next year, Demary said. Market pricing currently implies the ECB will hike by another 50 basis points to a peak of 3.75% around October, before cuts become more likely next year

- “We are not going back to a low inflation environment,” Demary said. “We are back in the old world with inflation slightly above the ECB’s inflation target, with monetary policy leaning against upwards price pressures with further increases in interest rates.” For more see MNI Policy main wire at 0819ET.

UK

BOE: The Bank of England has decided to undertake a review of its forecasting processing, the head of the Court of Directors said in a letter to the Treasury Select Committee Wednesday, with the cross-party group of legislators also requesting that it do so.

- The Court -- the central bank's overall governing body -- said, in response to a letter this week from the TSC, that it had discussed back at its May meeting learning the lessons of recent events and forecasting at a time of high uncertainty. The BOE's central projections failed to predict the extent or persistence of the rise in inflation and it has been publishing a large upward skew to its inflation, based on judgement and alternative analysis, to better reflect its views on inflation. (See MNI POLICY: BOE Hikes Whilst Seeking New Inflation Model).

- David Roberts, the Court's head said that he and Governor Andrew Bailey were working on how best to commission the review and decide on its terms of reference and that it would be supported by the Independent Evaluation Office, with the process set to be transparent.

US TSYS: Late Markets Roundup: July is Live

- Treasury futures are holding firmer for the most part, just off pre-FOMC levels with the short end underperforming after the Fed kept rates steady, as expected. But hawkish forward guidance with 12 of 18 Fed officials expecting another 50bp later this year saw futures gap lower. Chairman Powell: July is Live.

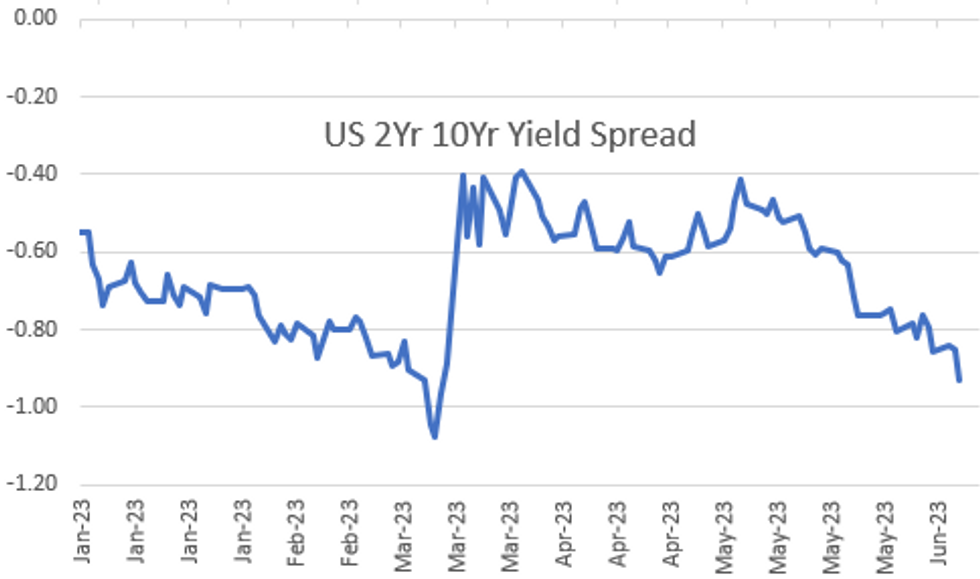

- The unexpected guidance weighed heavily on the short end, curves flattening sharply (2s10s fell to -95.800, lowest since March 10s when the spread inverted to the lowest level since the early 80s.

- The decision comes against the backdrop of an inflation picture that has been improving but is still a far cry from the central bank's official 2% target. CPI inflation slipped to a two-year low of 4.0% in May but core inflation remained quite elevated at 5.3%.

- Treasury futures extended highs this morning after lower than expected PPI (-0.3% vs. -0.1% est; YoY flat vs +1.5% est).

- STIR: July hike: +16bp having sat at +18.5bp after the announcement, back at the +16bp cumulative pre-decision. Terminal: 5.29% in Sep (and 5.28% in Nov), vs 5.32% held after announcement vs 5.25% pre-decision

- Cuts from terminal to year-end: near unchanged on presser, currently at 8bps vs 15bps pre-decision for a rate that’s 13bps higher than the current effective of 5.08%.

OVERNIGHT DATA

- US MAY FINAL DEMAND PPI -0.3%, EX FOOD, ENERGY +0.2%

- US MAY FINAL DEMAND PPI EX FOOD, ENERGY, TRADE SERVICES +0.0%

- US MAY FINAL DEMAND PPI Y/Y +1.1%, EX FOOD, ENERGY Y/Y +2.8%

- US MAY PPI: FOOD -1.3%; ENERGY -6.8%

US DATA: PPI inflation was generally softer than expected in May, with total final demand -0.3% M/M (cons -0.1%) after +0.2%, ex food, energy & trade seeing a notable miss but ex food & energy mostly in line.

- On that ex food, energy & trade miss, it came in at -0.04% M/M in May vs consensus 0.2%. Revisions were mixed on net but leave weaker momentum, with downward in April to 0.11% (initial 0.18%) but upward to 0.18% in March (initial 0.12%), and a 3-month annualized increase of 1%.

- The latest dip into deflation tallies well with yesterday’s CPI core goods ex used vehicles at 0.00% M/M after an equally tepid 0.04% M/M back in April. Continued sizeable improvements in supply chain pressures suggest potentially further moderation ahead.

- US MBA: MARKET COMPOSITE +7.2% SA THRU JUN 09 WK

- US MBA: REFIS +6% SA; PURCH INDEX +8% SA THRU JUNE 9 WK

- US MBA: UNADJ PURCHASE INDEX -27% VS YEAR-EARLIER LEVEL

- US MBA: 30-YR CONFORMING MORTGAGE RATE 6.77% VS 6.81% PREV

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 216.17 points (-0.63%) at 33994.42

- S&P E-Mini Future up 1.25 points (0.03%) at 4417.5

- Nasdaq up 31.8 points (0.2%) at 13604.33

- US 10-Yr yield is down 0.6 bps at 3.8075%

- US Sep 10-Yr futures are up 2.5/32 at 112-24

- EURUSD up 0.0036 (0.33%) at 1.0829

- USDJPY down 0.36 (-0.26%) at 139.86

- WTI Crude Oil (front-month) down $0.81 (-1.17%) at $68.58

- Gold is up $2.17 (0.11%) at $1945.81

- EuroStoxx 50 up 28.43 points (0.65%) at 4375.98

- FTSE 100 up 7.96 points (0.1%) at 7602.74

- German DAX up 80.11 points (0.49%) at 16310.79

- French CAC 40 up 37.73 points (0.52%) at 7328.53

US TSY FUTURES CLOSE

- 3M10Y -2.587, -145.039 (L: -151.619 / H: -142.765)

- 2Y10Y -6.989, -92.706 (L: -95.8 / H: -82.549)

- 2Y30Y -10.096, -85.144 (L: -89.738 / H: -70.192)

- 5Y30Y -7.687, -15.021 (L: -18.944 / H: -3.543)

- Current futures levels:

- Sep 2-Yr futures down 2.875/32 at 102-3.625 (L: 101-31.375 / H: 102-12.375)

- Sep 5-Yr futures down 3.5/32 at 107-20.25 (L: 107-12.25 / H: 108-04.5)

- Sep 10-Yr futures up 2.5/32 at 112-24 (L: 112-12.5 / H: 113-05.5)

- Sep 30-Yr futures up 20/32 at 126-28 (L: 126-07 / H: 127-06)

- Sep Ultra futures up 1-08/32 at 135-31 (L: 134-25 / H: 136-10)

US 10YR FUTURE TECHS: (U3) Resumes Its Downtrend

- RES 4: 115-19 High May 18

- RES 3: 115-00 High Jun 1 and a key resistance

- RES 2: 114-06+ / 114-23 High Jun 6 / 50-day EMA

- RES 1: 114-00 High Jun 13

- PRICE: 113-02+ @ 16:31 BST Jun 14

- SUP 1: 112-20+ Low Jun 13

- SUP 2: 112-16 76.4% retracement of the Mar 2 - May 4 rally

- SUP 3: 112-00 Low Mar 10

- SUP 4: 111-14+ Low Mar 9

Treasury futures remain in a downtrend and the Tuesday sell-off confirmed a resumption of the downtrend. Support at 112-29+, the May 26 / 30 lows have been cleared and the contract is trading just above its recent low. The focus is on 112-16, a Fibonacci retracement, where a break would open the 112-00 handle, the Mar 10 low. On the upside, initial firm resistance is seen at 114-00, Tuesday’s high.

SOFR FUTURES CLOSE

- Jun 23 +0.020 at 94.80

- Sep 23 -0.020 at 94.710

- Dec 23 -0.070 at 94.795

- Mar 24 -0.080 at 95.10

- Red Pack (Jun 24-Mar 25) -0.06 to -0.03

- Green Pack (Jun 25-Mar 26) -0.025 to -0.005

- Blue Pack (Jun 26-Mar 27) steadysteady0 to +0.020

- Gold Pack (Jun 27-Mar 28) +0.025 to +0.055

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.04511 to 5.10188 (-.03682/wk)

- 3M -0.03621 to 5.21811 (-.03127/wk)

- 6M -0.02769 to 5.26695 (-.01916/wk)

- 12M -0.00589 to 5.15284 (+.00467/wk)

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00343 to 5.06543%

- 1M -0.03515 to 5.15814%

- 3M -0.04357 to 5.50843 */**

- 6M +0.00100 to 5.65143%

- 12M +0.01543 to 5.81886%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.54443% on 6/9/23

- Daily Effective Fed Funds Rate: 5.08% volume: $131B

- Daily Overnight Bank Funding Rate: 5.06% volume: $291B

- Secured Overnight Financing Rate (SOFR): 5.05%, $1.375T

- Broad General Collateral Rate (BGCR): 5.03%, $620B

- Tri-Party General Collateral Rate (TGCR): 5.03%, $611B

- (rate, volume levels reflect prior session)

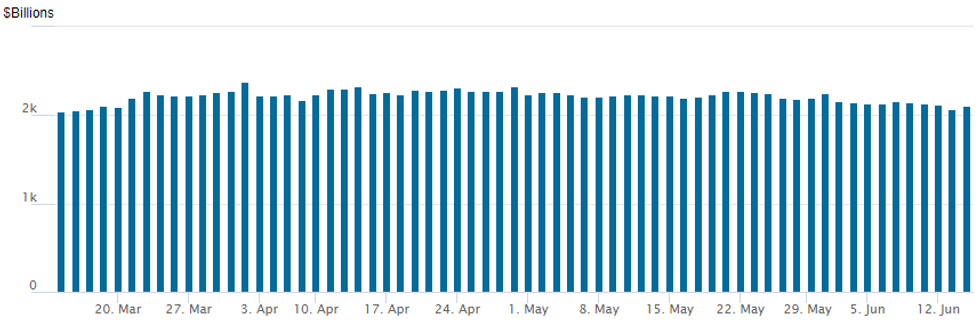

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage rebounds to $2,109.105B w/ 106 counterparties, compared to $2,074.520B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE: High-Grade Corporate Issuance Sidelined Ahead FOMC

- Date $MM Issuer (Priced *, Launch #)

- 06/14 $Benchmark issuance on hold ahead FOMC, $7.6B Priced Mon-Tue

- $850M Priced Tuesday

- 06/13 $850M *Duke Energy $350M 2033 tap+130, $500M +30Y +150

- $6.75B Priced Monday

- 06/12 $2.75B *Intesa Sanpaolo $1.25B 10Y +290, $1.5B 31NC30 +390

- 06/12 $2B *HSBC 11NC10 +280

- 06/12 $1B *Cox Communications $500M +5Y +155, $500M 10Y +197

- 06/12 $500M *Aviation Capital Grp 7Y +273

- 06/12 $500M *Global Atlantic 10Y +450

EGBs-GILTS CASH CLOSE: Gilts Only Partially Recover

Tuesday's Gilt selloff partially reversed Wednesday as UK yields fell led by the short-end. The German curve bear flattened ahead of Thursday's ECB decision.

- UK yields traded with more directional (downward) impetus than German counterparts, which weakened on the day but lacked clear direction.

- Even with a 7bp decline in yields (UK Apr GDP was a little softer than expected), with a fairly strong last hour of trade, 2Y Gilts sit 18bp higher than Monday's open.

- Periphery spreads likewise gave back some of Tuesday's tightening vs Bunds. Greek spreads widened for the 3rd straight session following the lack of ratings action from Fitch last Friday.

- BoE terminal hike pricing pulled back 7bp on the day, with ECB +2bp.

- Attention turns to the Federal Reserve decision after hours (no change in rates expected), with the ECB waiting in the wings Thursday (to hike rates by 25bp and confirm previous decision to end APP reinvestments in July - our preview is here).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4.2bps at 3.016%, 5-Yr is up 3.2bps at 2.507%, 10-Yr is up 2.9bps at 2.452%, and 30-Yr is up 2bps at 2.584%.

- UK: The 2-Yr yield is down 7.5bps at 4.822%, 5-Yr is down 5.6bps at 4.472%, 10-Yr is down 4.2bps at 4.392%, and 30-Yr is down 5.6bps at 4.559%.

- Italian BTP spread up 0.4bps at 163.6bps / Greek up 2.9bps at 131.3bps

FOREX: Hawkish Fed Projections Unable To Curtail Overall Greenback Weakness

- The greenback weakened steadily throughout Wednesday in the lead up to the June FOMC decision. The sell-off had been exacerbated by the USD index breaching its 100-day moving average with initially buoyant global equity benchmarks underpinning the rally for other G10 currencies with particular outperformance amid high beta currencies such as AUD & NZD.

- A surprisingly hawkish set of Fed projections to accompany the unchanged decision on rates boosted the greenback and saw the USD index recover the majority of these losses in the immediate aftermath.

- However, with Chair Powell dismissing the ‘skip’ thesis and declaring that each meeting will be live going forward, the USD’s renewed support waned. As we approach the APAC crossover, the DXY sits around 0.25% lower on the session with antipodeans continuing to outperform.

- GBPUSD has also posted a 0.4% advance, extending on an impressive rally Tuesday. Cable did pierce a key resistance point at 1.2680, the May 10 high. The next objective for the rally comes in at 1.2759, the 61.8% retracement of the Jun - Sep bear leg.

- In emerging markets, local currencies have benefitted from the greenback weakness and the consolidation of strength for major equity benchmarks. ZAR and PLN were standout performers as well as MXN and BRL continuing their impressive recent runs higher.

- With the Fed out of the way, the central bank focus turns to Europe, with Thursday’s ECB meeting expecting rates to be increased by 25bps. On the data front, New Zealand GDP and Australia employment kick off the APAC docket, before China releases a host of production/activity data. US retail sales, Philly Fed and initial jobless claims will also hit the wires.

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/06/2023 | 2350/0850 | ** |  | JP | Trade |

| 15/06/2023 | 0130/1130 | *** |  | AU | Labor Force Survey |

| 15/06/2023 | 0200/1000 | *** |  | CN | Fixed-Asset Investment |

| 15/06/2023 | 0200/1000 | *** | | CN | Retail Sales |

| 15/06/2023 | 0200/1000 | *** | | CN | Industrial Output |

| 15/06/2023 | 0200/1000 | ** | | CN | Surveyed Unemployment Rate |

| 15/06/2023 | 0645/0845 | *** |  | FR | HICP (f) |

| 15/06/2023 | 0900/1100 | * |  | EU | Trade Balance |

| 15/06/2023 | - | | EU | ECB Panetta at Eurogroup Meeting | |

| 15/06/2023 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 15/06/2023 | 1215/1415 | *** | | EU | ECB Deposit Rate |

| 15/06/2023 | 1215/1415 | *** | | EU | ECB Main Refi Rate |

| 15/06/2023 | 1215/1415 | *** | | EU | ECB Marginal Lending Rate |

| 15/06/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 15/06/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 15/06/2023 | 1230/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 15/06/2023 | 1230/0830 | *** | | US | Retail Sales |

| 15/06/2023 | 1230/0830 | ** | | US | Import/Export Price Index |

| 15/06/2023 | 1230/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/06/2023 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 15/06/2023 | 1245/1445 | | EU | Post-Meeting ECB Press Conference | |

| 15/06/2023 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 15/06/2023 | 1315/0915 | *** | | US | Industrial Production |

| 15/06/2023 | 1400/1000 | * | | US | Business Inventories |

| 15/06/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 15/06/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 15/06/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 15/06/2023 | 1535/1635 |  | UK | BOE Cunliffe at Politico Global Tech Summit | |

| 15/06/2023 | 2000/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.