Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

MNI: FOMC Cautious On Cuts, To Start QT Taper Debate in March

MNI INTERVIEW: Rising Rents Shouldn't Defer BOE Rate Cuts

MNI BRIEF: Overtightening Would Risk Scarring - BOE's Dhingra

US

US FED (MNI): FOMC Cautious On Cuts, To Start QT Taper Debate in March

- Most Federal Reserve officials warned against the possibility of easing monetary policy too fast at their January meeting, while also deciding they will debate a slowing in the pace of asset runoffs at their March meeting, minutes published Wednesday showed.

- Policymakers thought the risks to the Fed’s dual mandate of stable prices and maximum employment were becoming more balanced, but also remain cautious about the prospect of cutting interest rates, the minutes said.

NEWS

INTERVIEW (MNI): Rising Rents Shouldn't Defer BOE Rate Cuts

Elevated rental inflation poses a challenge to Bank of England communications as it approaches an easing cycle, but it should resist any temptation to delay cuts due to concerns over shelter costs, former senior New York Fed and BOE economist Gianluca Benigno told MNI.

BRIEF (MNI): Overtightening Would Risk Scarring - BOE's Dhingra

The restrictive stance of monetary policy will continue to weigh on economic growth and living standards, Bank of England external MPC member Swati Dhingra told an MNI Connect video conference, adding that overtightening would risk a hard landing and supply-side scarring.

POLAND (BBG): EU Set To Release Blocked Funds To Poland As Early As Next Week

The European Union is poised to release €6.3 billion ($6.8 billion) in post-pandemic aid to Poland as early as next week in a major vote of confidence in the new government’s ability to mend ties with Brussels. The European Commission is set to accept a package of recent political commitments as sufficient to trigger the first payment from almost €60 billion in grants and loans that have remained blocked over rule-of-law concerns, according to people familiar with the discussions who spoke on condition of anonymity.

NATO (MNI): Bipartisan US Senators Prepare Resolution Condemning Hungary

Senators Jeanne Shaheen (D-NH) and Thom Tilis (R-NC), the joint chairs of the Senate’s NATO Observer Group, are preparing to unveil a Senate resolutioncondemning Hungary for a variety of reasons including democratic backsliding, curtailing media freedom, and a “deepening relationship with Russia and China.”

SECURITY (MNI): RTRS-'Iran Sends Russia Hundreds Of Ballistic Missiles'

Reuters reports that according to its sources, "Iran has provided Russia with a large number of powerful surface-to-surface ballistic missiles [...] deepening the military cooperation between the two U.S.-sanctioned countries."

US TSYS Markets Roundup: Measure Twice, Cut Once

- Treasury futures drifting near late session lows after briefly paring losses as markets digested the January FOMC minutes. Focus on policy maker concern of cutting rates too soon vs. waiting too long took precedent as rates clung near lows.

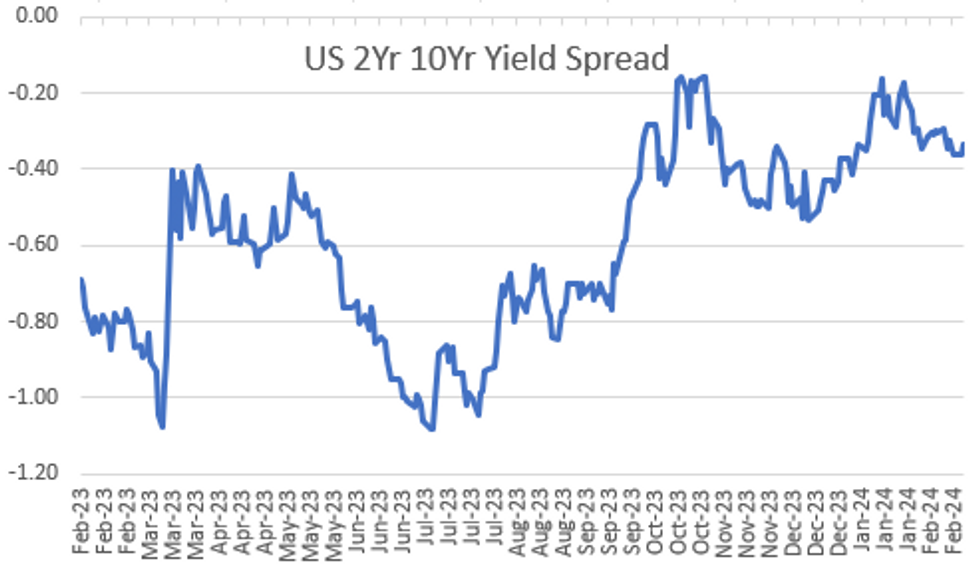

- Mar'24 10Y futures currently -8.5 at 109-21.5, vs 109-18 low; initial technical support of 109-17/16+ (50.0% of Oct 19 - Dec 27 climb / Low Feb 14) earlier to 109-15 low. Resistance above at 110-17.5 (Feb 15 high). Curves mildly flatter: 2s10s -0.163 at -34.063, 10Y yield +0.0394 at 4.3147%.

- Large flattener Block posted at 1032:32ET adding to dip in the short end to intermediates: -35,000 TUH4 102-01.38, post time offer, DV01 $1,337M vs. +14,500 UXYH4 113-25.5, buy through 113-23 post time offer, DV01 $1.328M.

- Projected rate cut pricing are consolidating from this morning's levels: March 2024 chance of 25bp rate cut currently -6.8% vs. -9.6% earlier w/ cumulative of -1.7bp at 5.312%; May 2024 at -26.6% vs. -30.0% w/ cumulative -8.3bp at 5.245%; June 2024 -60.5% vs. -64.9% w/ cumulative cut -23.5bp at 5.094%. Fed terminal at 5.33% in Feb'24.

- An hour prior to the minutes, Treasury futures gapped lower after $16B 20Y bond auction (912810TZ1) drew a large tail: 4.595% high yield vs. 4.562% WI; 2.39x bid-to-cover vs. prior month's 2.53x

- Limited reaction, if any to data (MBA Mtg Apps -10.6%) nor Fed speak. Boston Fed Collins fireside chat (no text, Q&A) later this evening at 0730ET.

- Corporate earnings after the close: Nvidia, Synopsys, Etsy, APA Corp, Rivian Automotive, Ansys Inc, Lucid, Marathon Oil.

OVERNIGHT DATA

- US MBA: REFIS -11% SA; PURCH INDEX -10% SA THRU FEB 16 WK

- US MBA: UNADJ PURCHASE INDEX -13% VS YEAR-EARLIER LEVEL

- US MBA: 30-YR CONFORMING MORTGAGE RATE 7.06% VS 6.87% PREV

- US MBA: MARKET COMPOSITE -10.6% SA THRU FEB 16 WK

- US REDBOOK: FEB STORE SALES +2.7% V YR AGO MO

- US REDBOOK: STORE SALES +3.0% WK ENDED FEB 17 V YR AGO WK

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 172.01 points (-0.45%) at 38389.97

- S&P E-Mini Future down 23.25 points (-0.47%) at 4967.25

- Nasdaq down 146.9 points (-0.9%) at 15480.85

- US 10-Yr yield is up 4.5 bps at 4.3206%

- US Mar 10-Yr futures are down 10/32 at 109-20

- EURUSD up 0.0008 (0.07%) at 1.0815

- USDJPY up 0.2 (0.13%) at 150.22

- Gold is up $1.02 (0.05%) at $2025.32

- European bourses closing levels:

- EuroStoxx 50 up 15.03 points (0.32%) at 4775.31

- FTSE 100 down 56.7 points (-0.73%) at 7662.51

- German DAX up 49.69 points (0.29%) at 17118.12

- French CAC 40 up 16.87 points (0.22%) at 7812.09

US TREASURY FUTURES CLOSE

- 3M10Y +1.775, -108.54 (L: -116.207 / H: -107.165)

- 2Y10Y +0.232, -33.668 (L: -35.64 / H: -31.606)

- 2Y30Y -0.105, -16.71 (L: -19.525 / H: -13.637)

- 5Y30Y -0.29, 19.102 (L: 16.608 / H: 21.422)

- Current futures levels:

- Mar 2-Yr futures down 2.5/32 at 101-30.75 (L: 101-30 / H: 102-03.125)

- Mar 5-Yr futures down 6.75/32 at 106-15 (L: 106-13.25 / H: 106-25.5)

- Mar 10-Yr futures down 9.5/32 at 109-20.5 (L: 109-18 / H: 110-04)

- Mar 30-Yr futures down 18/32 at 117-24 (L: 117-20 / H: 118-22)

- Mar Ultra futures down 27/32 at 123-15 (L: 123-10 / H: 124-22)

US 10Y FUTURE TECHS: (H4) Shallow Bounce, Bear Threat Remains

- RES 4: 112-00 Round number resistance

- RES 3: 111-21+ High Feb 5

- RES 2: 110-31+ 20-day EMA

- RES 1: 110-17+ High Feb 15

- PRICE: 109-26 @ 16:45 GMT Feb 21

- SUP 1: 109-17/15 50.0% of Oct 19 - Dec 27 climb / Low Feb 16

- SUP 2: 109-05+ Low Nov 28

- SUP 3: 108-19+ 61.8% of the Oct 19 - Dec 27 bull phase

- SUP 4: 108-14 Low Nov 15

Prices recovered slightly through the Tuesday London close and remain close to the week’s highs. Nonetheless, the shallow bounce does little to counter the over-arching bear threat in Treasuries. The break lower last week confirmed a resumption of the downleg that started Dec 27. The 110-00 handle has been cleared and sights are on 109-17, a pierced Fibonacci retracement that could prove key at the weekly close. A clear break would open 109-05+, the Nov 28 low. Initial firm resistance is at 110-25+, the 20-day EMA.

SOFR FUTURES CLOSE

- Mar 24 -0.010 at 94.703

- Jun 24 -0.030 at 94.940

- Sep 24 -0.035 at 95.255

- Dec 24 -0.045 at 95.570

- Red Pack (Mar 25-Dec 25) -0.055 to -0.055

- Green Pack (Mar 26-Dec 26) -0.05 to -0.045

- Blue Pack (Mar 27-Dec 27) -0.045 to -0.04

- Gold Pack (Mar 28-Dec 28) -0.04 to -0.04

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00075 to 5.32103 (+0.00518/wk)

- 3M -0.00381 to 5.32193 (+0.00791/Wk)

- 6M -0.02292 to 5.24349 (+0.01233/wk)

- 12M -0.05058 to 4.99891 (+0.02101/wk)

- Secured Overnight Financing Rate (SOFR): 5.30% (+0.00), volume: $1.610T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $673B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $664B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $104B

- Daily Overnight Bank Funding Rate: 5.31% (+0.00), volume: $280B

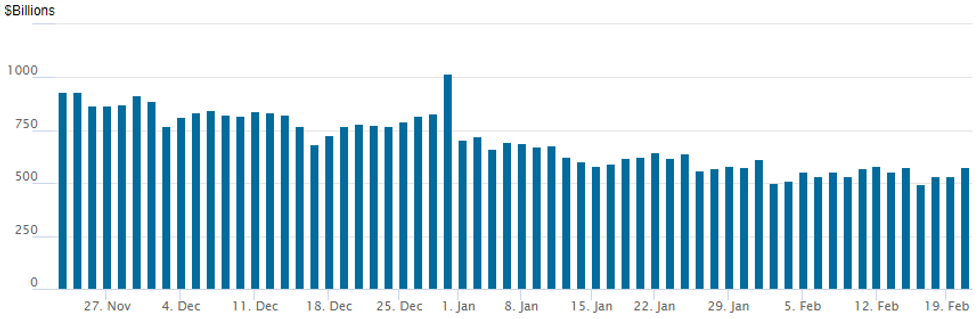

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

- RRP usage climbs to $574.882B vs. 530.879B Tuesday; compares to $493.065B on Thursday, Feb 15 -- the lowest since early June 2021 .

- Meanwhile, the latest number of counterparties climbs to 96 from 90 yesterday (compares to 65 on January 16, the lowest since July 7, 2021).

PIPELINE $13.5B Cisco Systems 7pt, $5B Astrazeneca 4Pt Debt Launched

- Date $MM Issuer (Priced *, Launch #)

- 2/21 $13.5B #Cisco Systems $1B 2Y +25, $2B 3Y +40, $2.5B 5Y +55, $2.5B 7Y +65, $.5B 10Y +75, $2B 30Y +85, $1B 40Y +95

- 2/21 $5B #Astrazeneca $1.25B 3Y +42, $1.25B 5Y +57, $1B 7Y +62, $1.5B 10Y +72

- 2/21 $2B Federal Rep of Germany (KFW) 10Y +51

- 2/21 $1.5B *NWB (Nederlandse Waterschapsbank) 5Y SOFR+46

- 2/21 $1.5B *Nordic Investment Bank (NIB) 5Y +37

- 2/21 $850M *First Abu Dhabi Bank 5Y +90

- 2/21 $500M #Inversiones CMPC 10Y +185

- 2/21 $Benchmark Abbvie investor calls, filed offer to fund Immunogen deal

- 2/21 $Benchmark Boston Scientific 5Y, 8Y investor calls

EGBs-GILTS CASH CLOSE: Afternoon Sell-Off Sees Curves Bear Flatten

European curves bear flattened Wednesday, with core instruments selling off toward the end of the session.

- Bunds and Gilts began the day on the back foot but had yields dipped by midday - all within prior session's ranges. But from midday London time through the cash close, yields rose steadily, with bear flattening evident as the 2Y segment underperformed.

- The short-end move came alongside a fairly sharp repricing out of rate cut expectations: 2024 ECB implied reductions were pared to 100bp from 108bp at midday; the BoE equivalent shifted to 67bp from 74bp.

- Alongside the more hawkish central bank repricing, periphery spreads closed wider to Bunds, reversing earlier tightening.

- The afternoon move couldn't be pinned on any particular development. BoE MPC's Dhingra maintaining a dovish outlook at an MNI event, and Eurozone flash consumer confidence data coming in exactly in line with expectations.

- While ECB's Wunsch noted in an interview that "it may be too early to get our hopes up" on inflation and rate cuts, those comments were not out of line with his previous views and were published well after the rate selloff had begun.

- Attention early Thursday will be on flash February PMIs.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 8bps at 2.854%, 5-Yr is up 8.1bps at 2.426%, 10-Yr is up 7.7bps at 2.45%, and 30-Yr is up 5.5bps at 2.59%.

- UK: The 2-Yr yield is up 7.7bps at 4.634%, 5-Yr is up 8bps at 4.143%, 10-Yr is up 6.2bps at 4.103%, and 30-Yr is up 4.3bps at 4.635%.

- Italian BTP spread up 1.3bps at 150bps / Spanish bond spread up 0.9bps at 91.8bps

FOREX Higher US Yields and FOMC Minutes Fail To Impact Greenback

- Despite the shift higher for US yields on Wednesday, the USD index has traded in a very narrow range. With treasuries extending lows following the latest 20-year auction tailing, the greenback traded moderately into the green ahead of the FOMC minutes, however, topside momentum failed to materialise.

- Moves this afternoon have been most noticeable through USDJPY, which improved its intra-day recovery to around 50 pips, closing in on yesterday’s highs located at 150.43. A brief uptick on the FOMC minutes quickly retraced, with the pair hovering around 150.20 ahead of the APAC crossover. USDJPY bulls will focus on 1.5089, the Feb 13 high, before 151.43, the November 16 high.

- Mixed performance across G10, with most ranges remaining contained. NZDUSD remains in positive territory and extends a noteworthy run of consecutive wins. Modest outperformance is likely thanks to strong demand at the latest long end NZGB syndication (which is usually dominated by offshore investors). NZDUSD saw support and rose closer to the 0.6200 mark, as well as tipping AUD/NZD toward the YTD lows of 1.0586.

- For emerging market FX, it is worth highlighting that one-month implied volatility for USDMXN sank to near 8.5%, the lowest level since mid 2021. Furthermore, one-month implied volatility on Brazilian real options has dipped to 9.2%, the lowest since 2014, potentially highlighting the reduced levels of embedded risk premium which reports suggest should particularly pop up on foreigners’ radar.

- Focus turns to Thursday’s release of European Flash PMIs, as well as final readings for Eurozone CPI. Canadian retail sales will also cross alongside US jobless claims. US Flash PMIs and existing home sales rounds off the docket.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/02/2024 | 0030/0930 | ** |  | JP | Jibun Bank Flash Japan PMI |

| 22/02/2024 | 0630/0630 |  | UK | BOE's Greene, Kroll South Africa breakfast | |

| 22/02/2024 | 0745/0845 | ** |  | FR | Manufacturing Sentiment |

| 22/02/2024 | 0815/0915 | ** | | FR | S&P Global Services PMI (p) |

| 22/02/2024 | 0815/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 22/02/2024 | 0830/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 22/02/2024 | 0830/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 22/02/2024 | 0900/1000 | ** |  | IT | Italy Final HICP |

| 22/02/2024 | 0900/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 22/02/2024 | 0900/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 22/02/2024 | 0900/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 22/02/2024 | 0930/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 22/02/2024 | 0930/0930 | *** | | UK | S&P Global Services PMI flash |

| 22/02/2024 | 0930/0930 | *** | | UK | S&P Global Composite PMI flash |

| 22/02/2024 | 1000/1100 | *** | | EU | HICP (f) |

| 22/02/2024 | 1100/0600 | *** |  | TR | Turkey Benchmark Rate |

| 22/02/2024 | 1330/0830 | *** |  | US | Jobless Claims |

| 22/02/2024 | 1330/0830 | ** |  | CA | Retail Trade |

| 22/02/2024 | 1445/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 22/02/2024 | 1445/0945 | *** | | US | S&P Global Services Index (flash) |

| 22/02/2024 | 1500/1000 | *** | | US | NAR existing home sales |

| 22/02/2024 | 1500/1000 | * | | US | Services Revenues |

| 22/02/2024 | 1500/1000 | | US | Fed Vice Chair Philip Jefferson | |

| 22/02/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 22/02/2024 | 1600/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 22/02/2024 | 1600/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 22/02/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 22/02/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 22/02/2024 | 1800/1300 | ** | | US | US Treasury Auction Result for TIPS 30 Year Bond |

| 22/02/2024 | 2015/1515 | | US | Philly Fed's Pat Harker | |

| 22/02/2024 | 2200/1700 | | US | Minneapolis Fed's Neel Kashkari | |

| 22/02/2024 | 2200/1700 | | US | Fed Governor Lisa Cook |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.