Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI INTERVIEW: FOMC In No Rush To Cut Rates- ExVC Kohn

- MNI BRIEF: Fed's Williams Says Rate Cuts Later This Year

- MNI US: Dep Treasury Secretary Adeyemo: "I Don't Expect The Government To Close"

- MNI Small Business Confidence Highest Since 2021

US

US FED INTERVIEW (MNI): FOMC In No Rush To Cut Rates- ExVC Kohn

Federal Reserve policymakers are in no hurry to begin reducing interest rates because they rightly fear recent disinflation could stall and see the first cut as the consequential start of a new easing cycle, former Fed Vice Chair Donald Kohn told MNI. “They don’t seem to be in any rush at all,” Kohn said in an interview. “Some of the disinflation could be temporary, one-off. They could envision a situation where inflation pressures didn’t abate and might have even gotten worse.”

FED BRIEF (MNI): Fed's Williams Says Rate Cuts Later This Year

New York Fed President John Williams said he expects the central bank to begin rate cuts likely later this year, and it is not his base case to tighten policy further, according to an interview published Friday. "At some point, I think it will be appropriate to pull back on restrictive monetary policy, likely later this year," said Williams, the vice chair of the FOMC, in an interview with Axios. "But it's really about reading that data and looking for consistent signs that inflation is not only coming down, but is moving towards that 2% longer-run goal."

NEWS

US (MNI): Dep Treasury Secretary Adeyemo: "I Don't Expect The Government To Close"

Deputy Treasury Secretary Wally Adeyemo, speaking at the Council of Foreign Relations on today's Russia sanction package, says he doesn't believe the government will shutdown next month.

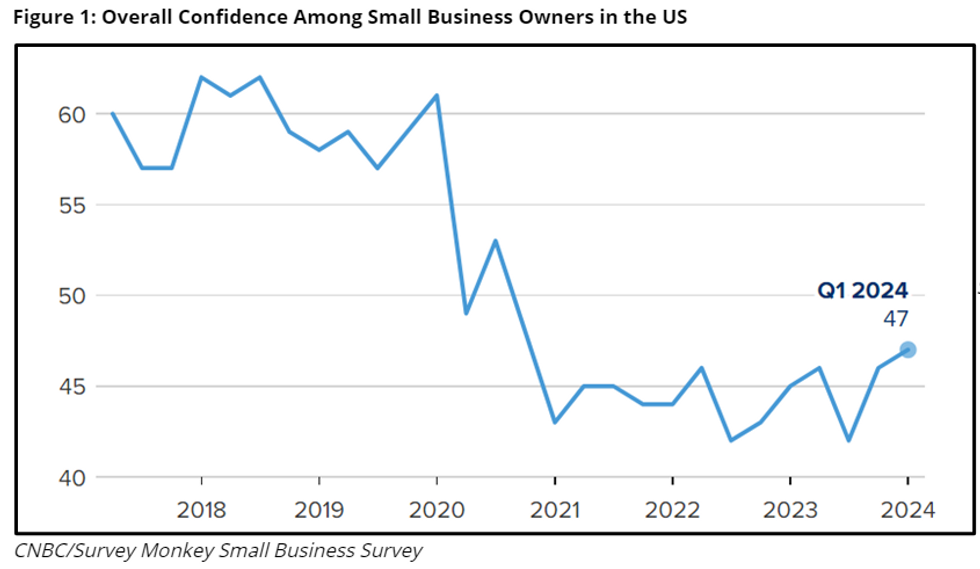

US (MNI): Small Business Confidence Highest Since 2021

Small business confidence is at the highest level since President Biden took office in 2021 according to the CNBC|SurveyMonkey Small Business Survey for Q1 2024. CNBC: “Even in the face of stubborn inflation, small business owners are striking a more positive tone… Twenty-eight percent of small business owners describe the current state of the economy as “excellent” or “good,” up five percentage points from the prior quarter and up from 18% year over year.”

US-RUSSIA (MNI): US Targets "Third-Country Sanctions Evaders"

The US Treasury Department has unveiled, "the largest number of sanctions imposed since Russia’s full-scale invasion of Ukraine," hitting over 500 targets in concert with the State Department, "to impose additional costs for Russia’s repression, human rights abuses, and aggression against Ukraine."

US-RUSSIA (MNI): New Sanctions To Target Russian Energy Revenue And Sanctions Evasion

The US will today unveil details of a new Russia sanctions package to mark the two-year anniversary of Russia's invasion of Ukraine and punish Moscow for the death of opposition figure Alexei Navalny.

SECURITY (MNI): US Takes Harder Line On Israeli Settlements, Sign Of Deepening Rift

In the past hour, US Secretary of State Antony Blinken, speaking in Argentina, and White House National Security Council Coordinator for Strategic Communications, John Kirby, briefing in Washington, have both told reporters that new Israeli settlements in the West Bank are "not consistent with international law."

ISRAEL (MNI): Paris Talks Set To Begin; FT Rpt-Israel To Seek Complete Gaza Control

The Times of Israel is reportingthat "The Israeli delegation to Paris for the high-level hostage talks departed Israel for France a short while ago[...] According to the reports, the delegation is headed by Mossad chief David Barnea and Shin Bet head Ronen Bar.

US TSYS Markets Roundup: Tsys Off Lows, Risk Unwinds Into Weekend

- Not much of a change since midday where Treasury futures climbed to session highs after a weaker open where Mar'24 10Y futures tapped the lowest level since late November '23.

- Treasury curves bull flattened (2s10s -4.271 at -43.590 -- Jan 3 low) on the bounce, no obvious headline driver, though trading desks widely citied a (modest) reversal in equities off contract highs as trading accounts took profits ahead the weekend.

- Mar'24 10Y futures had tested Thursday lows overnight (109-09) neared the 110 handle in late trade, climbing to 109-31 (+15), 10Y yield -.0629 at 4.25789%. Heavy volumes (TYH4>3.8M) tied to the roll to Jun'24 contract continues. Technical resistance above at 110-15.5 (20-day EMA).

- Projected rate cut pricing holds steady for the next couple meetings while June is off this morning's lows: March 2024 chance of 25bp rate cut currently -2.0% w/ cumulative of -0.5bp at 5.324%; May 2024 at -21.2% w/ cumulative -5.8bp at 5.271%; June 2024 -62.6% vs. -55.4% earlier w/ cumulative cut -21.4bp at 5.132%. Fed terminal at 5.33% in Feb'24.

- Look ahead: Next Monday sees New Home Sales (680k est vs 664k prior), MoM (2.4% est vs. 8.0% prior) at 1000ET, followed by Dallas Fed Mfg Activity Index at 1030ET. Flurry of Treasury auctions start Monday due to the short month: $63B 2Y note and $70B 26W bills at 1130ET, followed by $79B 13W bills and $64B 5Y Note auctions.

US TREASURY FUTURES CLOSE

- 3M10Y -8.071, -117.111 (L: -117.307 / H: -106.67)

- 2Y10Y -5.271, -44.59 (L: -44.59 / H: -38.848)

- 2Y30Y -6.573, -32.461 (L: -32.556 / H: -24.728)

- 5Y30Y -3.883, 8.861 (L: 8.563 / H: 13.565)

- Current futures levels:

- Mar 2-Yr futures up 1.125/32 at 101-28.25 (L: 101-24.5 / H: 101-29.375)

- Mar 5-Yr futures up 5.75/32 at 106-15.25 (L: 106-04 / H: 106-17.25)

- Mar 10-Yr futures up 12/32 at 109-28 (L: 109-09 / H: 109-31)

- Mar 30-Yr futures up 32/32 at 119-2 (L: 117-25 / H: 119-08)

- Mar Ultra futures up 55/32 at 125-26 (L: 123-24 / H: 126-04)

US 10Y FUTURE TECHS: (H4) Shallow Bounce, Bear Threat Remains

- RES 4: 112-00 Round number resistance

- RES 3: 111-21+ High Feb 5

- RES 2: 110-17+ High Feb 15

- RES 1: 110-15+ 20-day EMA

- PRICE: 109-28+ @ 16:40 GMT Feb 23

- SUP 1: 109-10 Low Feb 22

- SUP 2: 109-05+ Low Nov 28

- SUP 3: 108-19+ 61.8% of the Oct 19 - Dec 27 bull phase

- SUP 4: 108-14 Low Nov 15

Solid PMI data and a surge in US equities worked against Treasury prices Thursday, pressing Treasuries to 109-10, a new YTD low. The latest downleg affirms a resumption of the downtrend posted off the early February high, opening losses toward the late November lows of 109-05+. The 110-00 handle has been solidly cleared, with 109-17 support giving way into the Thursday close. Initial firm resistance remains at 110-15+, the 20-day EMA.

SOFR FUTURES CLOSE

- Mar 24 -0.010 at 94.688

- Jun 24 steady00 at 94.90

- Sep 24 +0.010 at 95.195

- Dec 24 +0.015 at 95.510

- Red Pack (Mar 25-Dec 25) +0.025 to +0.035

- Green Pack (Mar 26-Dec 26) +0.040 to +0.065

- Blue Pack (Mar 27-Dec 27) +0.070 to +0.080

- Gold Pack (Mar 28-Dec 28) +0.080 to +0.090

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00320 to 5.32413 (+0.00828/wk)

- 3M +0.00674 to 5.33057 (+0.01655/Wk)

- 6M +0.02078 to 5.27351 (+0.04235/wk)

- 12M +0.04738 to 5.07243 (+0.09453/wk)

- Secured Overnight Financing Rate (SOFR): 5.30% (+0.00), volume: $1.620T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $665B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $658B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $103B

- Daily Overnight Bank Funding Rate: 5.32% (+0.01), volume: $277B

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

- RRP usage recedes to $520.107B vs. 553.245B Thursday; compares to $493.065B on Thursday, Feb 15 -- the lowest since early June 2021 .

- Meanwhile, the latest number of counterparties falls back to 79 from 86 yesterday (compares to 65 on January 16, the lowest since July 7, 2021).

PIPELINE $6.9B Solventum Corp 6Pt Debt Launched; Total Month Supply $186.95B

Surprise $6.9B 6pt debt issuance from Solventum Corporation helps push total high grade corporate issuance for the week to $73.15B -- while total for the month rises to $186.95B - nearly matching February 2023 total issuance of $186.7B.

- Date $MM Issuer (Priced *, Launch #)

- 2/23 $6.9B #Solventum Corporation $1B 3Y +100, $1.5B 5Y +115, $1B 7Y +120, $1.65B 10Y +135, $1.25B 30Y +155, $500M 40Y +165

- 2/23 $Benchmark Potomac Electric Power investor calls

- 2/23 $Benchmark KeyCorp investor calls

$27.75B Priced Thursday - driven in large part by Abbvie's $15B 7pt on Thursday and Cisco's $13.5B 7pt issuance on Wednesday:

- 2/22 $15B *Abbvie** $2.25B 3Y +35, $2.5B 5Y +50, $2B 7Y +60, $3B 10Y +75, $750M 20Y +75, $3B 30Y +95, $1.5B 40Y +105

- 2/22 $3.1B *Panama $1.1B 7Y 7.5%, $1.25B 13Y 8%, $750M 33Y 8.25%

- 2/22 $2B *Caterpillar $800M 2Y +35, $600M 2Y SOFR+46, $600M 5Y +55

- 2/22 $2B *Federal Rep of Germany (KFW) 10Y +51

- 2/22 $2B *BNG Bank 3Y SOFR +32

- 2/22 $1.7B *Exelon $650M 5Y +87.5, $650M 10Y +115, $400M 29Y +130

- 2/22 $1.25B *Royal Caribbean 8NC3 6.25%

- 2/22 $700M *Northern States WNG 30Y +97

- **Abbvie held investor calls Wednesday after filing funding offer to fund Immunogen deal.

EGBs-GILTS CASH CLOSE: BTPs Shine As Week Ends On Stronger Note

European yields pulled back Friday, partially reversing rises earlier in the week, though the recent German curve flattening trend remained intact.

- The German and UK curves bull flattened (after twist flattening Thursday and bear flattening Wednesday), amid a rebound in ECB / BoE cut pricing from recent extremes. An in-line German IFO reading and modest uptick in Eurozone consumer 1-year inflation expectations had little impact.

- As with many intraday moves this week, afternoon price action had no evident catalyst, with a rally extending into the cash close as equities pulled back from recent highs.

- The rate move defied a parade of ECB speakers who appeared to push back on near-term cut pricing in coordinated fashion. That included the typical hawks (eg Holzmann, Muller, Nagel), but the doves too (though Centeno said the ECB must be open to a March cut even if unlikely, Stournaras and Simkus ruled one out, eyeing summer as more likely).

- Periphery EGBs impressed, with 10Y Italian spreads to Germany moving to the tightest levels since 2022 amid the ongoing risk rally.

- Germany 2s10s finished the week nearly 9bp flatter (flattest close since Dec 27), while the UK equivalent was around 0.5bp flatter.

- Next week will be busy, with the main highlight being the February flash round of Eurozone inflation.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 5.2bps at 2.853%, 5-Yr is down 7.5bps at 2.373%, 10-Yr is down 7.7bps at 2.363%, and 30-Yr is down 6.4bps at 2.493%.

- UK: The 2-Yr yield is down 6bps at 4.542%, 5-Yr is down 6.5bps at 4.088%, 10-Yr is down 6.8bps at 4.037%, and 30-Yr is down 4.4bps at 4.586%.

- Italian BTP spread down 3.8bps at 143.7bps / Spanish down 1.6bps at 88.9bps

FOREX USD Index Steps Lower On The Week Amid Optimism For Equities

- Surging equities this week weighed on the greenback overall with the USD index down -0.37%. However, the moderate downward adjustment was capped by a further uptick for front-end US yields as Fed officials continue to strike caution on premature monetary easing.

- Friday’s price action was mixed across G10 currencies, with major pairs making very limited adjustments amid a session void of meaningful data releases. Overall, NZD remains one of the best performers on the week, underpinned by the more optimistic risk backdrop.

- NZDUSD now stands around 2.6% above the February lows, with the pair set to close at its best level since mid-January and AUDNZD set to close below 1.06, levels not seen since May last year. Moves come ahead of the RBNZ decision next week, where MNI expect the RBNZ to leave rates on hold at 5.5%, even though the labour market data were stronger than expected.

- While USDJPY was unable to make a test of last week’s highs, price action this week has seen a consolidation above the 150.00 mark as cautious Fed remarks maintain the attractive carry profile.

- Recent fresh cycle highs confirm, once again, a resumption of the uptrend and note that last Tuesday’s gains resulted in a break of 149.75, the Nov 22 high. This signals scope for a climb towards 151.91/95, the Nov 13 ‘23 high and the Oct 1 ‘22 high and major resistance.

- Next week, the focus will be on the US January PCE deflator (out Thursday), which will be the last reading of the Fed's preferred inflation gauge before the March FOMC meeting. Later in the week, Eurozone February flash inflation readings begin next Thursday with France, Spain and Germany. The Eurozone-wide estimate is released on Friday.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/02/2024 | 0800/0900 | ** |  | ES | PPI |

| 26/02/2024 | 0900/0900 |  | UK | BOE's Breeden at BOE agenda for Research Conference | |

| 26/02/2024 | 1100/1100 | ** | | UK | CBI Distributive Trades |

| 26/02/2024 | 1100/1100 | | UK | BOE's Pill at BOE Agenda for Research conference | |

| 26/02/2024 | 1500/1000 | *** |  | US | New Home Sales |

| 26/02/2024 | 1530/1030 | ** | | US | Dallas Fed manufacturing survey |

| 26/02/2024 | 1600/1700 |  | EU | ECB's Lagarde participates in debate on ECB 2022 Report | |

| 26/02/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 2 Year Note |

| 26/02/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 26/02/2024 | 1800/1300 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 26/02/2024 | 1800/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 27/02/2024 | 2330/0830 | *** |  | JP | CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.