Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI INTERVIEW: Ex-FDIC's Bair Sees Limited SVB Contagion Risk

- MNI INTERVIEW: Inflation Proves More Persistent -Fed's Garriga

- MNI INTERVIEW: Inflation Slowdown Should Allow Fed Pause-Tilley

- MNI INTERVIEW: Fed Economist-Low For Long Rate Can Tame CPI

- MNI BRIEF: US Feb Hiring Above Expectations; Wage Growth Slows

US

US: The collapse of Silicon Valley Bank is unlikely to create major waves of contagion or significantly disrupt the financial system as long as regulators manage the situation adequately, former FDIC Chair Sheila Bair told MNI on Sunday.

- “It’s a USD200 billion bank in a USD23 trillion banking industry, so if handled with care, I don’t see it creating contagion,” she said in an interview. “It would be good and I’m sure the FDIC is focused on this, declaring what the uninsured dividend will be tomorrow. It looks like the bank had some very high quality assets, so the recoveries for the uninsured could be substantial.”

- She said SVB’s downfall was the product of a classic run on the bank as the firm faced USD42 billion in withdrawals in 24 hours. “As far as I can tell, Silicon Valley Bank wasn’t insolvent. This was a bank run,” said Bair, who headed the FDIC during the financial crisis of 2008.

FED: Inflation is proving more stubborn than anticipated due to shifts in U.S. consumer spending patterns, a rosier European outlook and China's emergence from it zero-Covid policy, but there are scant signs that rising interest rates will cause a downturn this year, Federal Reserve Bank of St. Louis research director Carlos Garriga said in an interview Friday.

- The U.S. central bank is set to respond to stronger data with a higher peak interest rate potentially held for longer, Fed Chair Jerome Powell said this week. Yet employers created nearly a million jobs in the first two months of the year reflecting robust labor demand, and that bodes well for economic activity overall, Garriga said.

- "I’m cautiously optimistic first quarter growth will be revised to positive territory, that could eventually turn into a positive second half if inflation continues to drop," he said. But, "economic activity is not a strong predictor of inflation," and inflation has fallen less quickly than hoped.

- "Most current estimates indicate we won’t get to the 2% target until mid-year 2024 or early 2025." For more see MNI Policy main wire at 1504ET.

US: U.S. inflation is likely to resume its downward drift in coming months despite bumps along the way, allowing the Federal Reserve to pause its rate increases after a few more hikes, former Philadelphia Fed economic advisor Luke Tilley told MNI.

- Fed Chair Powell’s decision to open the door to a 50-basis-point interest rate hike was understandable given a hot streak of recent data and big revisions to CPI that provided an entirely different picture of how the year ended, said Tilley, now chief economist at Wilmington Trust.

- “Three-month annualized basis core inflation was 8% in the middle of last year and had slowed to 3% by the end of last year. With those revisions it shifted a lot of inflation from the first to the second half of the year. Now instead of a 5% deceleration now it’s something like a 1.5% to 2% deceleration,” he said in an interview with MNI’s FedSpeak podcast. “Inflation looked a lot more sturdy at the end of the year and now they to respond in kind with the rate hikes.” For more see MNI Policy main wire at 1225ET.

- Markets already anticipate that the Fed will opt for a lower-for-longer approach, senior economist and economic adviser Melosi said in an interview, pointing to investors’ expectations at the end of last year for the policy rate to peak in 2023 at a level 75 basis points lower than that suggested by an economic model weighted to past Fed tightening cycles.

- The historical model and financial markets both see "inertia" as interest rates rise to fight inflation, but also when borrowing costs are on the way down again, he said. Less than half the modeled Fed rate hikes are predicted to unwind by early 2025.

- Central banks have been criticized for leaving interest rates low for too long while inflation surged and for hiking into potential recessions. Fed officials say the bigger danger is for rapid price gains to become embedded in the economy, requiring an even more painful tightening later. For more see MNI Policy main wire at 1330ET.

US DATA: U.S. employers hired significantly more workers than Wall Street expected in February, but wage growth slowed and more people entered the workforce, the Bureau of Labor Statistics said Friday.

- Nonfarm payroll employment increased 311,000, above expectations for a 225,000 gain, while the unemployment rate rebounded two-tenths to 3.6%. Average hourly earnings growth over the month slowed a tenth to 0.2%, a tenth weaker than expected, and was 4.6% over the year.

- Despite the stronger-than-expected payrolls figures, the odds that the Federal Reserve will raise interest rates by a larger 50 bps fell to below 50%, according to futures pricing. The U.S. dollar saw downside pressure and the 10-year Treasury yield extended gains. (See: MNI INTERVIEW: Fed Should Hike 50BPS If Data Stay Strong-Kohn)

- Job gains were led by the leisure and hospitality, retail trade, government and health care sectors. Employment declined in information and in transportation and warehousing, the BLS said. Strong employment gains in January and December were revised marginally lower by 34,000.

Late Markets Summary, Tsys Back Near Highs, Stocks Off Lows

- US Treasury futures have drifted back near session highs in late trade, yield curves re-steepen with short end outperforming: 2s10s little off earlier highs of -87.579. Front-month 2Y futures back near early session high of 102-10.75 as implied rate hikes slipping lower again.

- The Fed terminal rate has now fallen back to 5.27% in July'23, down nearly 45bps from Thursday. Fed funds implied now pricing around 33bps for the March meeting.

- From a technical perspective, front month 10Y futures have extended the current corrective bull phase. Price has breached the 20- and 50-day EMA earlier, the latter at 112-31+. The clear break opens 113-15+, a Fibonacci retracement, for direction.

- US equities remain weaker in late trade, the e-mini S&P futures attempting to recover from broad based selling tied to bank stocks. While many had rebounded ahead midday, risk appetite was poor after FDIC took over failed SVIB, appointed receiver.

- Front-month SPX futures are well off midmorning high of 3937.25, currently at 3873.0, after breaching support of 3869.38 50.0% retracement of the Oct - Feb bull cycle.

- Focus turns to next Tuesday's CPI data: MoM (0.5%, 0.4%); YoY (6.4%, 6.0%) next key inflation metric for the Fed to determine policy. Reminder, Fed enters media Blackout at midnight tonight.

OVERNIGHT DATA

- US FEB. PAYROLLS INCREASE 311,000; EST. 225,000

- US FEB. UNEMPLOYMENT RATE RISES TO 3.6% VS 3.4%

- A 'big' 0.2% for AHE but still clearly weaker than expected. Solid difference to stronger non-supervisory

- AHE Unrounded - Feb'23:

- M/M (SA): 0.242% in Feb from 0.273% in Jan

- Y/Y (SA): 4.616% in Feb from 4.363% in Jan

- AHE Non-Supervisory Unrounded:

- M/M (SA): 0.46% in Feb from 0.284% in Jan

- Y/Y (SA): 5.337% in Feb from 5.246% in Jan

- CANADA'S ECONOMY ADDS 21.8K JOBS IN FEBRUARY, BEATING 10K EST

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 222.82 points (-0.69%) at 32027.06

- S&P E-Mini Future down 41.25 points (-1.05%) at 3877.75

- Nasdaq down 156.2 points (-1.4%) at 11180.72

- US 10-Yr yield is down 19.9 bps at 3.7045%

- US Jun 10-Yr futures are up 50/32 at 113-1.5

- EURUSD up 0.0062 (0.59%) at 1.0642

- USDJPY down 1.36 (-1%) at 134.81

- WTI Crude Oil (front-month) up $0.92 (1.22%) at $76.63

- Gold is up $32.68 (1.78%) at $1863.61

- EuroStoxx 50 down 56.59 points (-1.32%) at 4229.53

- FTSE 100 down 131.63 points (-1.67%) at 7748.35

- German DAX down 205.24 points (-1.31%) at 15427.97

- French CAC 40 down 95.21 points (-.3%) at 7220.67

US TREASURY FUTURES CLOSE

- 3M10Y -14.469, -125.293 (L: -127.943 / H: -111.668)

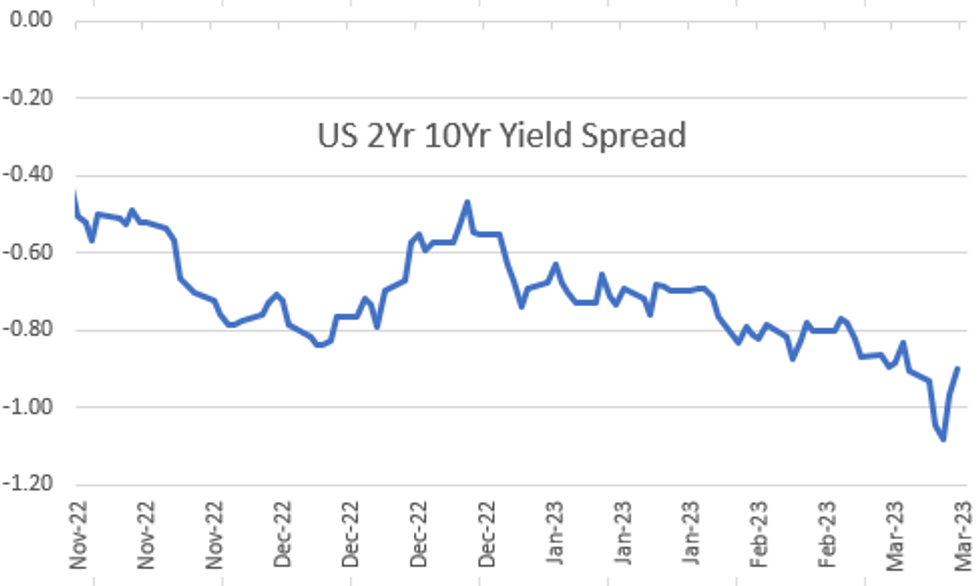

- 2Y10Y +7.524, -89.785 (L: -103.764 / H: -87.579)

- 2Y30Y +13.272, -89.426 (L: -104.468 / H: -87.222)

- 5Y30Y +8.634, -25.91 (L: -33.96 / H: -21.52)

- Current futures levels:

- Jun 2-Yr futures up 20.625/32 at 102-9.875 (L: 101-22.75 / H: 102-10.75)

- Jun 5-Yr futures up 1-05.25/32 at 107-31.75 (L: 106-29.25 / H: 108-04.5)

- Jun 10-Yr futures up 1-19/32 at 113-02.5 (L: 111-20.5 / H: 113-10)

- Jun 30-Yr futures up 3-14/32 at 129-09 (L: 126-03 / H: 129-19)

- Jun Ultra futures up 4-13/32 at 140-24 (L: 136-20 / H: 141-09)

US 10YR FUTURE TECHS: Tops 50-Day EMA Resistance

- RES 4: 114-06+ 61.8% retracement of the Feb 2 - Mar 2 bear leg

- RES 3: 114-00 High Feb 14

- RES 2: 113-15+ 50.0% retracement of the Feb 2 - Mar 2 bear leg

- RES 1: 113-10 High Mar 10

- PRICE: 113-02 @ 1500ET Mar 10

- SUP 1: 111-30/111-20+ 20-day EMA / Intraday low

- SUP 2: 110-20+ Low Mar 8

- SUP 3: 110-12+ Low Mar 02 and the bear trigger

- SUP 4: 110-06 3.00 proj of the Jan 19 - Jan 30 - Feb 2 price swing

Treasury futures traded higher again Friday as price extends the current corrective bull phase. Price has breached the 20- and 50-day EMA, the latter at 112-31+. The clear break here opens 113-15+, a Fibonacci retracement, for direction. On the downside, initial support is seen at Friday’s 111-20+ intraday low.

EURODOLLAR FUTURES CLOSE

- Mar 23 +0.058 at 94.860

- Jun 23 +0.155 at 94.425

- Sep 23 +0.440 at 94.610

- Dec 23 +0.520 at 94.895

- Red Pack (Mar 24-Dec 24) +0.265 to +0.540

- Green Pack (Mar 25-Dec 25) +0.170 to +0.205

- Blue Pack (Mar 26-Dec 26) +0.180 to +0.20

- Gold Pack (Mar 27-Dec 27) +0.190 to +0.195

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00400 to 4.55714% (-0.00243/wk)

- 1M -0.00743 to 4.79857% (+0.08943/wk)

- 3M -0.01557 to 5.13814% (+0.15414/wk)*/**

- 6M -0.07157 to 5.42829% (+0.11158/wk)

- 12M -0.12515 to 5.73814% (+0.04371/wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.15371% on 3/9/23

- Daily Effective Fed Funds Rate: 4.57% volume: $115B

- Daily Overnight Bank Funding Rate: 4.57% volume: $305B

- Secured Overnight Financing Rate (SOFR): 4.55%, $1.120T

- Broad General Collateral Rate (BGCR): 4.51%, $469B

- Tri-Party General Collateral Rate (TGCR): 4.51%, $461B

- (rate, volume levels reflect prior session)

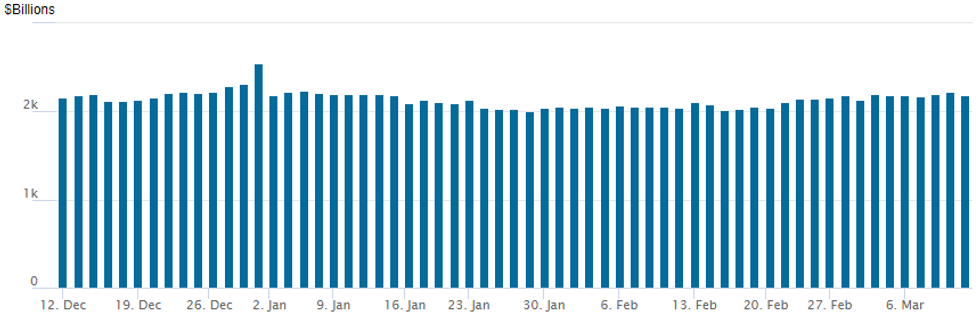

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,188.375B w/ 100 counterparties vs. prior session's $2,229.623B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

EGBs-GILTS CASH CLOSE: US Bank Fears Drag Down European Yields

Concerns over the US banking sector rippled through Europe Friday, with German and UK yields plummeting intraday before stabilising slightly before the cash close.

- German and UK yields tested their lowest levels in the month, with short end yields leading the charge (Schatz yields were at one point set to fall by 26bp, the biggest daily drop since 2008).

- Yields came off their session lows in the last hour of cash trade with some apparent relief on the US banking front as stocks bounced, but remained firmly lower on the day, with some re-steepening after the flattening earlier in the week.

- Terminal hike pricing for the ECB and Fed pared back about 25bp in tandem with Fed rate retracement.

- BTP spreads were fairly well-contained given the circumstances, with the 10Y spread closing just above 180bp.

- Fallout from today's closure by regulators of Silicon Valley Bank - whose troubles triggered the panic - will be eyed over the weekend, with the ECB decision and US CPI coming into focus later in the week.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 18bps at 3.097%, 5-Yr is down 15.1bps at 2.643%, 10-Yr is down 13.5bps at 2.508%, and 30-Yr is down 12.1bps at 2.468%.

- UK: The 2-Yr yield is down 16.9bps at 3.642%, 5-Yr is down 16.3bps at 3.525%, 10-Yr is down 15.6bps at 3.64%, and 30-Yr is down 11bps at 4.012%.

- Italian BTP spread up 6.5bps at 181.1bps / Spanish up 3.4bps at 103.6bps

FOREX: USD Pressure Extends Following NFP, Weighed By Financial Stability Concerns

- Despite the February change in US non-farm payrolls beating estimates, a set of weaker components within the employment report was met with immediate USD selling. With financial stability concerns providing an uncomfortable backdrop, the greenback extended the post-Powell reversal with the USD index looking set to close in line with last week’s close.

- With the Silicon Valley Bank situation in the back of trader’s minds, the weak details within the payrolls report saw an immediate gap lower for USDJPY from around 136.70 to 136.00. Any bounces remained small, and the resulting hours saw the pair fall to fresh lows for the week at 134.12.

- The pair has now traded well below support at 135.37 and has briefly shown below the 50-day EMA, which intersects at 134.23. A clear break of this average would strengthen a bearish threat.

- With the flight to quality in full force, the Swiss franc was a key beneficiary in G10 FX on Friday, with USDCHF posting 1.25% losses on the day. The Euro and GBP were also able to capitalise on the softer greenback, however, the more risk sensitive Aussie relatively struggled, posting 0.14% losses against the dollar, with AUDJPY weakness mirroring the moves in equity markets.

- A further extension of this equity weakness approaching the close provided some moderate relief for the USD index, which looks set to close around 0.7% weaker on the session.

- The key risk events next week are the US CPI report on Tuesday and Thursday’s ECB meeting.

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/03/2023 | - |  | EU | ECB Panetta at Eurogroup Meeting | |

| 13/03/2023 | 1230/0830 | * |  | CA | Household debt-to-disposable income |

| 13/03/2023 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 13/03/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 13/03/2023 | 1805/1805 |  | UK | BOE Dhingra Panellist at International Women’s Day event | |

| 14/03/2023 | 0700/0700 | *** | | UK | Labour Market Survey |

| 14/03/2023 | 0800/0900 | *** |  | ES | HICP (f) |

| 14/03/2023 | 0900/1000 | * |  | IT | Industrial Production |

| 14/03/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 14/03/2023 | 1000/0600 | ** | | US | NFIB Small Business Optimism Index |

| 14/03/2023 | - | | EU | ECB de Guindos at ECOFIN Meeting | |

| 14/03/2023 | 1230/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 14/03/2023 | 1230/0830 | *** | | US | CPI |

| 14/03/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 14/03/2023 | 1400/1000 | * | | US | Services Revenues |

| 14/03/2023 | 2120/1720 | | US | Fed Governor Michelle Bowman |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.