Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: Fed Can Hold Rates Steady, Stay There For A While-Harker

- MNI: Fed Harker Helps Take Edge Off Intraday Lift In Implied Rates

- MNI Atlanta Fed GDPNow Clears 4% For Q3

US

FED: Philadelphia Federal Reserve President Patrick Harker said Tuesday the Fed may be at the point where it can end its cycle of interest rate increases, adding that he sees the U.S. economy on the path to achieving a soft landing.

- “Absent any alarming new data between now and mid-September, I believe we may be at the point where we can be patient and hold rates steady and let the monetary policy actions we have taken do their work," he said in a speech. “Should we be at that point where we can hold steady, we will need to be there for a while," added Harker, a voting member of the FOMC this year. "I do see us on the flight path to the soft landing we all hope for and that has proved quite elusive in the past.”

- Two weeks ago the Federal Reserve raised the fed funds rate another 25 basis points to a range of 5.25% to 5.5% percent, the 11th increase in the span of 12 meetings. For more see MNI Policy main wire at 0815ET.

FED: Philly Fed’s Harker (’23 voter) saying we don’t want to overdo it with Fed tightening and we’ll start cutting rates sometime probably next year helps take the edge off an intraday climb in Fed implied rates.

- It broadly repeats the gist from his prepared remarks earlier today although the mention of cuts comes after similar comments from Williams yesterday, even if it is still consistent with the median dot from the June SEP pencilling in 5.5-5.75% for 4Q23 going to 4.5-4.75% for 4Q24.

- Fed Funds implied rates see +3bp for Sep and a cumulative +8.5bp for a terminal of 5.415% in Nov. Despite cut expectations being trimmed from earlier levels, it’s still followed by 64bp of cuts from terminal to Jun’24 and 141bp of cuts from terminal to Dec’24 for similar levels to Friday’s post-payrolls close.

US TSYS Philly Fed Harker Leans Dovish

- US rates remain strong after the bell, holding to a narrow range after scaling back early session support. No obvious headline driver, US markets appear to be following German Bund's lead (trading 133.45 high, through 133.11 50D EMA resistance).

- Bonds outperformed (USU3 +31 at 122-17 cs. 123-05 high) as curves reversed Monday's steepening: 3s10Y -9.678 at -142.744, 2Y10Y -6.185 at -74.160.

- No significant reaction noted from scant data (US JUN TRADE GAP -$65.5B VS MAY -$68.3B; US JUN WHOLESALE INV -0.5%; SALES -0.7%), with more of the same Wednesday.

- Philly Fed’s Harker (’23 voter) relayed earlier the Fed doesn’t want to overdo it with Fed tightening and we’ll start cutting rates sometime probably next year helps take the edge off an intraday climb in Fed implied rates.

- Harker broadly repeated the gist from his prepared remarks earlier today although the mention of cuts comes after similar comments from Williams yesterday, even if it is still consistent with the median dot from the June SEP pencilling in 5.5-5.75% for 4Q23 going to 4.5-4.75% for 4Q24.

- Strong upsized ($42B) 3Y note sale: trades 19bp through: 4.398% high yield vs. 4.417% WI; 2.9x bid-to-cover vs. 2.88x prior month.

OVERNIGHT DATA

- US JUN TRADE GAP -$65.5B VS MAY -$68.3B

- US JUN WHOLESALE INV -0.5%; SALES -0.7%

US: The Atlanta Fed GDPNow kicks up higher again in the still early days of the Q3 tracker, now seen at 4.1% from the 3.9% in the Aug 1 update.

- Upward revisions to private investment (from 5.2% to 8.1%) offset decreases for personal consumption (from 3.5% to 3.2%) and government spending (from 2.9% to 2.7%).

- If accurate, it would mark a particularly strong rebound from the 2.4% of Q2 and 2.0% of Q1 (itself revised higher multiple times) for the strongest quarter of GDP growth since 4Q21.

- CANADIAN JUN TRADE BALANCE CAD -3.7 BILLION

- CANADA JUN EXPORTS CAD 60.7 BLN, IMPORTS CAD 64.4 BLN

- CANADA REVISED MAY MERCHANDISE TRADE BALANCE CAD -2.7 BLN

MARKETS SNAPSHOT

Key late session market levels- DJIA down 180.05 points (-0.51%) at 35290.13

- S&P E-Mini Future down 25.5 points (-0.56%) at 4512.25

- Nasdaq down 137.1 points (-1%) at 13856.99

- US 10-Yr yield is down 7.5 bps at 4.014%

- US Sep 10-Yr futures are up 11/32 at 111-15

- EURUSD down 0.0043 (-0.39%) at 1.0959

- USDJPY up 0.93 (0.65%) at 143.43

- WTI Crude Oil (front-month) up $1.06 (1.29%) at $83.00

- Gold is down $11.36 (-0.59%) at $1925.20

- EuroStoxx 50 down 48.65 points (-1.12%) at 4288.85

- FTSE 100 down 27.07 points (-0.36%) at 7527.42

- German DAX down 175.83 points (-1.1%) at 15774.93

- French CAC 40 down 50.29 points (-0.69%) at 7269.47

US TREASURY FUTURES CLOSE

- 3M10Y -9.678, -142.744 (L: -150.097 / H: -137.631)

- 2Y10Y -5.976, -73.951 (L: -76.885 / H: -68.38)

- 2Y30Y -6.123, -56.067 (L: -59.978 / H: -50.75)

- 5Y30Y -1.631, 8.557 (L: 5.553 / H: 9.908)

- Current futures levels:

- Sep 2-Yr futures up 0.375/32 at 101-23.25 (L: 101-21.25 / H: 101-25.25)

- Sep 5-Yr futures up 5.25/32 at 107-4.25 (L: 106-27.5 / H: 107-08.25)

- Sep 10-Yr futures up 11/32 at 111-15 (L: 110-31 / H: 111-22)

- Sep 30-Yr futures up 31/32 at 122-17 (L: 121-12 / H: 123-05)

- Sep Ultra futures up 1-8/32 at 128-15 (L: 126-29 / H: 129-11)

US 10Y FUTURE TECHS: (U3) Corrective Cycle Extends

- RES 4: 113-08 High Jul 18 and a bull trigger

- RES 3: 112-31 High Jul 20

- RES 2: 112-15+ 50-day EMA

- RES 1: 111-18+/112-07 20-day EMA / High Jul 27

- PRICE: 111-17 @ 11:25 BST Aug 8

- SUP 1: 110-23/109-24 Low Aug 7 / 4 and the bear trigger

- SUP 2: 109-14 Low Nov 8 2022 (cont)

- SUP 3: 109-10+ Low Nov 4 2022 (cont)

- SUP 4: 108-26+ Low Oct 21 2022 (cont) and a major support

The trend condition in Treasuries remains bearish, however, a bullish corrective cycle remains in play and price has traded higher today. Resistance to watch is 111-18+, the 20-day EMA. A clear break of this average would signal scope for a stronger recovery and potentially expose the 50-day EMA, at 112-15+. The bear trigger has been defined at 109-24, the Aug 4 low. A break would resume the downtrend.

SOFR FUTURES CLOSE

- Sep 23 steady at 94.60

- Dec 23 steady at 94.655

- Mar 24 -0.005 at 94.935

- Jun 24 steady at 95.320

- Red Pack (Sep 24-Jun 25) +0.005 to +0.035

- Green Pack (Sep 25-Jun 26) +0.040 to +0.060

- Blue Pack (Sep 26-Jun 27) +0.065 to +0.070

- Gold Pack (Sep 27-Jun 28) +0.075 to +0.080

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00343 to 5.31240 (-.00784/wk)

- 3M -0.00215 to 5.36528 (-0.00530/wk)

- 6M -0.00172 to 5.42583 (-0.00836/wk)

- 12M -0.02124 to 5.31827 (-0.04408/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $106B

- Daily Overnight Bank Funding Rate: 5.32% volume: $273B

- Secured Overnight Financing Rate (SOFR): 5.30%, $1.349T

- Broad General Collateral Rate (BGCR): 5.28%, $576B

- Tri-Party General Collateral Rate (TGCR): 5.28%, $566B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

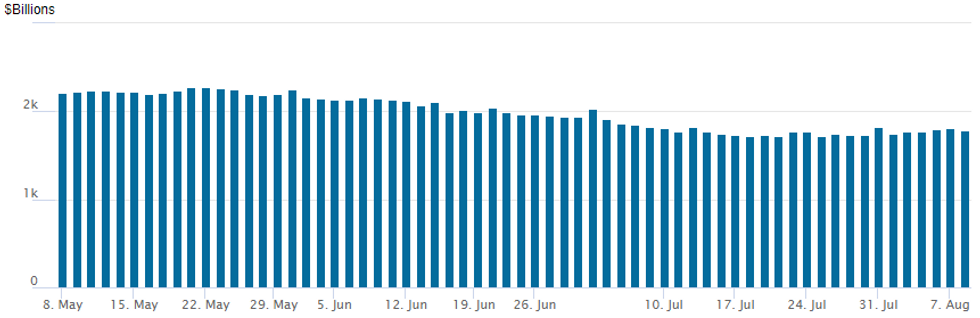

NY Federal Reserve/MNI

The latest operation falls back to $1,778.351B, w/103 counterparties, compared to $1,810.583B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE: Conoco Phillips, Ingersoll Rand Launch

$8.2B high-grade corporate debt to price Tuesday

- Date $MM Issuer (Priced *, Launch #)

- 08/08 $3B #BMW US $800M 2Y +55, $600M 2Y SOFR+62, $1B 5Y +95, $600M 10Y +115

- 08/08 $2.7B #Conoco Phillips $1B 10Y +105, $1B 30Y +135, $700M 40Y +150

- 08/08 $1.5B #Ingersoll Rand $500M 5Y +137, $1B 10Y +177

- 08/08 $1B #Virginia Electric and Power $400M 10Y +128, $600M 30Y +150

EGBs-GILTS CASH CLOSE: Bank Stock Drop Fuels Bull Flattening Rally

The German and UK curves bull flattened sharply, with Bunds outperforming Gilts in a risk-off move Tuesday.

- European bank stocks fell the most since March's turmoil (the index fell as much as 5%), amid a combination of Italy unexpectedly introducing a windfall tax on banks, and Moody's taking credit rating actions on US institutions.

- A further decline in inflation expectations in the ECB's monthly consumer survey added to the dovish tone for core FI.

- Yields bottomed out in early afternoon trade alongside a tentative stabilisation in Euro bank stocks, but the UK and German curves remained near their flattest levels of the session as the short-end underperformed the longer-end bounce.

- Periphery spreads were relatively well-behaved despite the risk-off tone, with the exception of Greece which widened for the 2nd consecutive session.

- Wednesday's schedule is basically vacant in terms of data and central bank speakers, with Thursday's US inflation figures remaining the focus of the week.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 6.9bps at 2.918%, 5-Yr is down 10.3bps at 2.487%, 10-Yr is down 13.2bps at 2.469%, and 30-Yr is down 14.4bps at 2.55%.

- UK: The 2-Yr yield is down 0.9bps at 4.954%, 5-Yr is down 3.5bps at 4.423%, 10-Yr is down 7.6bps at 4.385%, and 30-Yr is down 7.6bps at 4.58%.

- Italian BTP spread down 0.5bps at 165.5bps / Greek up 6bps at 133.7bps

FOREX: USD Index Edges off Highs, Remains Up 0.5%

- Late comments from Philly Fed’s Harker have helped curtail the greenback advance on Tuesday, emphasising that the Fed don’t want to overdo it with tightening. However, the USD remains solidly in the green, with markets taking note of a series of negative sector news for global banks, prompting a flight to quality across the currency complex.

- Moody's cutting their rating on the US Banking sector was compounded by a fresh Italian windfall tax on banking sector profits, significantly weighing on the EuroStoxx50 Bank Index. Risk sensitive currencies such as AUD, NZD and CAD all had meaningful sell-offs across the European time zone before moderately stabilising throughout US hours.

- AUDUSD declined as much as 1.15%, briefly trading below 0.6500 for the first time since June 01, before bouncing around 30 pips ahead of the APAC crossover. The greenback advance was most noticeable against Scandi FX in G10, with both the SEK and NOK declining by over 1%.

- Similar reverberations were sent through to EMFX, with the likes of ZAR and PLN being hit the hardest. Notably, USDZAR has extended its rise in August to around 6%. However, lower yields in the US, buffered by Harker’s remarks have offered some relief for Latin American currencies, which are rebounding into Tuesday’s close.

- Underlying dollar strength worked in favour of USDCNH (+0.48%), placing the pair briefly above the first upside technical level of 7.2457 - the 76.4% retracement for the July downleg. After disappointing trade figures overnight, the data turns focus to July inflation due Wednesday, with CPI seen dropping 0.4% and PPI at -4.0%. A miss on forecast is sure to reignite speculation of further stimulus.

- Elsewhere, global markets remain firmly focused on Thursday’s US CPI data for July.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 09/08/2023 | 0130/0930 | *** |  | CN | CPI |

| 09/08/2023 | 0130/0930 | *** | | CN | Producer Price Index |

| 09/08/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 09/08/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 09/08/2023 | 1230/0830 | * |  | CA | Building Permits |

| 09/08/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 09/08/2023 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.