Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Fed To Frontload Hikes But Keep Eye On Jobs--Ex-Officials

- MNI BRIEF: Forecasters Increase Inflation Views - Philly Fed - PCE inflation seen at 3.1% this year in survey of economists.

- BIDEN: U.S., ALLIES WOULD RESPOND DECISIVELY IF RUSSIA INVADES

- U.S. INTENSIFYING EFFORTS TO DETER RUSSIA, U.S. OFFICIAL SAYS

- UNCLEAR IF RUSSIA INTERESTED IN DIPLOMATIC SOLUTION: OFFICIAL

- U.S. SENATE BANKING COMM TO HOLD VOTE ON FEDERAL RESERVE NOMINEES Feb 15, 1415ET Rtrs

- ONTARIO DECLARES STATE OF EMERGENCY OVER PROTESTS, Bbg

US

FED: The Federal Reserve is likely to begin raising rates in March, probably by 25 basis points, and follow up with hikes in the next few meetings, but signs that tighter policy is hitting the labor market could prompt a mid-year pause, former Fed officials and staff told MNI.

- "They are going to be quite sensitive to the unemployment rate," said Tom Hoenig, former Kansas City Fed President. "If they start to hike rates and after three times they see unemployment start to rise they will hesitate and they will have to think about it carefully. They may then pause, even if inflation stays elevated."

- "They have a very tough needle to thread," he said in an interview with MNI. "They are much more inclined to watch that unemployment number than people otherwise suspect. They are watching it very carefully, every bit as closely as they do the inflation numbers." For more, see MNI Policy main wire at 1045ET.

FED: The Philadelphia Fed's Survey of Professional Forecasters predicts PCE headline and core inflation at 3.1% this year, while estimating 10-year annual-average CPI inflation at 2.5% and seeing CPI ending 2022 at 3.8%.

- Forecasters expect higher inflation in the short run, predicting current-quarter headline CPI inflation to average 5.5%, up from 3.0% in the last survey. Headline PCE inflation over the current quarter is seen at 4.7%, up 1.7ppts from the previous estimate. Over the long run, forecasters dropped their estimates of inflation slightly, predicting PCE headline inflation at 2.2% over ten years.

- The survey's 36 forecasters downgraded their views of the U.S. economy, predicting real GDP will grow at an annual rate of 1.8% in the first quarter before speeding up to 4.2% in the second quarter. Forecasters also downgraded their views for the unemployment rate, expecting it to decline to 3.7% in 2022 and 3.4% in 2023 before moving slightly higher over the following two years.

- In a special question done annually, forecasters dropped their estimate for median 10-year productivity growth to 1.6% from 1.75%.

US TSYS: Risk-Off on Russia Invasion Concerns, US$ Rally, Steady QE TAPER

Aside from the risk-off buying on Russia/Ukraine invasion fears, Tsys extend session highs after the bell -- for a more prosaic reason: measured pace of QE wind-down after NY Fed annc final buy-operations (see 1513ET bullet).

- Final buy-op on Thu March 9: Tsy 2.25Y-4.5Y, appr $4.025B.

- FI markets unwind shorts on bets the Fed could have annc'd an immediate end to QE, quelling chances of intermeeting move prior to March 16 FOMC.

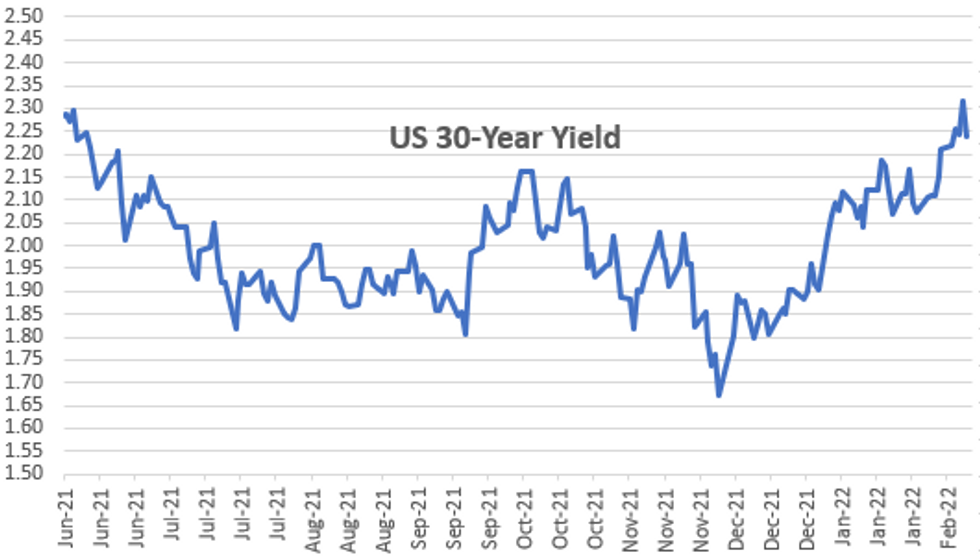

- 30YY falls to 2.2321%, 2.2349 last (-.0814); 10YY falls to 1.9112%, 1.9147%last (-.1147).

Late Trade, Selling Into Risk-Off Bid: Trading desks report pick up in selling after knee-jerk/risk-off move on Russia/Ukraine headline, Tsys have trimmed gains briefly, finish near highs (USH +1-6 at 152-27), equities drew some dip buying but remain weaker (ESH2 around 4418.0).

- Trading desks report leveraged $selling 30s and putting on 5s30s steepeners. Incidentally, 5s30s currently +3.81 at 40.21.

- Eurodollar Options: Better volumes than Treasury options so far, but still fairly sporadic from exhausted markets after Thursday's re-pricing of larger/faster rate hikes due to inflation spike.

- Treasury Options: Trade varied but volumes relatively muted given the shifts in policy pricing since Thursday, not to mention support for underlying futures evaporating around the London close.

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 485.08 points (-1.38%) at 34756.89

- S&P E-Mini Future down 85 points (-1.89%) at 4411.75

- Nasdaq down 396.7 points (-2.8%) at 13790.17

- US 10-Yr yield is down 9.7 bps at 1.932%

- US Mar 10Y are up 24/32 at 126-17.5

- EURUSD down 0.0089 (-0.78%) at 1.1338

- USDJPY down 0.77 (-0.66%) at 115.22

- WTI Crude Oil (front-month) up $3.59 (3.99%) at $93.49

- Gold is up $35.04 (1.92%) at $1861.66

- EuroStoxx 50 down 41.84 points (-1%) at 4155.23

- FTSE 100 down 11.38 points (-0.15%) at 7661.02

- German DAX down 65.32 points (-0.42%) at 15425.12

- French CAC 40 down 89.95 points (-1.27%) at 7011.6

US TSYS FUTURES CLOSE

Levels reflected after the closing bell but prior to settlement:

3M10Y -5.962, 154.345 (L: 153.931 / H: 166.218)

2Y10Y -1.976, 42.484 (L: 38.842 / H: 50.654)

2Y30Y +1.249, 74.409 (L: 65.055 / H: 82.127)

5Y30Y +4.417, 40.814 (L: 31.708 / H: 43.001)

Current futures levels:

Mar 2Y up 4.875/32 at 107-23.75 (L: 107-12.5 / H: 107-25.5)

Mar 5Y up 16.5/32 at 118-1 (L: 117-08.25 / H: 118-02.75)

Mar 10Y up 26/32 at 126-19.5 (L: 125-19 / H: 126-23.5)

Mar 30Y up 1-14/32 at 153-3 (L: 150-26 / H: 153-06)

Mar Ultra 30Y up 1-30/32 at 183-13 (L: 179-20 / H: 183-20)

Settles:

3M10Y -4.567, 155.74 (L: 153.319 / H: 166.218)

2Y10Y -1.913, 42.547 (L: 38.842 / H: 50.654)

2Y30Y -0.303, 72.857 (L: 65.055 / H: 82.127)

5Y30Y +1.841, 38.238 (L: 31.708 / H: 43.001)

Current futures levels:

Mar 2Y up 3.125/32 at 107-22 (L: 107-12.5 / H: 107-25.5)

Mar 5Y up 11.5/32 at 117-28 (L: 117-08.25 / H: 118-02.75)

Mar 10Y up 19/32 at 126-12.5 (L: 125-19 / H: 126-23.5)

Mar 30Y up 1-0/32 at 152-21 (L: 150-26 / H: 153-07)

Mar Ultra 30Y up 1-14/32 at 182-29 (L: 179-20 / H: 183-20)

US 10Y FUTURES TECH: (H2) Fresh Cycle Low

- RES 4: 129-14 High Jan 5

- RES 3: 128-22+ High Jan 24

- RES 2: 128-20 50-day EMA

- RES 1: 127-01/24 High Feb 7 / High Feb 4

- PRICE: 126-00+ @ 11:43 GMT Feb 11

- SUP 1: 125-17+ Low Feb 10

- SUP 2: 125-06+ Low May 30 2019 (cont)

- SUP 3: 125-04+ 2.00 proj of the Jan 13 - 19 - 24 price swing

- SUP 4: 124-22 2.0% 10-dma envelope

Treasuries resumed their downtrend Thursday, solidifying the bearish trend condition. The contract cleared a layer of support between 126-01 and 125-10+ and delivered a fresh cycle low. Thursday’s price action also highlights a continuation of the bearish price sequence of lower lows and lower highs. The focus turns to 125-06 next+, the 30 May 2019 (cont). Firm resistance is seen at 127-01.

US EURODOLLAR FUTURES CLOSE

Levels reflected after the closing bell but prior to settlement:- Mar 22 +0.020 at 99.30

- Jun 22 steady00 at 98.735

- Sep 22 +0.025 at 98.375

- Dec 22 +0.050 at 98.10

- Red Pack (Mar 23-Dec 23) +0.075 to +0.10

- Green Pack (Mar 24-Dec 24) +0.115 to +0.165

- Blue Pack (Mar 25-Dec 25) +0.145 to +0.165

- Gold Pack (Mar 26-Dec 26) +0.125 to +0.135

Settlement:

- Mar 22 +0.030 at 99.310

- Jun 22 -0.005 at 98.730

- Sep 22 +0.010 at 98.360

- Dec 22 +0.030 at 98.080

- Red Pack (Mar 23-Dec 23) +0.045 to +0.075

- Green Pack (Mar 24-Dec 24) +0.095 to +0.150

- Blue Pack (Mar 25-Dec 25) +0.130 to +0.150

- Gold Pack (Mar 26-Dec 26) +0.110 to +0.120

SHORT TERM RATES: Updated Buy-Operation

Fed: Updated NY Fed Operational Purchase Schedule

NY Fed updated purchase schedule: The Desk plans to purchase approximately $20 billion over the monthly period from 2/14/22 to 3/11/22 -- in effect ending intermeeting move. Note: Eurodollar lead quarterly EDH2 +0.030 at 99.31 as 50bp hike odds fall below 50%.

- Tue 02/15 1010-1030ET: Tsy 4.5Y-7Y, appr $3.225B vs. $6.025B prior

- Thu 02/17 1010-1030ET: Tsy 10Y-22.5Y, appr $1.625B steady

- Tue 02/22 1010-1030ET: TIPS 1Y-7.5Y, appr $1.025B vs. $2.025B prior

- Thu 02/24 1010-1030ET: Tsy 0Y-22.5Y, appr $6.225B steady

- Tue 03/01 1100-1120ET: TIPS 7.5Y-30Y, appr $0.625B vs. $1.225B prior

- Thu 03/03 1100-1120ET: Tsy 7Y-10Y, appr $1.625B vs. $3.225 prior

- Tue 03/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B steady

- Thu 03/09 1010-1030ET: Tsy 2.25Y-4.5Y, appr $4.025B

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00086 at 0.07843% (+0.00143/wk)

- 1 Month +0.06743 to 0.19114% (+0.07585/wk)

- 3 Month +0.11157 to 0.50643% (+0.16743/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.17600 to 0.84043% (+0.28500/wk)

- 1 Year +0.26772 to 1.39229% (+0.39329/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $71B

- Daily Overnight Bank Funding Rate: 0.07% volume: $280B

- Secured Overnight Financing Rate (SOFR): 0.05%, $914B

- Broad General Collateral Rate (BGCR): 0.05%, $344B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $337B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage bounces to $1,635.826B w/ 77 counterparties vs. $1,634.146B yesterday -- remains well off all-time high of $1,904.582B on Friday, December 31.

PIPELINE

No new issuance Friday, total $19.85B priced on week.

EGBs-GILTS CASH CLOSE: Early Reprieve Fades In Late Trade

German and UK yields ended up higher Friday following an early reprieve, as global core FI sold off in the afternoon.

- The Gilt curve bear flattened while the German curve bear steepened (reversing early flattening).

- No obvious drivers of late weakness, looked to be a resumption of Thursday afternoon's post-US CPI bearish price action in sympathy with Tsys.

- Periphery EGB yields widened for yet another session, as central bank tightening remained the focus, though finished off early wides.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1bps at -0.321%, 5-Yr is up 0.3bps at 0.086%, 10-Yr is up 1.6bps at 0.3%, and 30-Yr is up 2.3bps at 0.497%.

- UK: The 2-Yr yield is up 5.8bps at 1.42%, 5-Yr is up 3.3bps at 1.442%, 10-Yr is up 2.7bps at 1.551%, and 30-Yr is up 1.1bps at 1.624%.

- Italian BTP spread up 5.5bps at 166.2bps / Greek bond spread up 4.3bps at 233.6bps

FOREX: Greenback Surged Late on Russia Headlines

- After a particularly volatile Thursday session, the US dollar looks set to post a marginally positive week overall, with the dollar index currently 0.25% in the green.

- Expectations for a more hawkish Fed have kept the greenback underpinned despite coming under pressure in the hours following the US CPI data yesterday.

- US$ bounced late after US officials expressed concerns Russia invasion of Ukraine was imminent: EURUSD fell to 1.1336 on Russia headlines after trading either side of 1.1400 on a narrower 60 pip range much of the session; USDJPY fell to 115.06 low from around116 mark.

- EURGBP had the most notable move, retreating 0.5% despite the technical outlook remaining bullish, following the rebound from the major area of support around 0.8300.

- EURSEK also retraced 0.65% from yesterday’s highs following the relatively dovish Riksbank on Thursday. It is worth noting that the pair looks set to post its highest weekly close since September 2020.

- Emerging market currencies traded mixed, with the Mexican peso steadily grinding higher following the Feb Banxico meeting. Conversely the Russian Ruble faltered 1.6% following the CBR considering two hiking options and deciding on the more moderate option of a 100bp hike.

- A very quiet data calendar on Monday before RBA minutes and German ZEW sentiment data on Tuesday. The FOMC will also publish the minutes of their January meeting on Wednesday.

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/02/2022 | 1600/1100 | ** |  | US | NY Fed survey of consumer expectations |

| 14/02/2022 | 1615/1715 |  | EU | ECB Lagarde Speech on anniversary of Euro at EU Parliament | |

| 14/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 14/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 14/02/2022 | 1630/1730 | | EU | ECB Lagarde Intro at ECB Annual Report 2020 Plenum |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.