Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

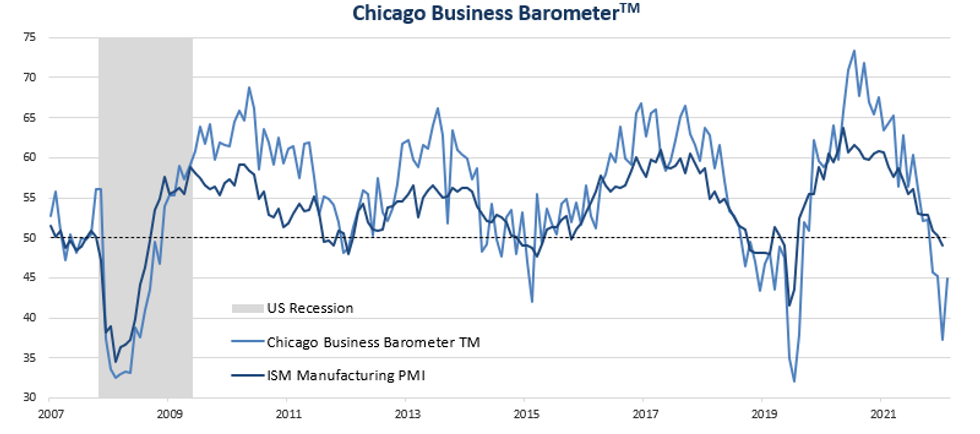

MNI: Chicago Business Barometer™ Improves in December

The Chicago Business BarometerTM, produced with MNI, increased by 7.7 points to 44.9 in December. This month’s recovery broke a three-month streak of falls, yet the index remained contractive for a fourth consecutive month.

The majority of sub-indexes improved over the month, led by Order Backlogs and New Orders whilst upticks in Production and Supplier Deliveries were more muted. Inventories, Employment and Prices Paid all weakened and only Order Backlogs, Supplier Deliveries and Prices Paid were above 50.

Source: MNI / ISM

LAST-MINUTE NEW ORDERS BOOST PRODUCTION

New Orders jumped by 13.4 points to 44.1, the highest since August. A number of last-minute and year-end blanket orders has provided a solid December boost.

Production rose by 3.3 points to 39.2 in December, improving from November’s 29-month low. Material and staff shortages were cited as hampering production, which remained below the 50-breakeven mark since September.

Order Backlogs saw the largest December increase, rising by 17.6 points to 53.7, giving back more than the November fall. Order Backlog levels are now again in line with the 12-month average of 54.4, due to the unanticipated boost in December orders coupled with continued shortages.

PRICE PRESSURES EASE FURTHER

Prices Paid eased a further 2.1 points to 64.1 in December, the lowest since September 2020. The index has followed a general downward trajectory since November 2021. Some firms are expecting higher labor costs. Others highlighted lower demand and falling oil and steel prices pushing prices down. US port congestion is improving and will see shipping and freight cost pressures moderate further. Firms are actively pushing back against higher supplier pricing plans.

Employment weakened by 6.3 points to 40.8 in December, the second lowest level since H1-2020 and only marginally above the September low. Firms struggled to replace employees that had retired or changed workplaces.

The survey ran from December 1 to 19.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.