Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

(Please note that this story replaces "MNI CHINA LIQUIDITY INDEX: China Economic Sentiment Weakens", erroneously published on May 31, which repeated a story originally a published a month earlier)

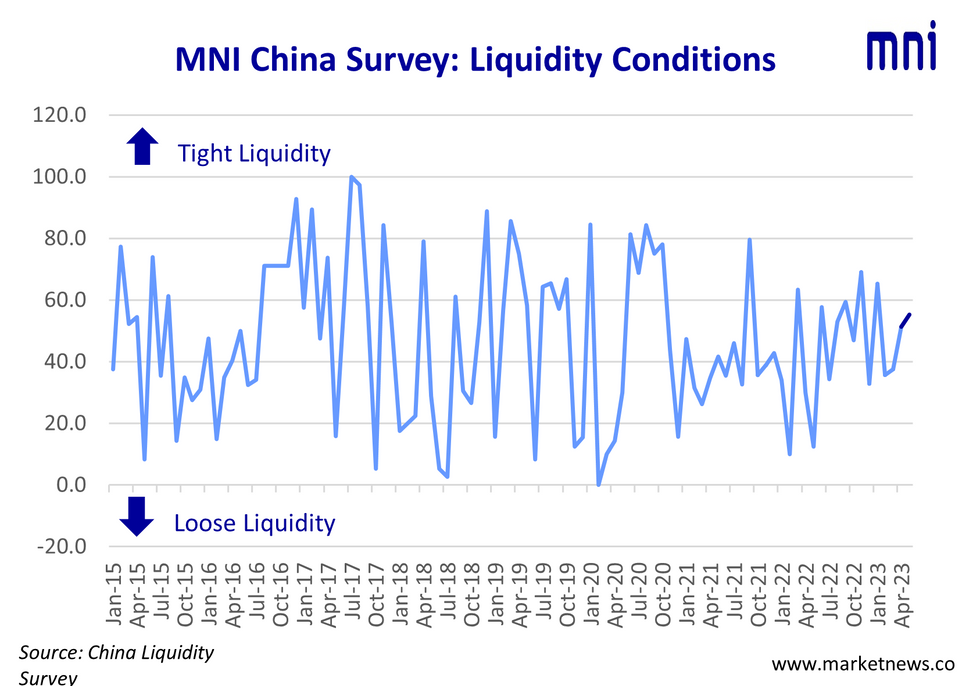

Traders in China’s interbank market reported a moderate tightening of liquidity and a slide in economic sentiment in May, with participants concerned the recovery lacks momentum given recent weak data, the latest MNI China Liquidity Survey showed.

The MNI China Liquidity Condition Index rose to 55.3 in May, from 51.3 in April, the fourth consecutive month of tightening, with 28.9% of the traders reporting tighter conditions.

The higher the index reading, the tighter liquidity.

The People’s Bank of China (PBOC) conducted CNY125 billion of MLF in May, injecting CNY25 billion into the market after offsetting maturities of CNY100 billion. The PBOC drained net CNY689 billion via its open market operation as of May 29, MNI calculated.

“Conditions tightened due to rising government bond issuance,” a trader with a medium-sized commercial bank in Shandong told MNI.

RECOVERY

The MNI China Economy Condition Index fell to 53.9, down from 68.4, the largest m/m drop since last October. Participants believing conditions worsened totalled 28.9%, up from 18.4% previous, with traders citing weak PMI and inflation data as areas of concern.

Fixed-asset investment in Jan-Apr period increased 4.7% y/y, with property development falling 6.2% compared with a year ago. The manufacturing purchasing managers’ index (PMI) also fell to 49.2 in April, down from 51.9 previously, the first time below 50 since December last year. Industrial profits in the first four months slid 20.6% y/y, National Bureau of Statistics data showed.

POLICY HOLD

The MNI China PBOC Policy Bias Index stood at 40.8, down from 44.7, with 81.6% of traders believing the policy stance would be maintained.

The MNI China Guidance Clarity Index dropped to 56.6 from 57.9, with 86.8% of participants saying they understood well the PBOC’s policy intentions.

RATES

MNI’s 7-Day Repo Rate Index read 57.9 in May, down from 63.2, with 28.9% of participants seeing the rate curve falling in the next two weeks and 44.7% predicting a rise.

The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 2.0650%

MNI’s 10-year CGB Yield Index was 52.6, down from 53.9 in April, with 23.7% expecting the curve to fall, based on doubts over the economic recovery, while 28.9% expected yields to rise

The MNI survey collected the opinions of 38 traders with financial institutions operating in the interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted May 15 – May 26.

The full report is available as a PDF:

MNI China Liquidity Index May 2023.pdf

For full database history and full report on the MNI China Liquidity Index™, please contact:sales@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.