Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

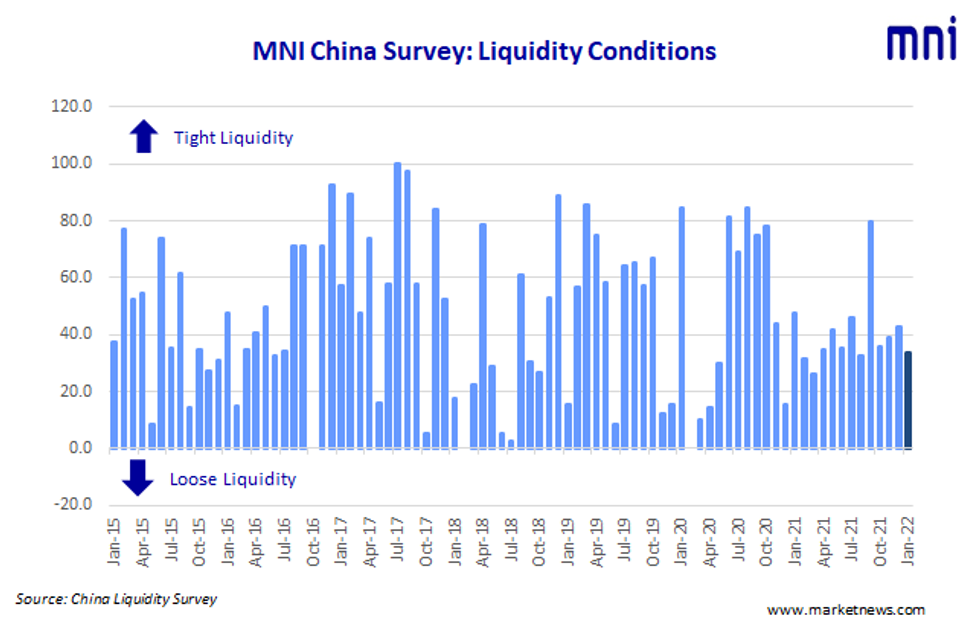

Liquidity across China’s interbank market withstood early year volatility and an improved economic outlook, according to the latest MNI Liquidity Conditions Index.

The Liquidity Condition Index slid to 33.9 in January -- for the first time in two years liquidity was looser in the first month of the year compared to the previous December. Half of the traders surveyed saw condition as “better” due the latest injections from the central bank.

The higher the index reading, the tighter liquidity appears to survey participants.

“Liquidity usually gets more volatile before holidays, especially the lunar New Year Holiday where there are bigger cash demands,” a trader with a state-owned bank based in Shanxi told MNI.

“Funds are influenced by both holiday factors and bond issuance this month,” with both central and local government in tune with investor needs, another trader based in Jiangsu said, “but the central bank will manage needs via its short-term tools.”

The People’s Bank of China conducted CNY500 billion MLF in December, draining CNY200 billion from the market after offsetting the CNY700 billion maturity. The PBOC drained a further net CNY200 billion via its open market operation as of January 25, MNI calculated.

OUTLOOK

The Economy Condition Index rose to 28.6 in January from 8.9 in December, the highest in seven months, with some traders upbeat on the back of the latest economic data. However, many were still aware of downside risks.

“The economy is resilient, with GDP increasing 8.1% in 202. Industrial output has also recorded three consecutive rebounds,” an upbeat Beijing based trader told MNI.

STEADY POLICY

The PBOC Policy Bias Index stood at 42.9 in January, up modestly from the 41.1 seen in December, with 85.7% of the participants saying current policy will be well implemented.

The Guidance Clarity Index came in at 55.4 in January, also little changed from December’s 53.6 reading, with 89.3% of the traders surveyed saying they saw a clear signal or message from central bank’s moves.

RATES DOWN

The 7-Day Repo Rate Index fell to 39.3 from 78.6 reading, with 28.6% of the participants predicting a lower rate in two weeks when seasonal factors fade.

The 7-day weighted average interbank repo rate for depository institutions (DR007) closed 1.9918% on Tuesday.

The 10-year CGB Yield Index stood at 66.1 in January, down from 76, with 28.6% seeing the yield going lower.

FURTHER RESERVES CUT?

The central bank cutting policy rates has left the market expecting further loosening moves. MNI added a special question in January survey: “Do you think another reserve cut is possible?” In response, 42.9% participants said they still expect a reserve cut while another 25.0% didn’t.

The MNI survey collected the opinions of 28 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions. Interviews were conducted Jan 10 – Jan 21Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.