Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

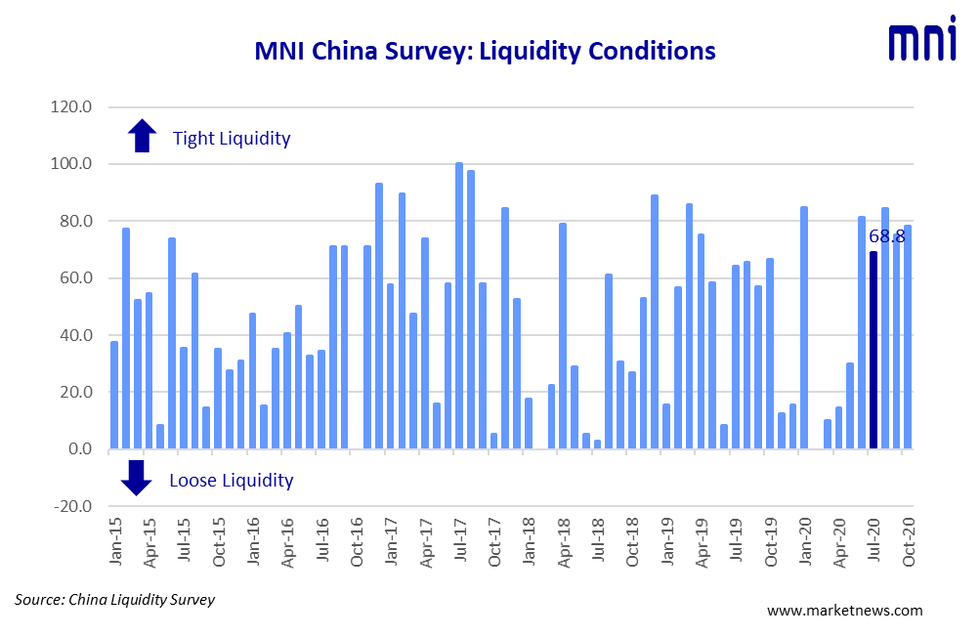

Liquidity was little changed across China's interbank markets in October although they were tighter at the medium-and-longer end of the curve, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index picked up to 78.1 in October from September's 75.0, with 62.5% respondents reporting tighter condition on the back of increased bond issuance and tax payments.

The higher the index reading, the tighter liquidity appears to survey participants.

One trader with a state-owned bank in Anhui said liquidity was well controlled by the People's Bank of China through the money markets, with funds seen as ample and not overflowing.

Another trader pointed to the increased bond issuance through October, particularly as many local governments looked to push through special bond issuance by the end of the month in order to meet Ministry of Finance-imposed targets.

The PBOC conducted CNY500 billion MLF in the month to offset the maturing CNY200 billion MLF then to release some medium-and-longer term funds. They drained CNY560 billion via open market operations as of October 27, MNI calculated.

STRONG ECONOMIC RECOVERY

The Economy Condition Index rose to 93.8 in October from 90.6 previously -- the highest in six years. Just under 90% of participants responded positively when asked about the current state of the economy.

China's Q3 GDP, reported in October, rose 4.9% y/y, or 2.7% q/q, putting YTD GDP in positive territory, up 0.7% y/y. Retail sales rose 3.3% y/y growth in September, up from the negative growth seen in August.

NORMAL POLICY

The PBOC Policy Bias Index rose to 65.6 in October, up from September's 59.4, with 31.3% of traders expecting a more "normalized policy" over the coming year as the pandemic impact fades.

The Guidance Clarity Index stood at 62.5 in October, slightly lower than the 65.6 previously, with three-quarters of respondents seeing improved transparency transparency.

RISING YIELDS

The 7-Day Repo Rate Index slid to 71.9 from last 75.0, with more than half of the participants predicting the rate will rise in coming weeks due to tax payments and bond issuance.

The 7-day weighted average interbank repo rate for depository institutions (DR007) closed at 2.5907% Tuesday.

The 10-year CGB Yield Index rose for a second consecutive month to 75.0 in October, following September's 65.6. Nearly 60% of the traders were seeing the hiking of the yield.

The MNI survey collected the opinions of 16 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed-income and currency instruments, and the main funding source for financial institutions. Interviews were conducted Oct 12 – Oct 23.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.