Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

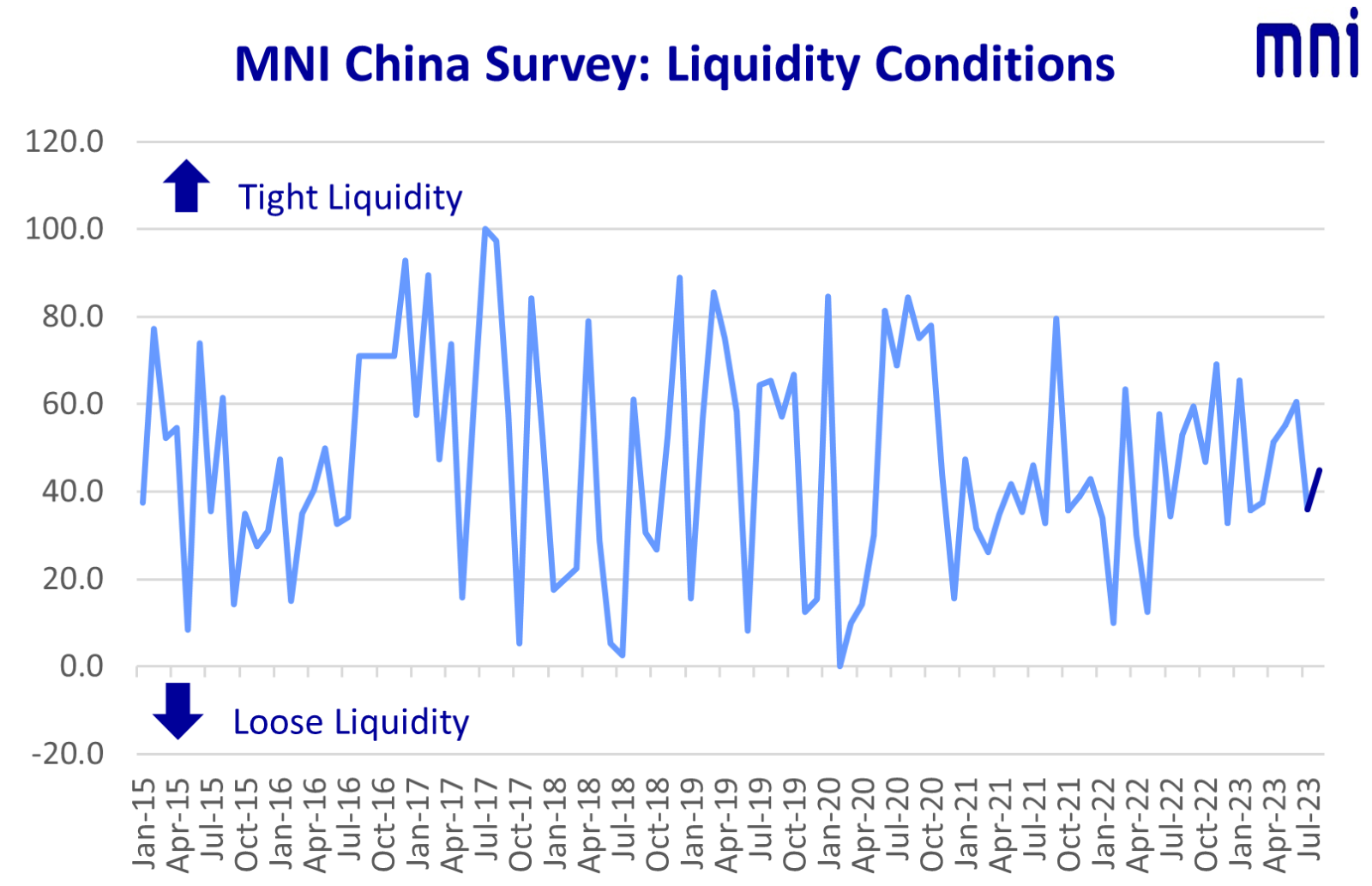

China’s interbank market liquidity tightened modestly in August but remained ample as the People’s Bank of China (PBOC) ensured funds were available to support the economic recovery. However, traders' outlook on the economy fell to the lowest level since May 2022, as authorities have struggled to inspire market confidence with recent policy announcements, the latest MNI Liquidity Conditions Index showed.

The MNI China Liquidity Condition Index climbed to 44.9 in August from July’s 35.9, with 23.1% of traders reporting tighter conditions, up 5.1 percentage points on last month.

The higher the index reading, the tighter liquidity.

“Conditions tightened as banks met deposit obligations with the treasury, but the central bank has filled the gap via open market operations,” a trader with a big commercial bank based in Jiangsu told MNI.

Looking forwards advisors recently told MNI the central bank will boost liquidity by cutting reserve requirement ratios in order to facilitate increased local government debt issuance in Q3. (See: MNI: PBOC To Support Local Govt Debt Sales, Advisors Say - Bonds & Currency News | Market News)

The PBOC conducted CNY billion MLF401 in August, injecting CNY1 billion after offsetting a maturity of CNY400 billion MLF. The PBOC injected net CNY685 billion via its open market operation as of August 28, MNI calculated.

The MNI China PBOC Policy Bias Index stood at 38.5 with 76.9% of local traders expecting the PBOC to maintain prudent monetary policy, and 23.1% anticipating further easing.

Regarding offshore liquidity, forex traders recently told MNI authorities were using tools including issuing yuan-denominated bonds to tighten offshore liquidity and support the value of the Yuan. (See: MNI: Yuan Seen As High As 7.0 After PBOC, Politburo Moves - Bonds & Currency News | Market News)

ECONOMY DROP

The MNI China Economy Condition Index fell to 25.5 in August, from 37.2 in July, marking the lowest point since May 2022, when Shanghai was in lockdown, with 59.0% of participants noting a lack of confidence in the economy.

China's industrial production grew 3.7% y/y in July slowing from 4.4% in June, retail sales rose 2.5% y/y, down from the previous 3.1%. Fixed-asset investment from January to July increased 3.4% y/y, although property sector investment fell 8.5% y/y.

“Recent economic data missed expectations, especially on consumption and investment which grew slowly, this shows short-term momentum is insufficient,” a Beijing-based trader told MNI.

Beijing sought to settle market concerns by cutting stamp duty on securities trading and relaxing mortgage rules. China's one-year Loan Prime Rate was cut to 3.45% from 3.55% following the PBOC's cut to the Medium-lending Facility by 15bps to 2.5% and the seven-day reverse repo rate by 10 bps to 1.80%. (See: MNI PBOC WATCH: Data-Driven PBOC Cuts Could Push LPR Lower - Bonds & Currency News | Market News)

Investor sentiment declined further when Country Garden, a supposedly high quality property developer with government support failed to repay offshore debt. (See: MNI: Country Garden Bigger Blow Than Evergrande- Fund Managers - Bonds & Currency News | Market News)

RATES DECLINE

The MNI China 7-Day Repo Rate Index fell to 26.9 in August, compared with 38.5 in July, with 53.8% of the participants seeing rates falling in coming weeks.

The MNI China 10-year CGB Yield Index read 34.6, down from previous 37.2, with 38.5% of local traders seeing a fall in the curve based on a weak recovery and loose capital. “The 10Y yield is likely to drop following the rate cuts, and the recovery is not strong enough to allow the curve to rise,” a senior trader based in Shanghai said.

RRR CUT

Given market calls for more supportive policies, MNI’s asked “Do you expect a RRR cut in next two months?”, 56.4% of local traders said "very likely yes”, whilst 20.5% were unsure, with the remainder saying unlikely.

“A RRR cut is likely given a huge amount of maturing MLF funds are approaching, the cut is needed to meet increasing credit demands,” a Beijing trader said.

The full report is available here:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.