Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI BanRep Preview - July 2022

Executive Summary

- The majority of surveyed analysts expect BanRep to hike the overnight lending rate by 150bps from 7.50% to 9.00% on Friday.

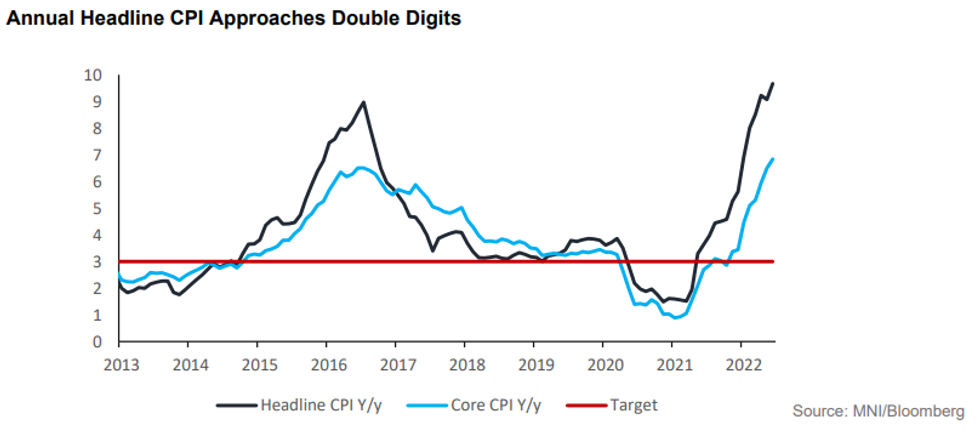

- Annual headline inflation is approaching 10% and the latest central bank surveys point to a continued deterioration of medium-term expectations.

- Inflation dynamics, combined with a resilient growth profile and substantial weakening of the local currency indicate the significant likelihood that BanRep maintain its aggressive pace of tightening.

Click here for the full preview: MNI BanRep Preview - July 2022.pdf

Minutes Confirm Need for Further Aggressive Action

The BanRep board used the June policy meeting minutes to affirm the justification for the bolder unanimous action. “The Board stressed that inflation expectations from various surveys have risen significantly, thus increasing the risk of de-anchoring them.” With this said, it is important to note that inflation expectations have continued their upward trajectory. In the latest BanRep survey of economists, year-end CPI is now predicted at 9.22% versus 8.62% from the prior survey. Additionally, medium-term expectations showed a similar deterioration, with the 2023 year-end median estimate rising from 5.2% from 4.66%.

Additionally, the minutes “also cautioned against the inflationary effects that could arise from the recent peso depreciation”. Given the aforementioned developments for the Peso, the central bank has little to gain from sending a relative dovish message with a below consensus hike at this juncture. Furthermore, given the sustained positive growth momentum, highlighted by May economic activity registering at 16.5% Y/y versus 12.0% in April, the most probable outcome will be a 150 basis point hike from 7.50% to 9.00% at the July meeting.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.