Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

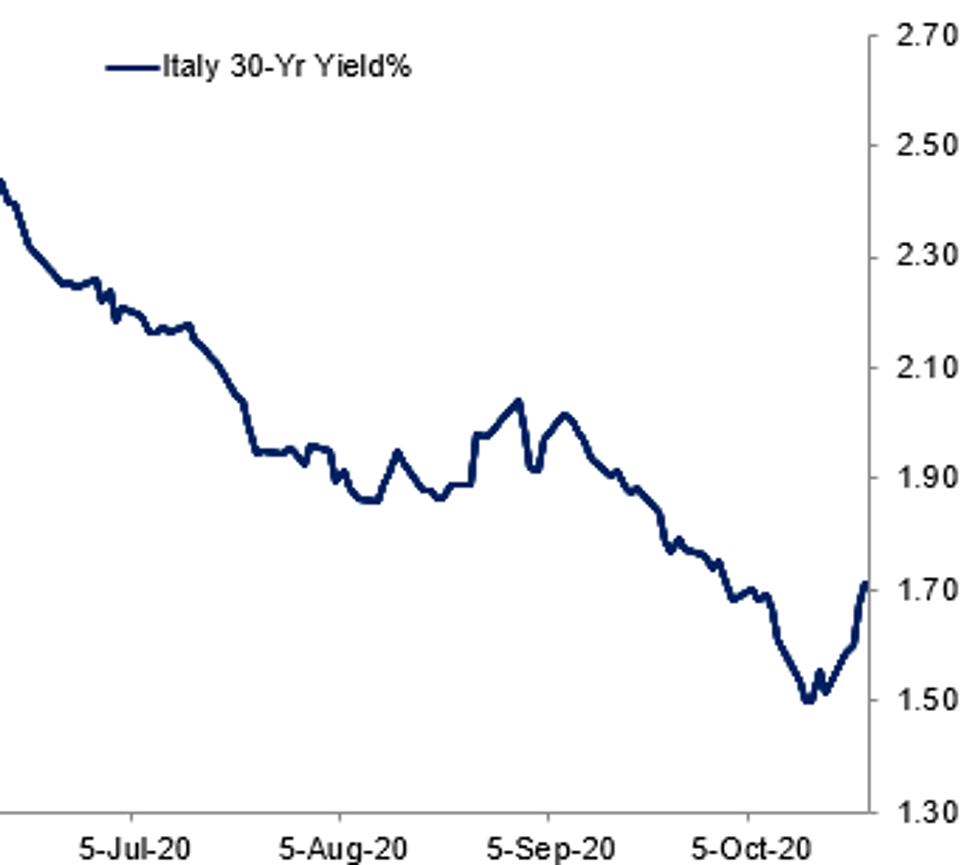

Fig. 1: BTP Issuance In Focus

BBG, MNI

BBG, MNI

EGB SUMMARY: Bunds head lower as equities reverse losses

- After being stable for most of the day, fixed Bunds began following Treasuries lower around 2:00BST - shortly before the US cash open with curve steepening, equities going bid and some continued optimism surrounding US fiscal stimulus prospects helping risk appetite.

- BTPs have been in focus with the syndicated exchange transaction seeing a new 30-year BTP launched for EUR8bln but with just shy of EUR10bln of buybacks of shorter-dated debt.

- Bund futures are down -0.30 today at 175.41 with 10y Bund yields up 1.1bp at -0.578% and Schatz yields unch at -0.779%.

- BTP futures are down -0.16 today at 148.68 with 10y yields up 0.5bp at 0.786% and 2y yields down -1.4bp at -0.329%.

- OAT futures are down -0.34 today at 169.39 with 10y yields up 1.5bp at -0.297% and 2y yields down -0.5bp at -0.704%.

GILT SUMMARY: Sunak Ups The Ante On Job Support Scheme

Gilts have been offered today and the curve has bear steepened.

- Cash yields are now 2-4bp higher on the day and the curve 2bp steeper. Last yields: 2-year -0.0384%, 5-year -0.0322%, 10-year 0.2712%, 30-year 0.8437%.

- The Dec-20 gilt future trades at 135.52, towards the lower end of the day's range (L: 135.45 / H: 135.87).

- Chancellor of the Exchequer Rishi Sunak as announced further job support measures following the fresh surge in coronavirus infections and tightening of social restrictions across the UK.

- The DMO earlier sold GBP2.25bn of the 0.625% Jul-35 Gilt and GBP1.75bn of the 0.625% Oct-50 Gilt. A further GBP382.0mn and GBP236.875mn of the respective issues was taken up through the PAOF.

- Tomorrow will see the release of retail sales for September and preliminary PMI data for October.

DEBT FUTURES/OPTIONS:

- Vol seller: LF1 100.00^ sold at 8.5 in 2k all day

- Bull flattener: 0LM1/LM1 100.12/100.25cs, bought the mid for half in 4.5k

- LH1 99.875/100.00^^, bought for 6 in 10k - potentially short cover as has been sold at 6.5 incl yesterday

- RXZ0 176c, sold at 59.5 in 1.8k * ref 175.54

- Bund downside: RXZ0 174.50/173.00ps vs 178.00c, bought the ps for 15 and 17 in 1.7k calls.

- Bund far OTM downside: RXZ0 166.00p, bought for 1 in 2.6k

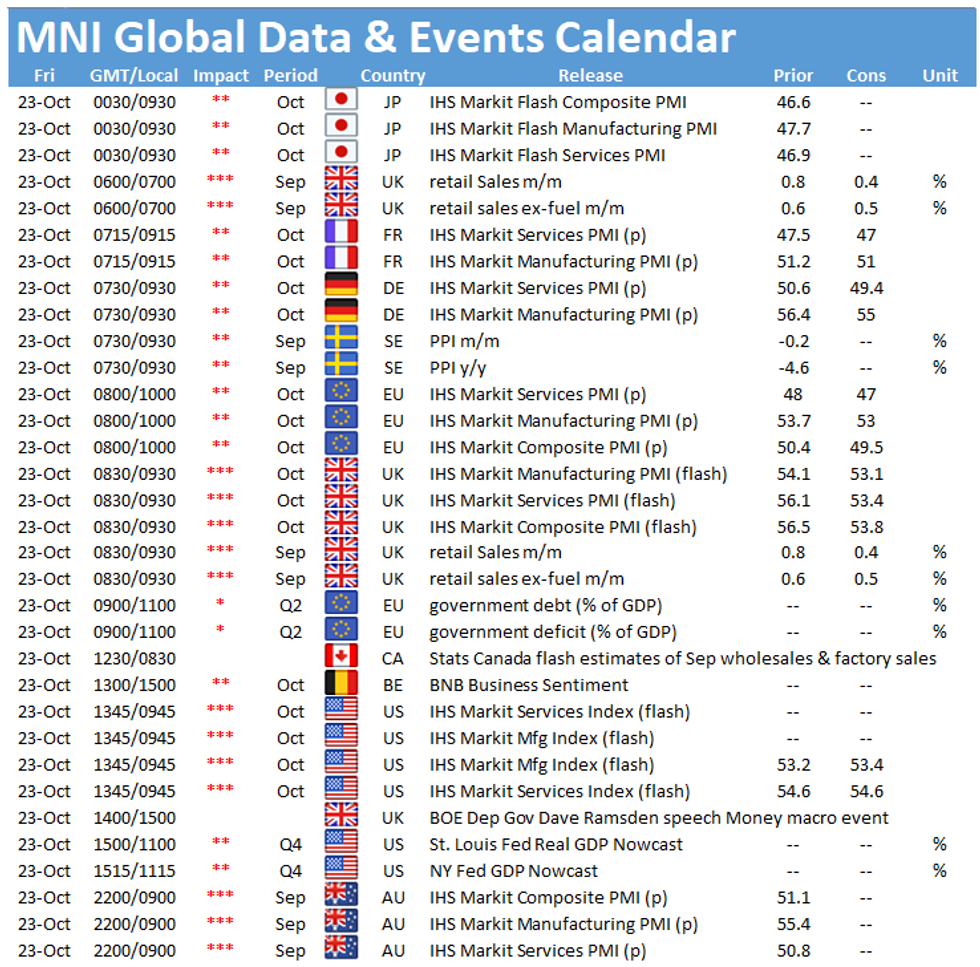

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok