Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

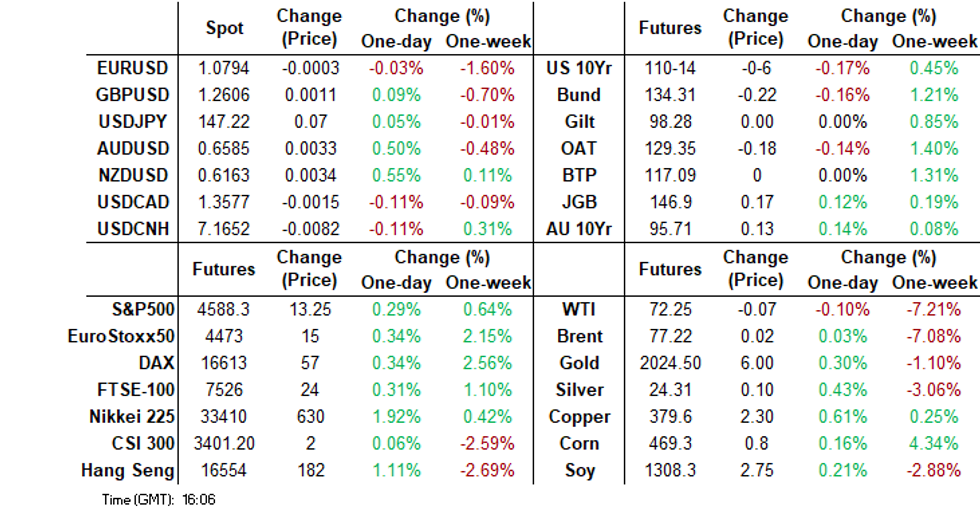

- AUD and NZD are leading the bid in the G-10 space today, the move higher has been seen alongside firmer regional equities and US equity futures.

- A$ outperformance came despite a disappointing Q3 GDP update, see below for more details. ACGBs (YM +8.0 & XM +11.0) sit richer but 3bps cheaper than pre-GDP data levels.

- Elsewhere, cash tsys sit 1-3bps cheaper across the major benchmarks, light bear flattening is apparent. Oil is little changed, while gold is softer.

- In Europe today German Factory Orders and Eurozone Retail Sales headline, further out we have ADP private payrolls and trade balance. The Bank of Canada meets and is expected to be on hold.

MARKETS

US TSYS: Trim Tuesdays Gain In Asia, Narrow Ranges

TYH4 deals at 110-24, -0-05+, a 0-09 range has been observed on volume of ~109k.

- Cash tsys sit 1-3bps cheaper across the major benchmarks, light bear flattening is apparent.

- Tsys trimmed Tuesday's gains in early dealing, Asia-Pac participants perhaps used the richening as an opportunity to square positions ahead of Friday's NFP print.

- Ranges remained narrow and the move lower didn't follow through, tsys pared losses ticked away from session lows.

- In Europe today German Factory Orders and Eurozone Retail Sales headline, further out we have ADP private payrolls and trade balance.

JGBS: Richer, Off Best Levels, 30Y Supply Tomorrow

In Tokyo afternoon dealings, JGB futures are holding richer, +27 compared to settlement levels, but off the session’s best levels.

- In an otherwise quiet calendar, BOJ Deputy Governor Himino said the central bank can make a smooth exit from monetary easing once sustainable 2% inflation is achieved, but it needs to keep policy loose for now. "The BOJ should carefully monitor the evolution of wages and prices, judge the timing of the exit and design its process," Himino said. (See Bloomberg link ICYMI)

- The move away from the session’s best level for the futures contract can therefore be traced back to the 1-3bps cheapening in cash US tsys in today’s Asia-Pac session. After the strong rally overnight, local participants may be using it as an opportunity to square long positions ahead of Friday’s NFP data.

- The cash JGB curve has bull-flattened beyond the 1-year (+1.8bps), with yields 0.2bp to 8.4bps lower. The benchmark 10-year yield is 2.7bps lower at 0.643% versus the new low of 0.622% for the decline that started in early November.

- Swaps curve has bull-flattened too, with rates 0.1 to 4.4bps lower. Swap spreads are wider beyond the 4-year.

- Tomorrow, the local calendar sees International Investment Flow and Tokyo Average Office Vacancies data, along with the Leading and Coincident Indices.

- The MOF also plans to sell Y900bn of 30-year JGBs.

AUSSIE BONDS: Richer But Off Best Levels Despite Q3 GDP Miss

ACGBs (YM +8.0 & XM +11.0) sit richer but 3bps cheaper than pre-GDP data levels. This came even though Q3 GDP surprised on the downside in terms of headline growth and its composition.

- Q3 GDP came in lower-than-expected at 0.2% q/q but the annual rate was higher at 2.1% y/y, in line with Q2. The composition of growth was soft given it was driven by government spending/investment and inventories. Non-dwelling construction was a bright spot though in the private sector.

- The move away from the best levels was assisted by the 1-3bps cheapening in cash US tsys in today’s Asia-Pac session. After the strong rally overnight, local participants may have used it as an opportunity to square long positions ahead of Friday’s NFP data.

- Cash ACGBs are 8-11bps richer on the day, 3-4bps cheaper in post-data dealings, with the AU-US 10-year yield differential 7bps tighter at +12bps. The differential was +19bps before the RBA decision yesterday.

- Swap rates are 6-9bps lower on the day, with EFPs little changed.

- The bills strip is holdings its bull-flattening, with pricing flat to +9.

- RBA-dated OIS pricing is 3-10bps softer on the day across meetings. This brings the post-RBA softening across meetings to 6-17bps.

- Tomorrow, the local calendar sees Trade Balance data for October.

AU STIR: RBA Dated OIS Extends Its Post-RBA Decision Softening

RBA-dated OIS pricing has experienced a 2-9 bps softening across meetings today, building on the downward trend observed after the recent RBA decision. As of the present moment, the softening from pre-RBA levels has aggregated to 6-15 bps across various meetings.

- With only around a 10% probability assigned to a 25bp hike occurring yesterday, the recent adjustment in pricing can be ascribed to the RBA statement lacking any hawkish undertones.

- Simultaneously, there has been a 5 bps reduction in terminal rate expectations today, settling at 4.37%. This revision aligns with the broader softening observed across the $-bloc in response to yesterday's disappointing US JOLTs job openings data.

- Looking ahead, the US economic calendar today features the ADP private payrolls report, with Non-Farm Payrolls scheduled for Friday.

- The current movement adds to the persistent decline in the anticipated terminal rate, marking a 14 bps decrease since the release of October's CPI Monthly data, which fell below expectations last week.

Figure 1: RBA-Dated OIS – Pre-RBA Vs. Post-RBA

Source: MNI – Market News / Bloomberg

RBA: MNI RBA Review - December 2023: On Hold, Watching & Waiting

- The RBA left rates at 4.35%, as expected, at its last meeting for 2023. The central bank retained its tightening bias with the final guidance paragraph unchanged word-for-word. It is in wait-and-see-mode, especially for the Q4 CPI data.

- Some of its November inflation concerns were restated in this month’s statement but there was nothing mentioned to suggest that they have become less worrying. If anything, there hasn’t been enough information yet to determine if they have dissipated. Thus, more emphasis has been put on upcoming CPI releases.

- The key data point ahead of the February 6 decision is likely to be Q4 CPI data on January 31 and currently there is little room in the projections for an upside inflation surprise. The meeting will also include updated staff forecasts, which will now be published, including the Statement on Monetary Policy, with the meeting statement and the decision will be followed an hour later by a press conference.

- See full review here.

AUSTRALIAN DATA: “Productivity Growth Picks Up” As Hours Worked Fall

Q3 productivity grew 0.8% q/q, the first quarterly rise since Q1 2022, but it is still down 2.1% y/y. This is good news for the RBA who has said that wage growth is still consistent with the inflation target if “productivity growth picks up”. The improvement though was predominantly driven by a 0.6% q/q drop in hours worked as the labour market eases rather than because of an improvement in efficiency, but it buys time for the latter to occur.

- Productivity is important for keeping a lid on unit labour cost (ULC) growth at a time of rising wages. The solid Q3 wage outcome due to government policy and the Fair Work Commission’s ruling on minimum wages plus the tight labour market meant that there was a strong rise in ULC of 2.2% q/q, less than Q3 2022, and 6.4% y/y, down from 6.9% in Q2.

Source: MNI - Market News/ABS

- If hours worked fall by the same amount as Q3 over the next two quarters and real GDP grows as the RBA expects, then its desired 1% productivity growth would be achieved by Q1 next year helped by very favourable base effects. If hours worked are flat instead, then it will be by mid-2024.

- If there are no further quarterly falls in hours worked ULC growth is likely to remain above 2% y/y using the RBA’s WPI assumptions. The scenario above where they fall further will result in them growing by less than 1% in H2 2024.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: GDP Disappoints – Headline And Composition

Q3 GDP came in lower-than-expected at 0.2% q/q but the annual rate was higher at 2.1% y/y, in line with Q2. The composition of growth was soft given it was driven by government spending/investment and inventories. Non-dwelling construction was a bright spot though in the private sector. Slower private growth and the first rise in productivity since Q1 2022 should reassure the RBA that monetary policy is working.

- Revisions and the subsequent base effects boosted Q3’s annual rate. Q3 2022 GDP was revised down to 0.2% q/q from 0.7%, and Q4 2022 and Q1 2023 were revised higher. Despite this the RBA’s Q4 forecast can be achieved/undershot with a realistic reading of 0.4% or less.

Source: MNI - Market News/ABS

- Domestic demand rose 0.5% q/q but has slowed from Q2’s 0.9% and Q1’s 0.7%, which should please the RBA. Household consumption was disappointing but the ABS said it was because government subsidies reduced services spending on electricity. Spending was flat to be up only 0.4% y/y, it has been lacklustre for 4 straight quarters but not contracting yet. Government spending grew 1.1% q/q and contributed 0.2pp.

Source: MNI - Market News/ABS

- The household savings ratio fell to 1.1% due to higher tax liabilities and interest payments. While it’s still positive, it’s the lowest since Q4 2007. Governor Bullock has said that aggregate savings buffers are still untouched but that may change in the quarters ahead.

- Total GFCF grew 1.1% q/q and 5.9% y/y with growth from public corporations remaining very strong. Private capex rose a solid 1.2% q/q and 4% y/y driven by a 3.3% increase in mining construction. Dwellings rose only 0.2% q/q & fell 0.3% y/y and machinery & equipment fell 0.5% but is up 7.7% y/y.

- Inventories contributed 0.4pp which the ABS said was due to falling mining exports but this followed a large 1.2pp Q2 detraction. Net exports were a 0.6pp drag, with exports down 0.7% q/q but imports up 2.1%. Services trade also detracted.

NZGBS: Richer, Off Best Levels, Flatter Curve, US ADP Employment Data Due

NZGBs closed 1-10bps richer across benchmarks after paring morning strength. The initial strength had been induced by a strong rally in US tsys during yesterday’s NY session following lower-than-expected JOLTS job openings data. It also reflected spillover from post-RBA decision strength in ACGBs. The local market was closed at the time of the RBA policy decision.

- With the local data calendar light today, the move away from the best levels likely reflected the 1-3bps cheapening in cash US tsys in today’s Asia-Pac session. After the strong rally overnight, local participants may have used it as an opportunity to square long positions ahead of Friday’s NFP data. Later today the US calendar shows ADP private payrolls.

- Swap rates closed flat to 9bps lower, with the 2s10s curve flatter and implied swap spreads wider.

- RBNZ dated OIS pricing closed little changed, with the expected terminal OCR 1bp firmer at 5.55%.

- Tomorrow, the local calendar is empty, ahead of Q3 Manufacturing Activity on Friday.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 4.5% Apr-27 bond, NZ$200mn of the 1.5% May-31 bond and NZ$50mn of the 2.75% Apr-37 bond.

FOREX: Antipodeans Firm In Asia

AUD and NZD are leading the bid in the G-10 space today, the move higher has been seen alongside firmer regional equities and US equity futures. US Tsy Yields are a touch higher and Oil is little changed.

- AUD/USD looked through a miss on the Q3 GDP data and sits ~0.6% higher. The $0.66 handle remains intact and resistance comes in at $0.6623, high from Dec 5.

- Kiwi is up ~0.6%, NZD/USD last prints at $0.6165/70. Bulls immediate focus is on the $0.62 handle.

- Yen is a touch pressured, higher US Tsy Yields are weighing, however USD/JPY has sat in a narrow range for the most part in Asia. The Japanese data docket was empty today.

- Elsewhere in G-10 GBP and CAD are a touch higher, the EUR is flat. BBDXY is ~0.1% lower.

- In Europe today German Factory Orders and Eurozone Retail Sales headline the docket.

EQUITIES: China Markets Lag Broader Rebound, Australian Shares Outperform

MNI (AUSTRALIA) Regional equities are mostly higher, except for some pockets of weakness in South East Asia. A core yield pull back through Tuesday has been a factor aiding sentiment, although US nominal cash Tsy yields are higher in the first part of Wednesday trade. US equity futures sit higher though after an indifferent Tuesday cash session. Eminis last +0.30% at 4588.5, while Nasdaq futures are slightly higher at +0.43%.

- Hong Kong markets have pushed higher, with the HSI up 0.73% at the break. The tech sub index is outperforming, +1.3%.

- China markets are only modestly higher though in terms of the CSI 300, +0.15% at the break, while the Shanghai Composite sits down slightly (-0.11%). This follows sharp losses and Moody's credit rating outlook downgrade yesterday.

- Onshore media has pushed back against this today, while also stating that the stock market hit a mild bull market in 2024 (Securities Times/BBG). Headlines have also cross from the NDRC that China has scope for macro adjustments to support the economy (NDRC).

- In Australia, the ASX 200 is up strongly, +1.7%, despite a disappointing Q3 GDP update. Financials and resource names have been the outperformers.

- Japan stocks are higher, +1.8% for the Nikkei 225, with lower core yields buoying tech related plays. The Kospi and Taiex have seen more modest rises, up around 0.30%.

- In SEA trends are more mixed, the Philippines and Malaysia bourse are down modestly.

- In India, we continue to see upside momentum, the Nifty up a further 0.50% in early dealings. This is fresh record highs for the index.

OIL: Crude Steady But Oversupply Remains Key Concern

Oil prices haven’t been able to make up any of Tuesday’s losses. Crude is little changed helped by a marginal decline in the greenback with WTI at $72.29/bbl and Brent $77.22.

- Oversupply remains a key concern for the market with US crude exports expected to reach a record high and continued scepticism that OPEC’s output will be cut as announced last week.

- Bloomberg reported that US crude stocks rose 594k barrels in the latest week, according to people familiar with the API data. Gasoline rose 2.8mn and distillate 1.9mn. The official EIA data is released later today.

- Prices are down around 7% since OPEC but technical measures are suggesting that crude could be oversold and it may also be impacted by declining liquidity, according to Bloomberg. The Russians have been trying to support the market with Deputy PM Novak saying that OPEC could do more if last week’s decision is not enough to stabilise prices. He and President Putin will travel to Saudi Arabia and the UAE this week.

- Venezuela is posing further risks as it is granting licenses to extract oil in a disputed region of Guyana and has warned foreign oil companies to leave. It also hasn’t released US prisoners as agreed. Both actions risk the cancellation of licenses granted by the US in October.

- Ahead of Friday’s US payroll report, ADP employment prints today and is expected to be slightly higher at 130k. There are also the October trade balance and final Q3 productivity/ULC. The Bank of Canada meets and is expected to be on hold.

GOLD: Pullback From The All-Time High Continues

Gold is little changed in the Asia-Pac session, after closing 0.5% lower at $2019.36 on Tuesday.

- The firmer dollar weighed on precious metals, with spot gold extending the pullback from Monday’s fresh all-time high. Bullion has retraced some 5.5% since Monday’s intraday high of $2135.

- Tuesday’s softness came despite a decline in US Treasury yields following weaker-than-expected JOLTs job openings data. The decline in job openings was the biggest monthly drop since May 2023 and marked the lowest level since 2021. Moreover, the ratio of openings/unemployed dropped to 1.34, the lowest since August 2021. Lower rates tend to be positive for bullion, which doesn’t yield any interest.

- Later today the US calendar shows ADP private payrolls, ahead of Non-Farm Payrolls on Friday.

- While the overall price action signalled the potential for a climb towards 2177.58 next, a Fibonacci projection, recent price action conveys a short-term pullback, which should be considered corrective, according to MNI’s technicals team. Initial support is $2004.1, the 20-day EMA.

ASIA FX: Only Marginal Benefit From Higher Equities To Local FX

USD/Asia pairs are mixed. Tracking somewhat tight ranges, despite the positive equity tone in the region. Higher beta plays have underperformed gains seen in AUD and NZD. Still to come is Taiwan inflation data. Note tomorrow we get China trade figures, along with Thailand CPI data.

- USD/CNH sits near 7.1650 in recent dealings, slightly below Tuesday closing levels in the US. Onshore spot opened higher, but couldn't get beyond the 7.1600 handle. Headlines crossed from Rtrs around state bank selling of USDs again to keep depreciation pressures in the aftermath of the Moody's rating outlook change. Equity sentiment has improved modestly, amid share backs and broader gains in the region.

- USD/TWD sits just off session highs, last near 31.50. Late Nov lows in the pair coincided with a test of downside support at the 200-day MA (currently near 31.30), which held. Highs from the second half of Nov came in around 31.65, which is also close to the current 20-day EMA. We have only just returned to positive YTD inflows, so there may be upside momentum if tech related sentiment improves further. In turn this may cap USD/TWD upside. Working the other way is TWD's unappealing carry characteristics, TWD forward points (3 month) remain comfortably in negative territory, albeit up from recent lows). Note the US-TW2yr swap rate differential is back to +366bps, around multi month highs.

- The Rupee has opened dealing a touch above yesterday’s closing levels however ranges are narrow. Onshore participants are digesting yesterday's move lower in US Tsy Yields seen after a softer than forecast JOLTs report. USD/INR prints at 83.36/37. A reminder that yesterday S&P Global India Services PMI printed at 56.9, the lowest level since November 2022.

- USD/MYR continues to observe the narrow 4.63/70 range has persisted for the most part since early November, trading remains stable and moves have had little follow through. In early dealing today the pair is a touch higher and last prints at 4.6735/60. A reminder Fortnightly Foreign Reserves tomorrow provide the only data of note this week. There is no estimate and the prior read was $110.5bn.

- The SGD NEER (per Goldman Sachs estimates) is little changed this morning, we remain a touch off recent cycle highs and well within recent ranges. The measure sits ~0.3% below the top of the band. USD/SGD firmed above the $1.34 handle, ticking higher yesterday despite a fall in US Tsy Yields and a strong November PMI print as perhaps a weak Retail Sales print weighed on the SGD. On Wednesday we sit at $1.3405/10.

- USD/THB sits off recent highs, last near 35.14. Recent highs have come close to the 200-day EMA (35.275), although onshore markets were closed yesterday, which would have impacted liquidity. The low on Monday was 34.71, which is keeping THB implied vol high. The 1 month was last at 9.57%, fresh highs back to April of this year. The THB is the second worst performer in the EM Asia FX space over the past 5 sessions, down a little over 1%. (the won is the worst -1.85%). The continued underperformance of local stocks is a factor, the SET barely off recent lows (+0.18% today). Underwhelming economic growth hasn't helped sentiment in this space.

- USD/PHP is not too far off recent lows, last at 55.325. Lows on Monday were at 55.24, levels last seen in early August. We are seeing some modest PPH outperformance despite higher BBDXY levels, but the divergence is only modest at this stage. Peso bulls will target a move towards 55.00, while on the topside, recent highs have been between 55.55/60. Note the 20-day EMA is around 55.64.• PHP may be getting some support for positive seasonality. In 4 out the last 6 Dec, PHP has risen against the USD in Dec. This may reflect remittance related inflows.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/12/2023 | 0700/0800 | ** |  | DE | Manufacturing Orders |

| 06/12/2023 | 0830/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 06/12/2023 | 0930/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 06/12/2023 | 1000/1100 | ** | | EU | Retail Sales |

| 06/12/2023 | 1030/1030 | | UK | BOE FPC Summary and Record | |

| 06/12/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 06/12/2023 | 1315/0815 | *** | | US | ADP Employment Report |

| 06/12/2023 | 1330/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 06/12/2023 | 1330/0830 | ** | | US | Trade Balance |

| 06/12/2023 | 1330/0830 | ** | | US | Non-Farm Productivity (f) |

| 06/12/2023 | 1500/1000 | *** | | CA | Bank of Canada Policy Decision |

| 06/12/2023 | 1500/1000 | * | | CA | Ivey PMI |

| 06/12/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.