Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

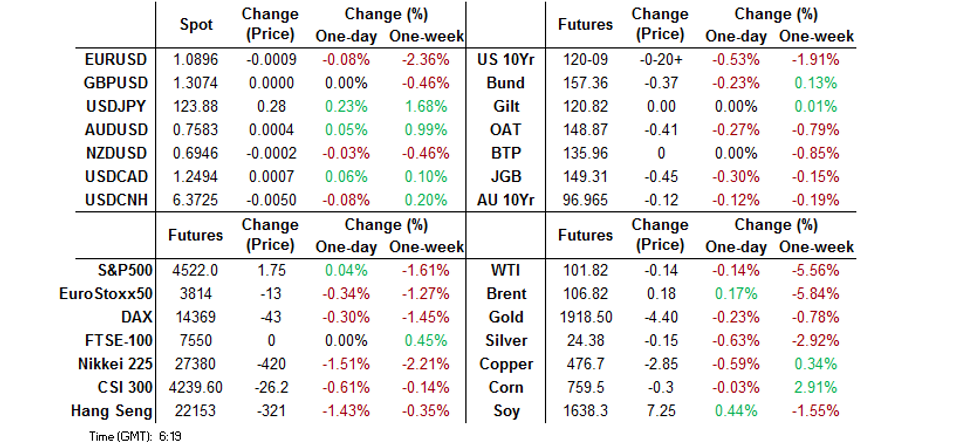

- Weakness in Core FI markets persists as the Asia-Pacific assess hawkish comments from Fed policymaker Lael Brainard, who called for a start to rapid balance sheet reduction as soon as next month. 10-Year ACGB yield surge to its highest point since 2015, while 10-Year JGB yield moves closer to the 0.25% official ceiling mandated by the BoJ.

- The yen goes offered as Brainard's comments served as a reminder of growing Fed/BoJ policy divergence. The greenback catches bid, with the DXY printing fresh cycle highs.

BOND SUMMARY: Core FI Crumble Under Pressure Of Hawkish Fed, BoJ Stays On Sidelines

Asia-Pacific reaction to Tuesday's hawkish Fedspeak resulted in continued selling pressure on core FI, with participants assessing remarks from FOMC's Brainard, who called for rapid balance-sheet reduction to start as soon as next month, a view later echoed by her Fed colleague Mary Daly. A bleak Caixin Services PMI reading failed to provide any support to the space, with markets in China, Hong Kong and Taiwan open again after a holiday-elongated weekend.

- T-Notes extended their rout to a fresh cycle low of 120-11. TYM2 still hovers just above there, last -0-16 at 120-13. Eurodollar futures run 1.5-11.0 ticks lower through the reds. Cash Tsy yields sit 5.1-7.0bp higher across the curve, with benchmark 10-Year yield running as high as to 2.616% at its peak. The minutes from the FOMC's March monetary policy meeting headline the local docket on Wednesday, with Fed's Harker due to discuss the economic outlook.

- It seemed like BoJ inaction vs. upward pressure on yields exacerbated JGB weakness, with futures posting a downtick after the Bank stayed on the sidelines despite earlier speculation re: potential for unscheduled bond purchases. JBM2 changes hands at 149.34, 42 ticks below last settlement and 2 ticks above session low. JGB yields pressed higher in cash Tokyo trade, with bear steepening evident amid particular weakness in the super-long end. The 10-Year yield targeted by the BoJ sits at 0.230%, not too far from the official cap of 0.250%.

- 10-Year ACGB yield surged to multi-year highs as Aussie bonds sold-off, extending the prior day's drop caused by a hawkish tilt in the RBA's rhetoric on interest rates outlook. Cash ACGB yields trade 8.2-12.7bp higher across the curve. Futures also slipped, with YM last -9.0 & XM -10.0. Bills run 6-18 ticks lower through the reds. The space paid little attention to an auction for ACGB May '30 as focus turns to a parliamentary testimony from RBA's Bullock & Kent.

FOREX: Fed's Brainard Cranks Up Hawkish Talk, Widening Policy Gap Saps Yen

The Asia-Pacific woke up to reports of hawkish comments from Fed policymaker Lael Brainard which rattled markets on Tuesday. As a reminder, she voiced support for starting a swift balance-book reduction as soon as next month. Regional headline flow failed to offer anything that could steal attention from Brainard, even as China, Hong Kong and Taiwan returned from holidays.

- Renewed awareness of a growing Fed/BoJ policy divergence pulled the rug from beneath yen, making it the worst G10 performer. Yesterday's remarks from BoJ Kuroda, who frowned upon "somewhat rapid" moves in the yen, failed to prevent the currency from losing ground. USD/JPY added ~30 pips and had a look above the Y124.00 mark, while its RSI moved further into overbought territory.

- The greenback garnered some strength amid a relentless upswing in U.S. Tsy yields. The DXY lodged its best levels since mid-2020.

- The Aussie dollar traded on a firmer footing as 10-Year ACGB yield surged to its highest point since 2015.

- In today's most awaited risk event, the FOMC will release the minutes from their March monetary policy meeting. German factory orders and comments from Fed's Harker, ECB's Lane & de Guindos, RBA's Bullock & Kent and Riksbank's Floden are also due.

FOREX OPTIONS: Expiries for Apr06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0935-55(E2.5bln), $1.1000(E1.1bln), $1.1035-41(E665mln)

- USD/JPY: Y121.00-10($670mln), Y121.75-80($752mln)

- USD/CAD: C$1.2500($598mln)

- USD/CNY: Cny6.4000($1.4bln)

ASIA FX: Hawkish Fedspeak Reverberates Across Asia, China's Caixin Services PMI Tumbles

Regional EM currencies suffered after hawkish Fed rhetoric pushed U.S. Tsy yields higher on Tuesday and into Wednesday's Asia-Pacific session, with markets in China, Hong Kong and Taiwan re-opening after a holiday. Continued spread of Covid-19 in China spoiled mood, especially after the latest Caixin PMI survey revealed its devastating impact on the local services sector.

- CNH: Offshore yuan knee-jerked lower in reaction to the release of Caixin Services PMI, with headline index plunging to 42.0, which represented the worst result since early 2020 and a significant miss of the median estimate of 49.7. The data provided evidence of sharp contraction in the sector, while Shanghai authorities announced a renewed mass testing drive coupled with continued lockdown. That said, spot USD/CNH gradually gave away all of its earlier gains.

- KRW: The won got battered amid firmer U.S. Tsy yields, which were pushed higher by Tuesday's comments from Fed's Brainard, who backed rapid balance sheet reduction from next month. Meanwhile, the BoK seems poised to hold the next monetary policy meeting without a Governor, as the nominee to take the bank's help will only attend his confirmatory hearing in parliament a few days later.

- IDR: The rupiah lost ground, with spot USD/IDR rising to a two-week high. Domestic headline flow was rather limited.

- MYR: Spot USD/MYR clawed back virtually all of its yesterday's losses, pushed higher by firmer U.S. Tsy yields.

- PHP: The peso was not spared from weakness and snapped its recent winning streak, with spot USD/PHP advancing after yesterday's rejection of support provided by its 100-DMA.

- THB: Onshore markets in Thailand were shut in observance of a public holiday.

EQUITIES: Lower As Fedspeak Spurs Caution

Most Asia-Pac equity indices are in the red at writing, following a negative lead from Wall St. Bearish spillover in the wake of Fed Gov Brainard’s hawkish comments on Tuesday was evident, with high-beta equities across the region struggling as U.S. Tsy yields have pushed higher in Asian hours.

- The Chinese CSI300 sits 0.5% worse off at typing, with a large miss in the Caixin Services PMI earlier in the session sending the index tumbling from neutral levels. The richly valued consumer staples sub-index struggled, while the large-cap ChiNext and tech-heavy STAR50 indices underperformed as well, with the latter duo dealing 1.3% and 2.3% softer respectively at writing.

- The Hang Seng trades 1.4% lower at typing, having pared losses from worst levels earlier in the session. China-based tech stocks underperformed, with the Hang Seng Tech Index dealing 3.2% weaker.

- Japan’s Nikkei 225 leads losses amongst regional peers, sitting 1.7% lower at typing. Tech-related stocks were mostly softer, while favoured names such as Tokyo Electron and Fast Retailing provided the most drag on the index. Elsewhere, financial and energy-related equities fared a little better, with limited gains observed in banking stocks.

- U.S. e-mini equity index futures sit flat to 0.2% worse off with NASDAQ contracts leading losses, each trading a touch above recently made one-week lows at typing.

GOLD: Flat As Fed Takes Focus

Gold is back from session lows to be virtually unchanged at writing, printing ~$1,924/oz. The precious metal has struggled to make headway above neutral levels as nominal U.S. Tsy yields have risen in Asian hours (with the 10-Year Tsy yield hitting levels last witnessed since Apr ‘19), continuing to operate around the bottom of Tuesday’s range.

- To recap, gold closed ~$9/oz lower on Tuesday as U.S. real yields and the USD (DXY) ticked higher, facilitated by hawkish comments from Fed Gov Brainard pointing to a “rapid pace” of Fed balance sheet reduction that could begin as soon as May.

- Looking ahead, focus will turn to comments on the economic outlook from the Fed’s Harker (1330 GMT), as well as the release of the FOMC’s March meeting minutes (1800 GMT).

- From a technical perspective, bullion remains range bound, while the outlook is bearish following the pullback from $2,070.4 (Mar 8 high). Key support is located at ~$1,906.6/oz (50-Day EMA), with further support at $1,895.3/oz. While both support levels were probed last week, a clear break lower would likely signal room for deeper moves lower. On the other hand, resistance is situated at $1,966.1/oz (Mar 24 high).

OIL: Flat As EU Sanctions Miss Russian Crude For Now

WTI and Brent are either side of unchanged at typing, having risen from session lows below neutral levels. Both benchmarks however operate around the lower end of Tuesday’s range as the impulse from expectations surrounding an EU embargo on Russian energy has weakened from earlier in the week.

- To elaborate, the bloc has announced a phased ban on Russian coal imports in their latest round of sanctions in response to alleged war crimes in Ukraine, missing expectations from some quarters for similar measures on Russian crude. EC President Ursula von der Leyen has since stated that members will continue working on ending imports of Russian oil and gas, with no timeline specified.

- Looking to China, concerns re: energy demand remain elevated as fresh COVID case counts nationwide for Apr 5 surged past 20K (both symptomatic and asymptomatic). Shanghai will remain under lockdown as the authorities announced another round of mass testing to begin on Wednesday, while transport ministry data reported late on Tuesday revealed that travel by road and air over the recent Qingming national holiday had declined by much more than expected as the country expands pandemic control measures in some areas.

- Elsewhere, some worry re: tightness in crude supplies was alleviated as weekly U.S. API inventory estimates crossed late on Tuesday. Reports pointed to a surprise build in U.S. crude stockpiles and increases in distillate and Cushing hub inventories, while there was a drawdown in gasoline inventories.

- Up next, U.S. EIA data is due later on Wednesday (1430 GMT), with WSJ estimates calling for declines in crude, gasoline, and distillate stockpiles.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/04/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Services PMI |

| 06/04/2022 | 0600/0800 | ** |  | DE | manufacturing orders |

| 06/04/2022 | 0700/0900 |  | EU | ECB VP de Guindos speaks | |

| 06/04/2022 | 0730/0930 | ** | | EU | IHS Markit Final Eurozone Construction PMI |

| 06/04/2022 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 06/04/2022 | 0900/1100 | ** | | EU | PPI |

| 06/04/2022 | 0900/1100 | | EU | ECB Schnabel Panel Moderation at ECB/EC Conference | |

| 06/04/2022 | 0900/1100 | | EU | ECB Exec Board member Fabio Panetta speech | |

| 06/04/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 06/04/2022 | 1145/1345 | | EU | ECB Philip Lane panel appearance | |

| 06/04/2022 | 1330/0930 | | US | Philadelphia Fed's Patrick Harker | |

| 06/04/2022 | 1400/1000 | * |  | CA | Ivey PMI |

| 06/04/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 06/04/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 06/04/2022 | 1800/1400 | * | | US | FOMC Minutes |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.