Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

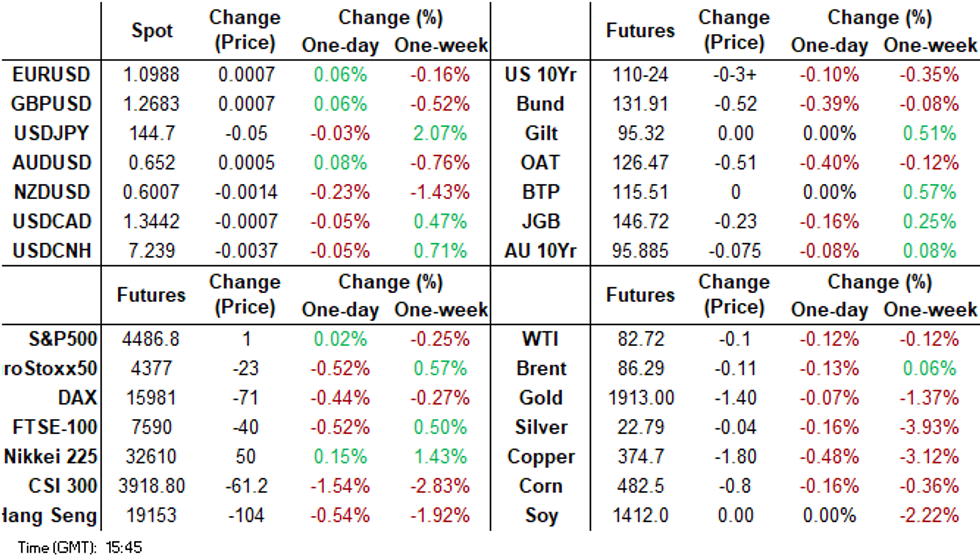

- The focus for China and Hong Kong markets remains property market sentiment and local government debt. Headlines crossed that China's Ministry of Finance will help shift $139bn of debt (or around 1 trillion yuan) from LGFVs to provinces. Provincial level governments will raise these funds through debt sales to repay debt of LGFVs. The initial market reaction was positive, but not large. China and HK equity indices remain down, albeit off session lows. USD/CNH is close to flat near 7.2400.

- Elsewhere, ACGBs (YM -6.0 & XM -7.5) are sitting at session lows. While the local session had RBA Governor Lowe’s appearance before Parliament, the market's direction appears more linked to the direction in US tsys from Thursday's NY session. TYU3 is trading at 110-23+, -04 from NY closing levels. With no headlines of significance and no cash tsy trading due to Japan’s observance of the Mountain Day public holiday, TYU3 dealings have been contained in a narrow range in the Asia-Pac session.

- FX moves have been muted in terms of the majors, although NZD/USD is threatening a downside test of 0.6000. Weaker PMI and food price data has weighed today. The market gives little chance for an RBNZ hike next week.

- Looking ahead, we get UK Q2 GDP printing, while in the US the July PPI and August U.of Mich sentiment readings are on tap.

MARKETS

US TSYS: Weaker, Narrow Range, No Cash Trading

TYU3 is trading at 110-23+, -04 from NY closing levels. With no headlines of significance and no cash tsy trading due to Japan’s observance of the Mountain Day public holiday, TYU3 dealings have been contained in a narrow range in the Asia-Pac session.

AUSSIE BONDS: Trading On A Weak Note, Wage Price Index On Tuesday

ACGBs (YM -6.0 & XM -7.5) are sitting at session lows. While the local session had RBA Governor Lowe’s appearance before Parliament, the market's direction appears more linked to the direction in US tsys, which are testing overnight lows in Asia-Pac trade.

- In his testimony, Governor Lowe highlighted household consumption and services inflation as the risks that will determine the policy path. These are familiar themes. Lowe added that the RBA is in watch-and-wait mode.

- Cash ACGBs are 5-7bp cheaper with the AU-US 10-year yield differential -2bp at +1bp.

- Swap rates are 4-6bp higher.

- The bills strip twist steepens with pricing flat to -6.

- RBA-dated OIS pricing is 1-3bp firmer across meetings.

- (AFR) Outgoing RBA governor Philip Lowe has urged policymakers not to succumb to the allure of quick fixes for the housing crisis, warning rent controls would make the shortage of homes even worse over the long term. (See link)

- Next week, the local calendar is uneventful on Monday. On Tuesday, attention turns to the CBA Household Spending data, setting the stage for the highly significant Wage Price Index scheduled for release on Wednesday and the Employment report on Thursday.

- The AOFM has announced plans to sell A$500mn of 2.75% 21 May 2041 bond on Wednesday.

NZGBS: Weaker, But Off Cheaps, Outperforms $-Bloc

NZGBs closed with a twist steepening of the 2/10 curve. Benchmarks were 1bp richer to 3bp cheaper. The short-end's move away from early session cheaps was aided by a soft Manufacturing PMI report that showed the index falling to 46.3 in July from a revised 47.4 in June. This was the lowest level since the gauge slumped to 39.0 in August 2021 during the Covid-19 pandemic. The long-term average is 52.9.

- The intraday short-end strengthening stood in stark contrast to the observed cheapening in US tsys and ACGBs, notably. Consequently, the yield differentials for the NZ-US and NZ-AU 10-year yield differentials contracted by 4bp.

- The swap curve also twist steepened with rates 2bp lower to 5bp higher.

- RBNZ dated OIS pricing closed 1-3bp softer across meetings.

- Food prices fell 0.5% m/m in July, with fruit and vegetable prices -4.1% m/m.

- Next week, the domestic calendar sees the Performance Services Index and Net Migration data on Monday, followed by REINZ House Prices on Tuesday. These precede the RBNZ Policy Decision on Wednesday. Bloomberg consensus is unanimous in expecting the OCR to be kept at 5.50%. The OIS market currently attaches an 8% chance of a 25bp hike.

EQUITIES: Japan Stocks Outperform Again, China Markets Down Despite LGFV Debt Relief

Regional equity indices are mixed as we approach the end of the week. Outside of Japan, most regional markets are again weaker. The early positive impetus to US equity futures also wasn't sustained. Eminis last track at 4484, down slightly for the session. Earlier highs were just above 4496.25. Nasdaq futures are still slightly higher, but well off intra-day highs.

- The focus for China and Hong Kong markets remains property market sentiment and local government debt. The HSI is down 0.62% at the break, which is up from lows, but only marginally. The HSTECH index is down by close to 1.90%.

- Not long before the break we had Bloomberg headlines cross that China's Ministry of Finance will help shift $139bn of debt (or around 1 trillion yuan) from LGFV to provinces. Provincial level governments will raise these funds through debt sales to repay debt of LGFVs. The initial market reaction was positive, but not large. Bloomberg notes this is a smaller than a similar scheme, which was launched in 2015, while it is also well below total LGFV debt estimates compiled by the IMF.

- On the mainland, the CSI 300 sits -1.38% lower at the break, with real estate sub-index at -0.43%, which is up from session lows, but still down for the week.

- Japan stocks are outperforming, the Topix and Nikkei 225 both up by 0.80-0.90%. Weaker yen levels and carry over from China recommencing tours to the country remain positives.

- The Kospi and Taiex are close to flat. In SEA Singapore shares are down over 1%. Weaker than expected Q2 GDP revisions have not helping sentiment.

FOREX: USD Can't Sustain Early Gains, NZD Underperforms

The BBDXY tracked higher in initial trade, as markets extended the USD's gains that came post the CPI print in Thursday NY trade. However, the BBDXY couldn't sustain a move above 1233.40, the index last around 1232.90, little changed for the session. Japan onshore markets have been closed today, which has meant no cash US Tsy trading. US bond futures have been range bound, unable to test late Thursday session lows. Equity futures opened higher, but are now back close to flat.

- USD/JPY attempted an early move towards 145.00 but this ran out of steam quickly, an option expiry later today in NY with a 145.00 strike may have been a factor. USD/JPY, last tracked around 144.65/70, slightly below Thursday closing levels in NY.

- NZD has underperformed at the margins. We had softer data on the manufacturing PMI front, which dipped further into contractionary territory (46.3), while food prices fell 0.5% m/m (the first fall since Feb 2022). The pair last tracked near 0.6010, but support appears evident ahead of the 0.6000 figure level, which is close to multi-month lows.

- AUD/USD was softer in early trade, but didn't test sub 0.6500. The pair was last 0.6520/25. RBA Governor Lowe testified before parliament, reiterating many previous well documented points. Household consumption, services inflation and the China slowdown are RBA watch points. AUD/NZD has tracked higher today, last near 1.0850.

- EUR/USD has been steady, unable to move back above the 1.1000 level.

- Looking ahead, we get UK Q2 GDP printing, while in the US the July PPI and August U.of Mich sentiment readings are on tap.

OIL: Little Changed In Asia-Pac After Giving Early Gains On Thursday

Oil is little changed in Asia-Pac trade after closing 1.8% lower on Thursday.

- After briefly pushing on to fresh YTD highs in London trading on Thursday, crude oil steadily moved lower both before and after US CPI and OPEC's MOMR, with Treasury sell-off and resumption of USD strength in the second half of the NY session adding a further headwind.

- Oil is on track to end the week little changed ahead of a report from the International Energy Agency that will provide a snapshot of a crude market that’s tightening due to supply curbs. Global markets are heading for a sharp supply deficit of more than 2 million barrels a day this quarter as Saudi Arabia slashes output, according to a monthly report from OPEC on Thursday. (See link)

- China’s inbound shipments of fuel oil fell from a record set in June as a local bottleneck eased and refiners received a fresh import quota. Imports declined to 330,000 barrels a day in July, down from June’s peak of 432,000 barrels a day. (See link)

GOLD: Little Changed After Less Dovish Fedspeak

Gold is slightly stronger in the Asia-Pac session, after closing marginally weaker at $1912.48 on Thursday. Bullion had initially spiked to $1930 after US CPI printed in line with expectations and initial jobless claims increased. However, that move proved to be short-lived as Fedspeak dampened optimism that easing inflation signalled the end of monetary tightening.

- Fed’s Daly (’24 voter) noted that the Fed still has more work to do and that the CPI data was largely as expected and that it doesn’t say ‘victory is ours’ on inflation. Daly added the Fed is yet to determine whether to raise and how long to hold rates, with Daly being data dependent and it premature to decide on another hike. There is a lot more info coming in before the September meeting and before year-end.

- Still, the Fed is looking increasingly likely to leave interest rates unchanged at its next meeting, with market participants having significantly pared bets on a September hike over recent weeks. The market currently attaches a 10% chance of a 25bp hike at the 20 September FOMC meeting.

ASIA FX: USD/CNH Steady Despite Equity Weakness, USD/KRW 1 Month Breaks Higher

A firmer bias has been evident in USD/Asia pairs today, but we generally sit away from session highs in latest dealings. USD/CNH sits close to 7.2400, little changed for the session, despite reports of LGFV debt relief. 1 month USD/KRW has broken higher. In SEA, IDR sits close to recent highs, while USD/SGD is finding selling interest above 1.3500. India CPI is out next Monday (IP is out later today), while we still await the China July aggregate credit figures.

- USD/CNH has traded a tight range. We got to 7.2340 not long after the firmer than expected CNY fixing. Equity sentiment has been weaker, despite further reports around LGFV debt relief and the regulators meeting with property developers. China equity indices are trying to claw back losses post the lunch time break, but remain comfortably in negative territory for now. USD/CNH was last near 7.2400.

- 1 month USD/KRW broke above 1320, but saw selling interest around 1322. We sit close to 1320 in latest dealings. Onshore equities are down a touch in terms of the Kospi. Earlier data showed the first 10-days of August export data still down around -15% in y/y terms.

- USD/SGD is still finding selling interest above 1.3500. The pair was last around 1.3485/90. The final Q2 GDP print came in a touch below expectations, at 0.1%, versus the projected 0.4%. Singapore avoided a technical recession, albeit just (Q1 growth was -0.4%). In y/y terms, growth was +0.5%, versus 0.8% expected. The government has revised down its 2023 growth forecast range to 0.5-1.5% from 0.5-2.5%.

- USD/IDR is back under 15220, right around the simple 200-day MA. We saw a very large net equity outflow from offshore investors yesterday, just under $1.2bn, the largest single daily outflow since end May 2005. Local equities have been largely tracking sideways in recent trade, the JCI under the 6900 level.

- USD/INR sits away from recent highs, last near 82.75, but has tracked sideways in early dealings today.

- USD/THB is holding above 35.00, last near 35.12. Earlier highs were close to 35.20. On the data front, consumer confidence edged down in July, back to 55.6 from 56.7 in June. This is the first downshift since the middle of last year.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/08/2023 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 11/08/2023 | 0600/0700 | ** | | UK | Index of Services |

| 11/08/2023 | 0600/0700 | *** | | UK | Index of Production |

| 11/08/2023 | 0600/0700 | ** | | UK | Trade Balance |

| 11/08/2023 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 11/08/2023 | 0600/0700 | *** | | UK | GDP First Estimate |

| 11/08/2023 | 0645/0845 | *** |  | FR | HICP (f) |

| 11/08/2023 | 0700/0900 | *** |  | ES | HICP (f) |

| 11/08/2023 | - | *** |  | CN | Money Supply |

| 11/08/2023 | - | *** | | CN | New Loans |

| 11/08/2023 | - | *** | | CN | Social Financing |

| 11/08/2023 | 1230/0830 | *** |  | US | PPI |

| 11/08/2023 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 11/08/2023 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.