Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Asia-Pac equity benchmarks and U.S. e-mini futures creep higher in overnight trade as market sentiment shows signs of recovery, despite a slew of escalating geopolitical risks. T-Notes stabilise after an initial upswing.

- The Australian dollar and short-end ACGB yields are pushed higher by hawkish revisions to RBA rate-hike calls, with Australian labour market data helping boost hawkish bets. Surge in AUD/NZD saps strength from the kiwi after the pair punches through technical resistance.

- The PBOC cut their 1-Year and 5-Year Loan Prime Rates by 10bp and 5bp respectively and set the USD/CNY mid-point at the lowest point since 2018. Offshore yuan edges higher, but its reaction is limited.

BOND SUMMARY: Broader Risk Recovery Outweighs Geopol Worry, Short-End ACGBs Go Offered On RBA Repricing

Core bond markets briefly showed some strength, which may have been linked to further complications on the geopolitical front. With tensions surrounding Russia's military activity near the Ukrainian border simmering in the background, North Korea hinted that it might resume testing intercontinental ballistic missiles (ICBM) and nuclear weapons. Core FI space gradually lost shine later into the session, as Asia Pac equity markets and U.S. e-mini futures crept higher.

- T-Notes rose to a session high of 127-20 before trimming gains and stabilising. TYH2 last trades -0-06+ at 127-15. Eurodollar futures trade 0.5-5.0 ticks lower through the reds. Bull flattening remains evident in U.S. Tsy curve, while yields have trimmed losses and last sit just 0.2-1.2bp lower. Weekly jobless claims, existing home sales & Philadelphia Fed Business Outlook take focus on the data front, with a 10-year Tsy auction also up today.

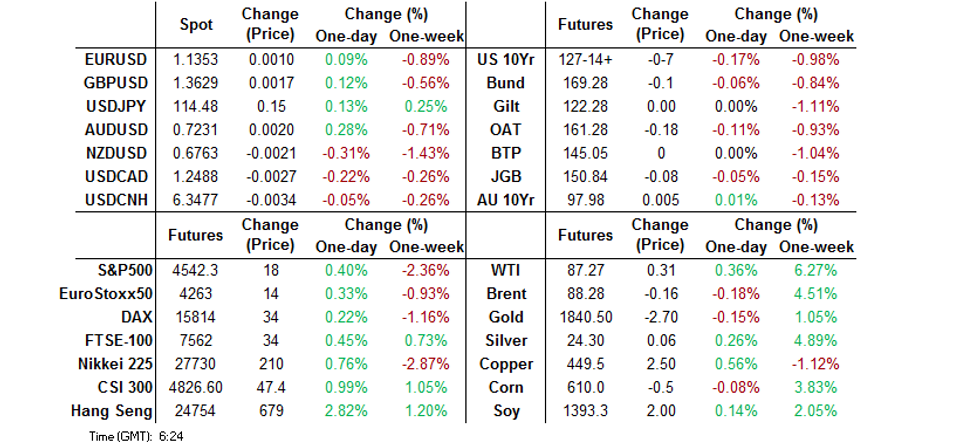

- Selling pressure hit short-end ACGBs after the release of strong Australian jobs data, which fanned expectations of an earlier withdrawal of stimulus by the RBA. The unemployment rate fell to a 13-year low of 4.2% in December from 4.6% prior, undershooting the median estimate of 4.5%. While the ABS highlighted that the survey was taken before a sharp spike in Covid-19 cases, the report fell on a fertile ground, as Westpac had earlier front-loaded their RBA rate-hike call. Although a subsequent spell of demand for core FI brought some reprieve to ACGBs, they resumed losses amid further hawkish RBA repricing. YM trades -3.0 as we type, with XM unch. at typing. Bills run +1 to -4 ticks through the reds. The weakness in short-end ACGBs drives flattening in cash curve, with yields last seen unch. to +3.2bp & 3-Year ACGBs taking the biggest hit. A note from Goldman Sachs may have added fuel to short-end ACGB sales, as they now expect the RBA to scrap new QE purchases this coming Feb (previously this May) and start raising the cash rate in May 2023 (previously Nov 2023).

- JGB futures posted a leg lower upon the re-opening of Tokyo markets. They staged a recovery attempt on the back of the aforementioned bid in core FI, but lost ground into the lunch break and after. JBH2 last trades at 150.88, 4 ticks below previous settlement. Cash JGB curve runs slightly steeper, as the super long end underperforms.

FOREX: AUD Surges On Strong Jobs Data, Leaves Antipodean Cousin Behind

A combination of strong labour market data released out of Australia and a hawkish change to the rate-hike call of an influential RBA watcher bolstered the Australian dollar, which still comfortably outperforms all G10 peers. Buying was triggered by the December jobs report, which showed that the unemployment rate undershot the expected level (4.5%) and fell to a 13-year low of 4.2%. Employment growth was slightly faster than forecast, while the participation rate stayed at 66.1%. The data came with a caveat, as the ABS noted that the survey was taken "was prior to the high number of COVID cases associated with the Omicron variant," but was enough to fuel hawkish RBA bets.

- Before the release of Australian jobs report, Westpac's Bill Evans said that he now expects Australia's central bank to deliver the first cash rate hike this coming August, which will be followed by another hike in October. Evans had earlier forecast the cash rate not being raised until February 2023.

- Trans-Tasman flows pushed AUD/NZD to within touching distance from the NZ$1.0700 mark. BBG trader sources suggested that buy-stops were triggered above resistance from Jan 5 high of NZ$1.0651. The swing in AUD/NZD sapped strength from the broader kiwi dolar and the flightless bird landed at the bottom of the G10 pile.

- Spot USD/CNH ground lower with all eyes on the PBOC. China's central bank cut their 1-Year & 5-Year Loan Prime Rates, which came after reductions to 1-Year MLF & 7-Day Reverse Repo rates delivered earlier this week. Meanwhile, the USD/CNY reference level was set at the lowest point since May 2018, which some interpreted as a sign of the PBOC's sense of comfort with redback appreciation.

- The DXY moved in tandem with U.S. Tsy yields, as both retreated in early trade only to gradually recoup the bulk of their losses. The initial weakness in U.S. Tsy yields dragged USD/JPY lower, but the yen went offered later in the session amid recovery in risk appetite. Worth noting that it is a Gotobi day in Japan, which may have contributed to eventual JPY weakness.

- U.S. weekly jobless claims, final EZ CPI, ECB Dec MonPol meeting minutes & Norges Bank MonPol decision take focus from here.

FOREX OPTIONS: Expiries for Jan20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250-65(E997mln), $1.1280-90(E1.1bln), $1.1300-15(E3.8bln), $1.1345-58(E2.2bln), $1.1400-10(E635mln), $1.1450(E1.1bln)

- USD/JPY: Y114.00-20($1.4bln), Y114.65-75($674mln)

- GBP/USD: $1.3750-70Gbp632mln)

- AUD/USD: $0.7260-70(A$526mln)

ASIA FX: KRW Loses Shine On North Korean Threat, PBOC Set USD/CNY Mid-Point At Multi-Year Low

Most USD/Asia crosses stayed in negative territory in the wake of yesterday's greenback sales, with monetary policy decisions from a couple of Southeast Asian central banks eyed today.

- CNH: Spot USD/CNH ground lower with all eyes on the PBOC. China's central bank trimmed 1-Year Loan Prime Rate by 10bp and 5-Year Loan Prime Rate by 5bp, which came after reductions to 1-Year MLF & 7-Day Reverse Repo rates earlier this week. Meanwhile, the PBOC set their USD/CNY reference rate at the lowest point since May 2018 and roughly in line with expectations, which some may have read as a sign that Chinese policymakers are comfortable with redback appreciation.

- KRW: South Korean won re-opened on a firmer footing but trimmed gains after North Korea (via its state media) delivered a veiled threat to lift the self-imposed moratorium on ICBM & nuclear weapons tests. Yonhap later reported that North Korea appears to be preparing a military parade.

- IDR: The rupiah was stable, with participants on the lookout for monetary policy decision from Bank Indonesia. The central bank is expected to keep their main policy rate unchanged, but their language will be closely watched.

- MYR: Bank Negara Malaysia are also set to deliver a monetary policy decision, and are also expected to stand pat. The ringgit garnered some strength in the lead-up to the announcement, even as FinMin Zafrul told parliament that recent flooding may cost the economy as much as $1.9bn.

- PHP: Spot USD/PHP continued to operate close to a fresh cycle high printed yesterday, slowly moving away from that level. The Philippines' daily cases remained on downward trajectory.

- THB: Spot USD/THB was clawing back initial losses, before it sold off again as Thailand's Covid-19 task force approved the easing of some restrictions and the resumption of the "Test & Go" travel programme Feb 1 for travellers of all nationalities.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/01/2022 | 0700/0800 | ** |  | DE | PPI |

| 20/01/2022 | 0745/0845 | ** |  | FR | Manufacturing Sentiment |

| 20/01/2022 | 0900/1000 | *** |  | NO | Norges Bank Rate Decision |

| 20/01/2022 | 1000/1100 | *** |  | EU | HICP (f) |

| 20/01/2022 | 1100/0600 | * |  | TR | Turkey Benchmark Rate |

| 20/01/2022 | 1230/1330 | | EU | ECB publishes Dec meet accounts | |

| 20/01/2022 | 1330/0830 | ** |  | US | Jobless Claims |

| 20/01/2022 | 1330/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 20/01/2022 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 20/01/2022 | 1500/1000 | *** | | US | NAR existing home sales |

| 20/01/2022 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 20/01/2022 | 1600/1100 | ** | | US | DOE weekly crude oil stocks |

| 20/01/2022 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 20/01/2022 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 20/01/2022 | 1800/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

| 21/01/2022 | 2330/0830 | *** |  | JP | CPI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.