Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

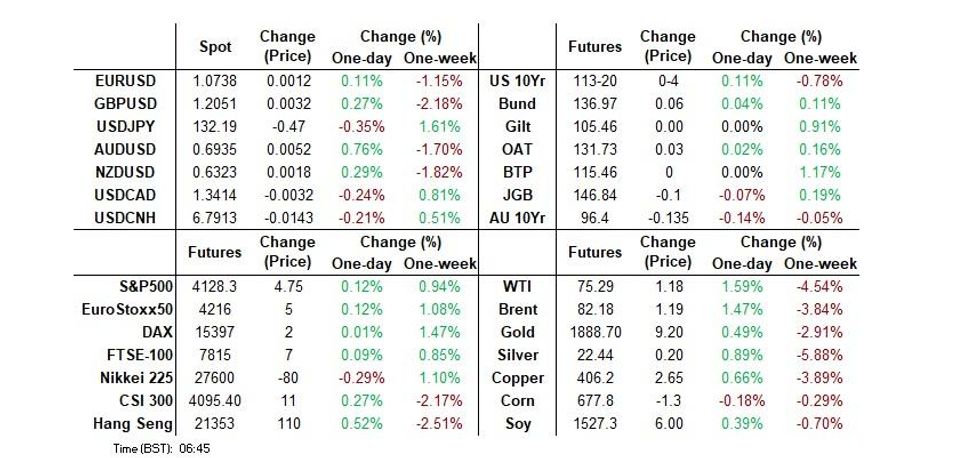

- AUD outperformed in G10 FX trade as RBA terminal cash rate pricing shifted higher after the RBA board delivered the expected 25bp hike, while pointing to further rate hikes in the months ahead.

- Asia-Pac equities have traded in a mixed fashion.

- German industrial production data headlines a thin data slate, while Fed Chair Powell heads up a raft of speakers from the major global central banks.

US TSYS: Richer In Asia, Powell In Focus

TYH3 deals at 113-19+, +0-03+, a touch off the top of its 0-09+ range on volume of ~139K.

- Cash Tsys sit 1-5 bps richer across the major benchmarks, the curve has bull steepened.

- Participants faded Monday's leg of post-NFP cheapening in early Asia-Pac dealing after frenetic moves in recent sessions.

- The richening held through the Asian session.

- A couple of block buys in TU futures (+3.5K & +5.5K) aided the bid.

- Tsys looked through weakness in ACGBs as the RBA raised rates 25bps. The accompanying hawkish guidance noted that rates will need to rise further and more than once.

- The U.S. trade balance headlines an otherwise thin data slate today. More widely, Fed Chair Powell provides the macro highlight in his first remarks since last week's Fed meeting. 3-Year Tsy supply is also due.

JGBS: Futures Off Lows, 30-Year Auction Aids Twist Steepening

JGB futures recouped the losses incurred during the early break through their overnight session base, with the initial move lower presumably triggered by the firmer than expected wage data flagged earlier and Tokyo reaction to Monday’s weakening in core global FI markets. Futures are -10 into the close, while cash JGBs are 1bp richer to 1bp cheaper, pivoting around 30s.

- BoJ matters continue to dominate with Finance Minister Suzuki being the latest Cabinet level official to explicitly push back against the idea that BoJ Deputy Governor Amamiya has been tapped to succeed outgoing Governor Kuroda. Meanwhile, Chief Cabinet Secretary Matsuno noted that the timing and method of BoJ appointments are a matter for the Diet.

- Elsewhere, we saw comments surrounding last year’s intervention in FX markets on the part of the Japanese government, but there was little new information provided alongside the data, with Finance Minister Suzuki reiterating well-trodden rhetoric surrounding the FX market.

- The low price at the latest round of 30-Year JGB supply just missed expectations, while the price tail widened a touch even as the cover ratio pushed above the 6-auction average. It would seem that the relative richness vs. other super-long benchmarks and continued uncertainty re: BoJ policy post-Kuroda was enough to disincentivise some prospective bidders, albeit with prevailing yield levels proving enough to generate a baseline level of demand. 30+-Year paper struggled post auction, resulting in the aforementioned twist steepening.

- BoJ Rinban operations covering 1 to 25-Year JGBs headline domestically on Wednesday.

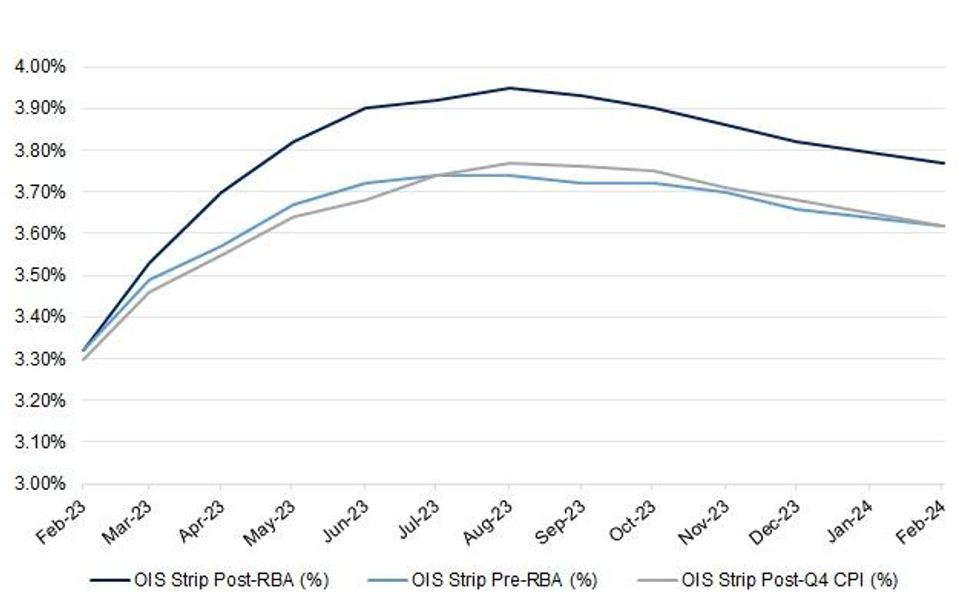

AUSSIE BONDS: Bear Flattening After RBA Points To Multiple Hikes

Aussie bonds were pressured after the RBA board delivered the expected 25bp hike, while pointing to further rate hikes in the months ahead (we place emphasis on the plural in future hikes). Terminal cash rate pricing has shifted above 3.90% to reflect this, after printing around 3.75% pre-decision.

- The Bank also tipped its hat to firm domestic demand resulting in more meaningful inflationary pressure, albeit while providing a sense of increased worry re: the health of some households (alongside some firmer language against the risks of a de-anchoring of inflation expectations, although it reaffirmed that expectations remain well anchored at present).

- The Bank didn’t allude to its updated underlying inflation forecasts (which will be published on Friday), while it only expects headline inflation to return to the upper end of the target range in ’25.

- Aussie bond futures breached their early session lows on the move, after firming off their early Sydney lows ahead of the RBA decision. YM finished -16.0, while XM was -13.5, a touch off their respective post-decision bases, while wider cash ACGBS sit 7.5-15.5bp cheaper as the curve bear flattens, reflecting the pricing of more aggressive RBA tightening near-term.

- The AU/U.S. 10-Year yield spread widened post-RBA, pushing out by half a dozen bp on the day to ~-2bp, briefly testing above parity.

- A$1.0bn of ACGB Nov-33 supply headlines domestically on Wednesday.

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

NZGBS: Off Cheaps After Long Weekend Catch Up, RBA To Impact On Wednesday

NZGBs finished off cheapest levels on Tuesday, with the initial post-long weekend move reflecting the weakness observed in global core FI markets in lieu of Friday’s firmer than expected U.S. economic data, as well as reaction to the latest rounds of Fed, ECB & BoE speak. Still, core global FI found a bit of a base in the early rounds of wider Asia-Pac dealing, which allowed NZGBs to finish 14-17bp cheaper across the curve, with bear flattening in play. The local close came before the latest RBA decision across the Tasman, which pressured ACGBs, a move likely to be reflected in NZGBs come tomorrow’s local open (new flow & wide market-dependent).

- Swap rates were 16-17bp higher in a parallel shift, also finishing off session extremes, leaving swap spreads flat to wider on the day.

- RBNZ-dated OIS indicates ~55bp of tightening for this month’s decision, alongside a terminal OCR of ~5.25%, higher vs. Friday’s closing levels in lieu of the repricing of global central bank expectations witnessed in that window. Once again, these marks will likely be adjusted higher in reaction to the RBA decision during early Wednesday trade.

- There wasn’t much in the way of meaningful domestic headline flow to trade off, which left post-weekend adjustments at the fore.

- Looking ahead, there is nothing of note on the local docket on Wednesday.

FOREX: AUD Outperforming After RBA Hikes 25bps & Flags More Hikes To Come

AUD is the strongest performer in the G-10 space at the margins, with the greenback moderately weaker as its gives back some post NFP gains.

- AUD/USD prints at $0.6925/30 ~0.7% firmer, the pair was up as much as 1% in the aftermath of the RBA decision. The central bank raised the cash rate 25bps and noted in its statement that rates will need to rise further and more than once. Earlier the Dec trade balance had printed a touch below expectations.

- USD/JPY is ~0.3% softer, last printing ¥132.25/35. The 20-day EMA at 130.34 is the next downside target. Dec Labour Cash Earning rose 4.8% vs 2.5% exp, Dec Real Cash Earning were also on the wires printing at 0.1% vs -1.5% exp. Jan Household spending fell 1.3% more than the exp -0.4%. Dec, P Coincident Index printed in line with expectations

- NZD is also firmer, last printing $0.6320/25. The pair met resistance above its 50-day EMA, paring gains to sit at current levels. Jan ANZ Commodity Prices fell 1%, the prior read was -0.1%.

- EUR/USD and GBP/USD are both marginally firmer, with the moderate weakness in the USD boosting the pairs.

- Cross-asset flows see e-minis up ~0.1%, although off session highs, and BBDXY down ~0.1%.

- US Trade Balance, which headlines an otherwise thin data slate. Fed Chair Powell speaks today for the first time since last week's Fed meeting.

FX OPTIONS: Expiries for Feb07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0600(E829mln), $1.0700-20(E816mln) $1.0800(E1.3bln), $1.0830-50(E1.6bln), $1.0890-00(E1.1bln), $1.0990-00(E1.2bln)

- USD/JPY: Y130.00($1.1bln), Y133.50($500mln)

- GBP/USD: $1.1900-25(Gbp588mln)

- EUR/GBP: Gbp0.8850-70(E1.2bln)

ASIA FX: North East Asia FX Firms, But PHP & MYR Underperform

A number of USD/Asia pairs are lower, although there hasn't been a great deal of follow through. There were also some exceptions, with USD/PHP and USD/MYR both pressing higher. USD/CNH sits close to 6.7920 currently, down slightly for the session. We are still waiting for China FX reserves data, along with Taiwan for Jan trade figures. Tomorrow is headlined by the RBI decision, +25bps expected.

- USD/CNH is has again found support around the 6.7800 level, with the pair last around 6.7915/20. The CNY fixing was actually weaker relative to expectations, reversing relative to yesterday's trend. Onshore equities are higher, but only modestly.

- 1 month USD/KRW got to the low 1250 region, but found support around this level and pushed back to 1255/56 currently. Onshore equities are higher 0.50%, with offshore investors adding +$134.1mn. Local officials will meet with FTSE/Russell officials tomorrow to push Korea's case for WGBI inclusion.

- The SGD NEER (per Goldman Sachs estimates) is moderately firmer this morning, the measure has eased recently as broad based USD strength has been present in the wake of a strong NFP print last week. NEER sits ~0.7% below the upper end of the band at present levels. USD/SGD is ~0.1% softer today, last dealing $1.3260/70, the pair is at its highest level since Jan 11. The pair has risen ~2% off lows seen last week. Whilst technicals remain bearish for USD/SGD, the tide may be turning. The pair has held above its 20-day EMA (1.3217) in recent trade. Bulls target the 50-day EMA at $1.3381. Bears first look to break 2023 lows at $1.3032.

- USD/PHP is tracking higher today. The pair last around 54.925, +0.950% above closing levels for yesterday. This coincides with earlier Jan highs, with the 55.00 level also approaching. The 20-day EMA, around 54.60 has been breached, which the 50-day EMA sitting higher at 55.33. This morning's Jan inflation surprise, +8.7% y/y, versus 7.6% expected, suggests the BSP clearly has more work to do. The forecast range was 5.4-8.0%, while core inflation rose to 7.4% y/y, from 6.9% in Jan. The next BSP meeting is Feb 16, with the central bank stating recently that it will take all necessary actions to bring down inflation.

- USD/MYR is back above 4.3000, +0.90% on last closing levels, although onshore markets were closed yesterday, so some of this reflects catch up. IP figures were weaker than expected at +3.0% y/y, versus 4.2% forecast. Mid Jan highs in USD/MYR come in around 4.3400.

ASIA: Mixed Inflation Picture To Result In Varying Central Bank Actions

CPI data for January has so far been mixed in Asia. Thailand and Indonesia saw a moderation in both core and headline whereas Korea and the Philippines saw them rise. This is likely that non-Japan Asian inflation ex China was stable around 5.4% in January but the core may have ticked up to 4.2%.

- Korean headline inflation rose to 5.2% y/y, the first increase since October due to electricity tariffs, but still well off its July peak of 6.3%. Core inflation rose to 5.0% y/y from 4.8% The BoK focuses on underlying inflation and while they are unlikely to be happy with the rise in core, ex utilities it was unchanged at 4.1%.

- Indonesian inflation eased to 5.3% y/y from 5.5%after peaking at 6% in September. Core, which Bank Indonesia is focusing on, eased back to 3.3% from 3.4% the previous month. The moderation in inflation was driven by lower fuel prices, which also resulted in a drop in administered price inflation. Supply side reforms are also helping to keep inflation contained. After 225bp of tightening this cycle, the January CPI data maybe enough for BI to pause.

- Inflation in Thailand also eased in January to 5% y/y from 5.9% and underlying to 3% from 3.2%, indicating that the recovery isn’t creating unmanageable price pressures. Base effects should keep core inflation down but the Bank of Thailand is likely to continue its gradual tightening given the expected tourism rebound.

- Inflation in the Philippines significantly exceeded expectations in January and rose to 8.7% y/y from 8.1%. Core was also higher at 7.4% from 6.9%, the highest since 1999. The central bank has tightened by 350bp this cycle and though the impact is expected to be felt on prices this year, the spread of inflation is likely to result in further hikes.

Source: MNI - Market News/Refinitiv

MNI RBI Preview - February 2023: +25bps Expected, But Will Stance Be Shifted To Neutral?

EXECUTIVE SUMMARY

- The RBI is expected to deliver a 25bps hike at tomorrow’s policy meeting. This is the consensus from economists surveyed by Bloomberg, although a small number of forecasters expect the RBI to remain on hold. If a 25bps hike is delivered, which is also our expectation, then this would take the policy rate to 6.50%.

- A case could be made for no change, given the likely headline CPI trajectory and the potential for the RBI to revise down its inflation outlook (6.7% is the projection for the current financial year, ending March 31). Still, an important offset comes from sticky core inflation pressures. So, whilst the real policy rate, against headline inflation is trending back into positive territory, against core inflation, it will only just be in positive territory.

- The other focus point from the meeting is likely to RBI’s policy stance. There is a general consensus that ‘withdrawal of accommodation’ will be replaced with something more akin to ‘neutral’. A shift to neutral language around the stance of policy would leave the market expecting a pause in the tightening cycle at the next meeting and the RBI becoming more data dependent around future shifts. We would note though this is not a consensus market viewpoint, with some forecasters still expecting 'withdrawal of accommodation' to be maintained in terms of RBI language.

- Full preview here:

EQUITIES: China/HK Equities Edge Higher, Mixed Trends Elsewhere

Regional equities have traded in a mixed fashion today. US futures are higher, albeit away from best levels. Eminis last around +0.10%, Nasdaq futures +0.14%. This follows falls during Monday trade for the major US bourses.

- China/HK equities are higher. The HSI is up 0.84% to the break, with the tech sub index around +2% at this stage. while the CSI is +0.34% at this stage. Sentiment has been lifted in the developer space, as Wuhan lifted home purchase curbs.

- Housing remains the missing link in terms of the China rebound story in 2023. Bloomberg notes the easing of curbs in Wuhan (on housing purchases) could pave the way for other cities to follow suit (see this link for more details).

- The tone elsewhere is more mixed. The Nikkei 225 is close to flat, while earlier wages data came in stronger than expected with real wages back in positive territory.

- The Kospi is up 0.60%, while the Taiex is also firmer (+0.20%), despite the negative tech lead from Monday's session.

- The ASX 200 is down -0.55%, with a hawkish RBA 25bps hike likely weighing at the margin. SEA equity indices are mostly lower, with Indonesian stocks the exception (+0.87%).

GOLD: Bullion Awaiting Fed Powell’s Comments

Gold prices range traded on Monday after falling sharply in the wake of the strong US payrolls data. They are up 0.3% during today’s APAC session to around $1872.30/oz, close to the intraday high of $1875.67. This has been helped by a slightly weaker USD (DXY -0.1%).

- Bullion has traded today above support at $1861.40, the post-payroll/ISM low. Resistance remains at $1903.40, the 20-day EMA.

- Later Fed Chairman Powell speaks, which could influence gold prices as the market looks for direction on the rate outlook. A more hawkish tone would be negative for zero-yielding gold. On the data front there is US December trade data and January NFIB business optimism.

OIL: Crude Stronger On Improved Demand Optimism And Supply Outages

Oil has been trading in a tight range during today’s APAC session. WTI is up 1% to $74.90, close to the intraday high of $74.98 and Brent is up 1% to $81.80, just below the high of $81.84. The market has been more positive today after Saudi Arabia signalled confidence in the demand outlook and reports of supply outages.

- Saudi Aramco, Saudi Arabia’s public energy company, increased prices for mainly the Asian market in March reflecting its optimism in the demand outlook.

- On the supply side, the pipeline from Kurdish oil fields in Iraq that goes through Turkey has been closed due to Monday’s earthquake. Usually 450kbd goes through that pipeline. Turkey also stopped flows to the Ceyhan export terminal. In addition, there was a power outage at a large Norwegian field.

- In January, Russia saw a 46% drop in oil and gas revenues, putting pressure on the government deficit. This was due to a drop in the price of Urals blend and in natural gas exports. The market is still watching for the impact of the latest sanctions on Russian supply.

- Later Fed Chairman Powell speaks, which could be important for direction on the rate outlook. On the data front there is US December trade data and January NFIB business optimism. There is also US API inventory data released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/02/2023 | 0645/0745 | ** |  | CH | Unemployment |

| 07/02/2023 | 0700/0800 | ** |  | DE | Industrial Production |

| 07/02/2023 | 0745/0845 | * |  | FR | Foreign Trade |

| 07/02/2023 | 0800/0900 | ** |  | ES | Industrial Production |

| 07/02/2023 | 0900/0900 |  | UK | BOE Ramsden Intro at UK Women in Economics Event | |

| 07/02/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 07/02/2023 | 1015/1015 | | UK | BOE Pill Chairs UK Women in Economics Panel | |

| 07/02/2023 | 1330/0830 | ** |  | US | Trade Balance |

| 07/02/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 07/02/2023 | 1430/1430 | | UK | BOE Cunliffe Speech at UK Finance | |

| 07/02/2023 | 1500/1000 | ** | | US | IBD/TIPP Optimism Index |

| 07/02/2023 | 1700/1800 |  | EU | ECB Schnabel in Finanzwende e.V. Webinar | |

| 07/02/2023 | 1730/1230 |  | CA | BOC Governor Macklem speech/press conference in Quebec City | |

| 07/02/2023 | 1740/1240 | | US | Fed Chair Jerome Powell | |

| 07/02/2023 | 1800/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 07/02/2023 | 1900/1400 | | US | Fed Vice Chair Michael Barr | |

| 07/02/2023 | 2000/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.