Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

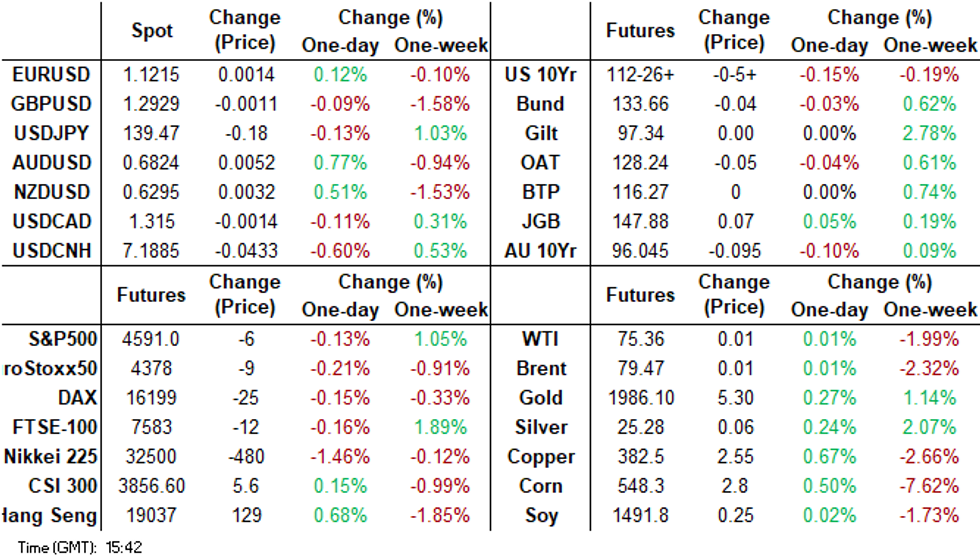

- Australian June employment came in stronger than expected. RBA dated OIS pricing shifts 4-9bp firmer across meetings after the data. A 56% chance of a 25bp hike is now priced for August versus 40% before the data. AUD/USD is back above 0.6800, the best performer in the G10 space.

- Elsewhere, the defence of the yuan picked up. The CNY fixing was the strongest (relative to expectations) since November 2022, while macroprudential rules were shifted to enable onshore firms' greater access to offshore capital. Bloomberg also reported the authorities are considered easing mortgage restrictions. USD/CNH got close to 7.1750 before rebounding.

- In Europe today German PPI provide the highlight. Further out we have Initial Jobless Claims, Home Sales and Philadelphia Fed Business Outlook. We also have the latest 10-Year TIPS supply.

MARKETS

GLOBAL: APAC Countries To Be Concerned By Softer China Outlook

MNI (Australia) - China data have been surprising to the downside in recent months and there has been increasing discussion of a disappointing economic recovery. This has impacted oil market sentiment, as China is the largest oil importer, and numerous countries in APAC have begun to discuss the potential impact on their growth outlook from a slower China. Some countries will be impacted more than others.

- Exports to China for most countries in the APAC region are important to the total. In 2022 Australia was the top of the list with 29.1% of exports going to China but NZ, Taiwan, Indonesia and South Korea all have more than 20%. In contrast, India only has 3.5% of its shipments destined for China. Major OECD nations such as the US and euro area only have a minor exposure.

- These figures don’t tell the whole story regarding the impact of slower China growth. In terms of GDP, Taiwan and Malaysia are the most exposed, whereas Australia’s economy is only slightly more exposed to its exports to China than Thailand’s and less than Korea’s. But many APAC countries are likely to be concerned about slower China demand.

Source: MNI - Market News/Refinitiv

US TSYS: Marginally Cheaper In Asia

TYU3 deals at 112-27, -0-05, a 0-06 range has been observed on volume of ~46k.

- Cash tsys sits 0.5-1.5bps cheaper across the major benchmarks, the curve has bear steepened.

- Tsys were pressured after spillover from ACGBs, the Australian Unemployment Rate held steady at 3.5% in June after the May figure was revised lower.

- The move did not follow through and tsys pared losses. Narrow ranges were observed for the remainder of the session as little meaningful macro news flow crossed.

- FOMC Dated OIS remain stable; ~25bps of hikes are priced into next weeks meeting. A terminal rate of 5.40% is seen in November with ~70bps of cuts by June 2024.

- In Europe today German PPI provide the highlight. Further out we have Initial Jobless Claims, Home Sales and Philadelphia Fed Business Outlook. We also have the latest 10-Year TIPS supply.

JGBS: Futures Holding Richer, Narrow Range, June National CPI Tomorrow

In the Tokyo afternoon session, JGB futures are holding firmer, +12 compared to the settlement levels, after trading in a relatively narrow range.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined trade balance data that surprisingly printed a trade surplus.

- Accordingly, local participants have likely been on headlines and US tsys watch.

- Cash tsys sit 0.5-1.5bps cheaper across the major benchmarks, with the curve steeper. US tsys appear to have been pressured by spillover from ACGBs after the Australian unemployment rate held steady at 3.5% in June. However, the move did not follow through and tsys pared losses. Narrow ranges were observed for the remainder of the session as little meaningful macro news flow crossed.

- The cash JGB curve bull flattened in the afternoon session with yields 0.3bp to 4.0bp lower (40-year) The benchmark 10-year yield is 0.7bp lower at 0.459%, below BoJ's YCC limit of 0.50%.

- The swaps curve has also bull flattened with swap spreads tighter out to the 10-year and wider beyond.

- Later today the local calendar sees June data for Machine Tool Orders (Final).

- Tomorrow the local calendar releases National CPI data for June and International Investment Flows (July 14).

- Tomorrow the MoF will also conduct a Y500bn Liquidity Enhancement Auction for OTR 5-15.5-year JGBs.

AUSSIE BONDS: Holding Sharply Cheaper After Employment Data Beat

ACGBs (YM -12.0 & XM -9.5) are holding weaker after an upside surprise in the June employment report.

- June employment came in stronger than expected but below the upper end of forecasts. The economy added 32.6k new jobs after an upwardly revised 76.5k in May. The unemployment rate was steady at 3.5% after May was revised down from 3.6%. Full-time jobs and hours worked rose.

- As the labour market remains very tight, Q2 inflation due July 26 will likely need to be down significantly including services for another RBA pause in August.

- Cash ACGBs are 4-7bp cheaper after the data with the 3/10 curve 3bp flatter. The AU-US 10-year yield differential +6bp on the day at +20bp.

- Swap rates are 9-12bp higher on the day, 4-7bp higher after the data.

- The bills strip bear steepens with pricing -8 to -13.

- RBA dated OIS pricing shifts 4-9bp firmer across meetings after the data. A 56% chance of a 25bp hike is now priced for August versus 40% before the data.

- Tomorrow the local calendar sees no data releases.

- In Europe today German PPI provide the highlight. Further out we have Initial Jobless Claims, Home Sales and Philadelphia Fed Business Outlook. We also have the latest 10-Year TIPS supply.

AUSTRALIAN DATA: Labour Market Still “Very Tight”, August Hike On Cards

June employment came in stronger-than-expected but below the upper end of forecasts. The economy added 32.6k new jobs after an upwardly-revised 76.5k in May. The unemployment rate was steady at 3.5% after May was revised down from 3.6%. Full-time jobs and hours worked rose. As the labour market remains very tight, Q2 inflation due July 26 will likely need to be down significantly including services for another RBA pause in August.

- The May unemployment rate was revised down 0.004pp which rounded was to 3.5% from 3.6%. June was 0.08pp below May at 3.47% driven by jobs growth and a 10.9k drop in the number of unemployed. The participation rate fell 0.1pp to 66.8%.

- The trend of rising full-time (FT) jobs with falling part-time (PT) continued and along with the increase in hours worked is pointing to persistent labour shortages despite a 2.9% y/y increase in the labour force. FT employment rose 39.3k to be up 4% y/y and PT fell 6.8k to be up only 0.7% y/y. 3-month momentum remains robust for total and FT employment.

- Hours worked rose 0.3% m/m to be up 4.7% y/y, exceeding the growth in jobs at 3% y/y, as existing employees meet some of the demand. FT hours rose 0.8% m/m & 5.6% y/y while PT fell 2% m/m to be up only 0.4% y/y. Weaker PT hours may reflect the increase in the underemployment rate from its February trough. In June it was stable at 6.4%, which while low historically, is up from the 5.8% low.

- The growth in population over 15yrs continued to rise to new historical highs at 2.8% y/y up from 2.7%. The employment-to-population ratio remained at the record 64.5%.

Source: MNI - Market News/ABS

AUSTRALIAN DATA: RBA Indicators Signal Labour Market Adding To Price Pressures

In June, Deputy Governor Bullock spoke about the labour market and pointed out that the NAIRU was estimated to be around 4.5% and thus the current labour market situation is inflationary. The labour market remains “very tight”. Bullock also pointed out four labour market indicators that the RBA is watching closely. Today we got updates for three of them and they suggest little change in the labour market.

- The unemployment rate was 3.5% in both May and June, thus 1pp below the NAIRU. See MNI Labour Market Still Very Tight, August Hike On Cards for details. An increase in jobs and a drop in the number of unemployed saw it fall to 2 decimal places.

- The underemployment rate was steady in June at 6.4%, which is 0.4pp above the February low but still 2.1pp below the pre-pandemic January 2020 rate. Full-time employees are working more hours but this trend is less pronounced for part-timers.

Source: MNI - Market News/ABS

- The RBA also looks at the quarterly ratio of vacancies to unemployment. Q2 unemployed rose 0.5% q/q, which was less than Q1, but vacancies fell 2% q/q. The ratio eased further to 83.5 in Q2 from 85.7, off its Q3 2022 peak of 91.9 but it is still significantly higher than pre Covid and signalling that there is just under one vacancy per job seeker.

Source: MNI - Market News/ABS/Refinitiv

NZGBS: Short-End Closed On A Negative Note, 10Y Weaker But Off Cheaps

Short-end NZGBs closed on a weak note with the 2-year benchmark yield 9bp cheaper. The 10-year benchmark was also 4bp weaker on the day but finished off session cheaps after this week’s supply saw solid demand for the Apr-37 line (cover ratio of 3.16x). The line was 2.0bp richer in post-auction trade. The bid was less enthusiastic for the May-28 and May-32 lines with cover ratios of 2.68x and 2.36x respectively. Nonetheless, the lines were 1-1.5bp lower in post-auction trading.

- In the absence of domestic data, the local market seems to have been affected negatively by the post-employment data reaction in ACGBs. Furthermore, given the somewhat concerning Q2 core CPI print from yesterday, there is a possibility of follow-through selling in the market.

- Swap rates are 5-8bphigher with the 2s10s curve flatter and implied long-end swap spreads wider.

- RBNZ dated OIS pricing is 1-5bp firmer across meetings beyond October. Terminal OCR expectations sit at 5.70%, the highest since early July.

- The local calendar has no data tomorrow with the next data release on note being Trade Balance data on Monday.

- Later today, the US calendar delivers Weekly Jobless Claims Data along with the July Philly Fed and June Existing Homes Sales.

FOREX: AUD Firms As Unemployment Rate Falls

AUD is the strongest performer in the G-10 space at the margins on Thursday in the Asian session. The economy added 32.6k new jobs in June after an upwardly-revised 76.5k in May. The unemployment rate was steady at 3.5% after May was revised down from 3.6%.

- AUD/USD prints at $0.6830/35, the pair is up ~0.9% today. Resistance comes in at $0.69, the high from June 16 and key resistance, then $0.6936, the high from Feb 16.

- Kiwi is firmer after the bid in AUD spilled over, although the NZD is marginally lagging. NZD/USD is up ~0.7% and sits a touch above the $0.63 handle. Bulls target yesterday's high ($0.6344), a break through here opens the high from 14 July ($0.6412).

- Yen is also firmer, USD/JPY is down ~0.3% and the pair last prints at ¥139.10/20. Japanese trade balance for June was on the wires this morning, a surplus of ¥43.0bn was printed. A deficit of 46.7bn had been expected. Support comes in at ¥137.25, low from Jul 14. Resistance is at ¥139.99 high from Jul 19.

- Elsewhere in the G-10 space, NOK is up ~0.7% however liquidity is generally poor in Asia. EUR is up ~0.2%.

- Cross asset wise; regional equities are little changed from yesterday's closing levels. US Equity futures are pressured albeit off session lows. Netflix lead US Equities lower in post market trade after sales missed Wall St estimates. BBDXY is down ~0.3% and US Tsy Yields are a touch firmer across the curve.

- PPI data from Germany headlines in Europe, further out we have US Initial Jobless Claims.

JAPAN DATA: Trade Balance Returns To Surplus

Japan June exports were slightly weaker than expected, printing at +1.5% y/y, versus +2.4% forecast and 0.6% prior. Imports also undershoot forecasts, albeit by slightly more - printing at -12.9% y/y, versus -11.3% forecast and -9.8% prior. This enabled the trade balance to rise more than expect to +¥43bn versus -¥46.7bn forecast and -¥1381.9bn. This is the first trade surplus since July 2021. It's consistent with an improved terms of trade backdrop since the start of this year, see the chart below.

- On the export side, trends to the US (+11.7% y/y) and the EU (+15.0%) were positive. Less so for China (-11.0%y/y) and Asia (-8.4%y/y).

- Import growth continues to trend lower, now back to lows from Q4 2020.

Fig 1: Japan Trade Balance & Citi ToT Measure For Japan

Source: Citi/Market News - MNI/Bloomberg

EQUITIES: Lower US Futures Weigh, While China Support For The Private Sector Doesn't Lift Sentiment

Asia Pac equities are mixed, with weaker US futures weighing on some markets. Netflix leads US Equities lower in post market trade after sales missed Wall St estimates. Eminis are down 0.14% to ~4591, while Nasdaq futures are off 0.45%, which is away from session lows. A sharp rebound in CNH, coupled with reports the authorities are considering easing mortgage rules to boost demand, hasn't aided HK or China mainland equities a great deal.

- The HSI is up 0.26% at the break, which is down from earlier session highs.

- The authorities stated yesterday they would support the private sector and protect businesses. Then Bloomberg headlines crossed today, stating the authorities were considering easing mortgage rules to spur housing demand in big cities. Some weakness in tech shares (off around 0.30%) has weighed amid profit concerns.

- Mainland shares have also struggled for positive traction, despite the above positives. At the break, the CSI 300 is off by 0.10%, the Shanghai Composite -0.33%.

- Japan's Nikkei 225 is off by around 0.95% at this stage, while the Topix is down by ~0.60%. A firmer yen backdrop, coupled with lower US futures has weighed.

- The Kospi is weaker in South Korea, off ~0.20%, but the Taiex is firmer, +0.35%, bucking the weaker SOX trend from US trade on Wednesday.

- In SEA, Indonesian markets have returned, with the JCI up 0.50%, while Philippine stocks have risen 1%. Thai stocks are weaker, down -0.25% as political uncertainty continues.

OIL: Crude Range Trading, Supply/Demand Factors Balancing Out

Oil has been range trading during the APAC session and is only 0.1% higher. Brent is around $79.55/bbl down from the intraday high of $79.74 and WTI is $75.39 after a high of $75.56. The USD index is 0.2% lower, providing some support to crude today.

- This week indications that Russia is reducing output have offset demand concerns stemming from China’s disappointing data and uncertainty re Fed policy. On Wednesday, China made a commitment to improve business conditions, which if successful could increase oil demand.

- The expiry of the August WTI contract today could increase volatility.

- US jobless claims, Philly Fed index and existing home sales print later.

GOLD: Highest Level Since May

Gold moved higher (+0.4%) in Asia-Pac trading, reaching its highest level since May, following a relatively unchanged closing on Wednesday. Despite a stronger USD, lower US tsy yields helped keep gold within a narrow range on Wednesday, having broken above the resistance level at $1968.0 (June 16 high) on Tuesday.

- Recently, gold has been supported by indications of a slowdown in price increases, leading traders to speculate about the Federal Reserve's potential pause in interest rate hikes, despite policymakers maintaining a hawkish stance.

- On Wednesday, US yields decreased by 1 to 2bp at the short end and 4 to 6bp at the long end after the release of lower-than-expected UK CPI (0.1% MoM vs. 0.4% est). Consequently, UK gilts closed 10 to 20bp richer.

ASIA FX: CNH Rebounds As Yuan Defence Steps Up

USD/Asia pairs are mostly lower, led by a sharp CNH rebound, as the authorities stepped up their defence of the yuan. THB outperformed early but has trimmed gains from best levels. Only MYR is not firmer against the USD in the session to date. Still to come is Taiwan export orders. Tomorrow, the focus will rest on the first 20-days of trade data for July out of South Korea.

- USD/CNH got to lows near 7.1750, but sits slightly higher now, last in the 7.1840/50 region, This is +0.65% stronger for the session and more than unwinds yesterday's dip. The CNY fixing was the strongest (relative to expectations) since Nov 2022, while macroprudential rules were shifted to enable onshore firms' greater access to offshore capital. Bloomberg also reported the authorities are considered easing mortgage restrictions.

- USD/THB hit fresh lows of 33.76 in earlier trade. We now sit higher, back around 33.90/95. This is fresh lows in the pair back to mid May. Lows at that juncture were in 33.55/60 region. Beyond that lies the 33.40 region, levels seen in early February of this year and then the 33.00 figure level. Highs from yesterday were near 34.20, while at the start of the week the pair topped out around the 34.70 level.

Broader USD weakness is helping the baht, although in the past week it has rallied over 2%, a clear outperformer, as market optimism grows we may be getting towards an end to the political impasse. Still, a Pheu Thai candidate could be fighting an uphill battle to secure enough votes in parliament, with the next PM vote scheduled for the 27th of July. - The rupee is marginally firmer in early dealing, the USD is broadly weaker however the Rupee is underperforming in the USD/Asia space. USD/INR prints at 82.03/05, the pair found support ahead of 82 in early trade and continues to hold above the figure. Strong inflows by foreign investors into Indian equities have continued with $369mn net inflow on Monday and Tuesday of this week.

- The Ringgit has pared early losses as broader USD/Asia weakness after a firmer than forecast Yuan fixing saw USD/MYR retreat from session highs. USD/MYR prints at 4.5450/4.5500, the pair is ~0.2% above yesterday's opening levels. Palm Oil futures sit at their highest level since early March, as supply concerns in the US market spill over. The market has looked through a stronger than forecast June Trade Balance, which printed at MYR25.81bn vs 16.65bn exp.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing, the measure sits a touch off cycle highs and is ~0.2% below the top of the band. Broader USD trends are dominating flows today, USD/SGD is down ~0.2% a touch above session lows and last prints at $1.3215/25. A reminder that the local docket is empty for the reminder of the week. Looking ahead, the next data of note is Monday's June CPI print, there are no estimates as of yet and the prior readings were 5.1% Y/Y (headline) and 4.7% Y/Y (core).

- USD/PHP sits below earlier highs, the pair last in the 54.40/45 region. Earlier highs were close to 54.65. The pull back is in line with broader USD weakness, with the move lower in USD/CNH particularly strong today. For USD/PHP we remain above recent lows around the 54.30 level. This keeps us within recent ranges for the pair. Peso bulls will target a move towards 54.20, late March lows, while we need to fill the gap back towards the July 12 low of 54.94 on any renewed upside push. On the geopolitical front, the country stated the US has pledged to support the Philippines defence upgrade and that the Philippines will do everything to assert its rights in the South China Sea.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/07/2023 | 0600/0800 | ** |  | DE | PPI |

| 20/07/2023 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 20/07/2023 | 0800/1000 | ** |  | EU | EZ Current Account |

| 20/07/2023 | 1230/0830 | ** |  | US | Jobless Claims |

| 20/07/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 20/07/2023 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 20/07/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 20/07/2023 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 20/07/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 20/07/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 20/07/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 20/07/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 10 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.