Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Treasuries open Asia trading slightly firmer, however weakened after Atlanta Fed Bostic's comments, where he mentioned there is no rush to cut rates, but sees two rate cuts this year. This has supported USD sentiment, with marginal index gains. Still the BBDXY is tracking higher for the 7th straight week.

- Risk appetite has been buoyant in the equity space though, likely helping contain some of the fallout for higher beta FX. Hong Kong equities surge higher continued their winning streak post the LNY break, as investors hope for a MLF cut this weekend, while China consumer spending is picking up with a surge in travel spending during the LNY break.

- Looking ahead, UK retail sales data headlines the European docket on Friday before focus turns to US PPI figures and building permits. Preliminary UMich consumer sentiment and inflation expectations will round off the week.

MARKETS

US TSYS: Treasuries Weaken on Fed's Bostic's Comments, US PPI Later

TYH4 is currently trading at 110-01, down - 04+ from New York closing levels.

Treasuries open Asia trading slightly firmer, however weakened after Atlanta Fed Bostic's comments, where he mentioned there is no rush to cut rates, but sees two rate cuts this year.

- Treasury futures are testing lows as Asia breaks for lunch, the move lower was driven by Fed's Bostic comments. Mar'24 10y futures hit a low of 110-00+, currently just above there at 110-01, while Mar'24 2Y futures broke through US session lows to trade at 102-01+.

- Ahead of another day of US data, key technical levels to watch include initial support at 109-17/16+ (50.0% of the Oct 19 - Dec 27 bull phase/Low Feb 14), a break below here could open up new yearly lows and a test of 109-05+ (lows of Nov 28). To the upside, initial resistance lies at 110-17.5 (the highs from Feb 15th), while a break above opens up a move to 111-02+ (20-day EMA).

- Cash yields are 1-3bps higher across the curve, the 2Y yield +2.3bp higher at 4.597%, 10Y yield +2.3bps higher at 4.253%.

- Headlines have been on the quiet side during the Asia today, with a meeting between US Secretary Of State and China's Wang Yi later the only thing to note.

- Looking ahead: Friday data calendar includes PPI, House Starts/Build Permits, UoM Inflation

STIR: $-Bloc 2024 Easing Expectations Remain Substantial

STIR markets in the $-bloc continue to anticipate an easing cycle in 2024, albeit with significantly reduced expectations relative to late January.

- The trimming of year-end easing projections gained momentum earlier in the week after unexpectedly high US CPI for January.

- Relative to early February, official rate expectations for December 2024 currently sit 25bps (Australia) to 47bps (NZ) higher across the $-bloc. They were another 10-15bps higher on Wednesday versus today.

- December 2024 expectations and the cumulative easing across the $-bloc stand at: 4.44%, -89bps (FOMC); 4.32%, -68bps (BOC); 3.88%, -44bps (RBA); and 5.15%, -48bps (RBNZ).

JGBS: Futures Cheaper & At Session Lows, Enhanced-Liquidity Auction Due

In the afternoon session, JGB futures sit in negative territory and at session lows, -8 compared to the settlement levels.

- There hasn’t been much in the way of domestic drivers to flag today. December’s Tertiary Industry Index has just been released showing a rise of 0.7% m/m versus +0.2% est.

- Later today, the MoF will conduct an Enhanced-Liquidity Auction for OTR 15.5-39-year JGBs.

- BoJ Governor Ueda, in Parliament today, said the BoJ will consider whether it will keep its large-scale monetary easing policies including the negative rate once its price goal comes into sight. That said, financial conditions are likely to stay accommodative for the time being even if the negative rate is ended given the current economic outlook.

- Cash US tsys are dealing 2-3bps cheaper in today’s Asia-Pac session after Atlanta Federal Reserve President Raphael Bostic said after market that he is still not thoroughly convinced inflation is on track to the central bank's 2% target (MNI)

- Cash JGBs are dealing mixed, with yield movements across the curve bounded by +/- 2bps. The benchmark 10-year yield is 0.9bp higher at 0.735% versus the February low of 0.665%.

- The swaps curve has slightly bear-steepened out to the 20-year, with rates unchanged beyond. Swap spreads are wider.

- The local calendar sees Core Machine Orders on Monday, ahead of 20-year supply on Tuesday.

AUSSIE BONDS: Cheaper, Near Weakest Levels, Narrow Ranges

ACGBs (YM -3.0 & XM -4.5) are cheaper and at/or near Sydney session lows. With the domestic calendar empty today, the local market has drifted cheaper with US tsys in today’s Asia-Pac session. Cash US tsys are dealing ~2bps cheaper compared to the NY close.

- Cash ACGBs are 3-4bps cheaper, with the AU-US 10-year yield differential 2bps higher at -7bps. At -7bps, the 10-year yield differential currently sits in the bottom half of the range of +/-30bps which has been observed since November 2022.

- However, a simple regression of the AU-US cash 10-year yield differential against the AU-US 1Y3M swap spread over the current tightening cycle indicates that the 10-year yield differential is currently 13bps too low versus its fair value (i.e., -7bps versus +6bps).

- Swap rates are 3-5bps higher, with EFPs little changed.

- The bills strip has bear-steepened, with pricing -1 to -4.

- RBA-dated OIS pricing is flat to 3bps firmer across meetings. A cumulative 36bps of easing is priced by year-end.

- Next week, the local calendar is empty on Monday, ahead of the RBA Minutes of the Feb. Policy Meeting on Tuesday.

- Next Wednesday, the AOFM plans to sell A$800mn of 3.75% Apr-37 bond.

NZGBS: Closed On A Weak Note

NZGBs closed on a weak note, with benchmark yields 1-5bps cheaper and the 2/10 curve steeper. The local highlight today was a speech from RBNZ Governor Orr. He didn't, however, touch on the rates outlook. The Governor stated: "Tackling these persistent inflationary pressures and bringing levels of ‘core’ inflation in line with our 1 to 3% target is an important part of bringing inflation back down to the 2% midpoint." You can see the full speech at this link.

- The NZ-AU 10-year yield differential closed unchanged at +63bps, with the NZ-US differential 2bps tighter at +56bps.

- The previously outlined BusinessNZ Manufacturing PMI was the only data today. It didn’t move the market.

- (Bloomberg) -- NZ posted its biggest calendar-year jump in population since the end of World War Two, reinforcing the scale of the potential impact on demand and inflation from record immigration. The estimated population increased by 2.8% in 2023. (See link)

- Swap rates are 1-5bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is 1-4bps softer across meetings, with May-July leading. A cumulative 45bps of easing is priced by year-end.

- Next week, the local calendar sees the Performance Services Index and Non-Resident Bond Holdings on Monday, ahead of Q4 PPI on Wednesday.

AUSSIE BONDS: AU-US 10-Year Yield Differential Too Tight

Today, the AU-US 10-year cash yield differential is 3bps higher at -7bps.

- At -7bps, the cash AU-US 10-year yield differential currently sits in the bottom half of the range of +/-30bps which has been observed since November 2022.

- However, a simple regression of the AU-US cash 10-year yield differential against the AU-US 1Y3M swap differential over the current tightening cycle indicates that the 10-year yield differential is currently 13bps too low versus its fair value (i.e., -7bps versus +6bps).

- The 1y3m differential is a proxy for the expected relative policy path over the next 12 months.

Figure 1: AU-US Cash 10-Year Yield Differential (%) Vs. Regression Fair Value (%)

Source: MNI – Market News / Bloomberg

RBNZ: Still More Work To Do To Anchor Inflation Expectations

RBNZ Governor Orr gave a speech earlier today in NZ. Note Governor Orr didn't touch on the rates outlook in the speech.

- The Governor stated: "Tackling these persistent inflationary pressures and bringing levels of ‘core’ inflation in line with our 1 to 3% target is an important part of bringing inflation back down to the 2% midpoint."

- "In this context, a flexible approach to inflation targeting, with a medium-term focus, remains appropriate. This provides the Monetary Policy Committee with the ability to weigh different considerations when responding to shocks to the economy. The Reserve Bank believes that the current 2% mid-point inflation target remains appropriate for New Zealand."

- “2% continues to strike the right balance between the costs and benefits of inflation,” Mr Orr says. “A focus on 2% appears to be consistent with an ‘optimal’ level of inflation.”

- He added: "Non-tradable inflation is slowly moving in the right direction", But that "We’ve got more work to do to have inflation expectations truly anchored at that 2% level. This is the part where capacity pressures and inflation expectations are the monetary committee’s real focus.”

- You can see the full speech at this link.

FOREX: USD Firms, Tracking Higher For The 7th Straight Week

The USD index has firmed in the first part of Friday trade the BBDXY up 0.10% to be tracking above 1245. We are comfortably below earlier highs in the week (post the US CPI print above 1251), but still up for the week, which would be the 7th straight run of weekly gains.

- USD strength coincided earlier with Fed Bostic comments, which helped US yields firm a touch. The Fed official stated that he wants more certainty in the inflation fight before cutting rates. He added he projects 2 rates cut this year, which is obviously well short of what markets are pricing (close to 90bps). The comments don't appear a departure from what Bostic has said previously though.

- US yields are 1.5-2.5bps firmer across the benchmarks, the 10yr last near 4.25%.

- USD/JPY dipped in early trade to 149.83, but is back to 15.30/35 this afternoon just off session highs. Comments by BoJ Governor Ueda in parliament were in line with recent rhetoric, while FinMin Suzuki warned about FX, but again the language used didn't appear to a departure from what we have seen recently around intervention risks.

- AUD/USD and NZD/USD are also lower, albeit outperforming JPY at the margins. AUD/USD was last 0.6510/15, while NZD is back sub 0.6100. The positive regional equity tone (MSCI Asia Pac up 1%), may be providing some offset to the firmer US yield backdrop.

- Earlier RBNZ Governor Orr stated that more needs to be done to anchor inflation expectations, but didn't touch on the rates outlook in his speech.

- Looking ahead, UK retail sales data headlines the European docket on Friday before focus turns to US PPI figures and building permits. Preliminary UMich consumer sentiment and inflation expectations will round off the week.

Hong Kong/China Equites: Hong Kong Equities Surge Higher, MLF Sunday

Hong Kong and China equities surge higher to continue their winning streak post the LNY break, as investors hope for a MLF cut this weekend, while China consumer spending is picking up with a surge in travel spending during the LNY break.

- As we break for Asia lunch Hong Kong equity markets are surging higher, with hope for a MLF cut and consumer spending picking up, while any weakness in equities over the past week or so has been met with swift buying. It has been light on for market moving headlines today. While looking more closely at the market, the China Mainland Property Index is 4.81% higher today, this is after property developer Redsun was issued with a Wind-Up noticed yesterday. The HS Tech index trades 3.41% higher, supported by positive US tech earnings, while the HS China Enterprise Index, which tracks Chinese companies listed on the Hong Kong exchange, is up 2.44% and finally the HSI is 2.20%

- In headlines, US Secretary Of State will meet with China's Wang Yi later today, while Chinese builder Logan gets respite as a Hong Kong court dismisses petitions to wind up the business, stock is 10% higher, while bonds in the company are changed trading in the 10/12 area

- Looking ahead note that China markets return on Monday. Sunday is slated for the MLF announcement. No change is expected by the consensus in terms of the current 1yr rate at 2.50%, although some forecasters are penciling in a 10bps cut.

ASIA PAC EQUITIES: Regional Asian Equities Hit 2022 Highs

Regional Asian equities continue their march higher today BBG APAC Index is heading for it's highest levels since march 2022, after Japanese equities edge close to hitting all time highs not seen since 1989. Tech stocks are the top performers in the region after US semiconductor equipment manufacturer Applied Materials posted a bullish revenue forecast.

- Japan equities are higher today following the another record high close for the US market on Thursday, while the weaker yen continues to support the market. The Nikkei 225 continues to edge closer to all time highs of 38,915.87, while demand for March options betting on the Nikkei 225 to break to 40,000 soar today to levels not since June. Currently the Nikkei 225 is 1.53% higher, while Topix is 1.66% higher.

- Taiwan equities are lower today, under-performing the wider Asian markets as investors look to book profits, after equities surged 3.46% yesterday. Currently the Taiex is down 0.10%.

- South Korea equities edge higher again today, led by tech names. Foreign buying of SK stock has slow in the past week with just $42m of inflows today as the 5-day moving average decreased to 252.1m below the 20-day average of $288.5m. Currently the Kospi is 1.14% higher.

- Australia equities closed higher today led by Miners and Financials as CBA, up 1.75% contributes most to the index gain. Elsewhere Australia's stock exchange the ASX fell 4.00% after the company misses estimates. The ASX 200 is up 0.67%.

- Indonesian equities continue their moves higher post presidential election, while Global fund buying of Indonesian stock hit a 2 month high with $174.6m of inflows on Thursday. Currently the Jakarta Comp is 0.63% higher.

- Elsewhere in SEA, NZ up 0.73%, Singapore up 1.41%, Philippines up 0.36%, while Thailand lags trading unchanged for the day.

JAPAN DATA: Inflows Into Japan Stocks Continue, Japan Investors Ramp Up Offshore Bond Purchases

Japan weekly investment flows saw continued buying from offshore investors into local equities. A total of ¥621.3bn of net inflows were recorded last week. This marked the 6th straight week of inflows into the space. There had been some chatter such inflows from China investors may cool as the authorities look to prop up the local markets, but this didn't disrupt the aggregate flow picture (at least for last week). In terms of flows into local bonds they remained positive at ¥175.9bn, but down from the prior pace.

- In terms of outbound Japan flows to the rest of the world, there was a sharp spike in offshore bond purchases, just under ¥1500bn, see the table below. The net flow picture into this has been positive since mid-Dec last year.

- Offshore flows into overseas stocks by local investors were a much more modest ¥22.1bn.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending Feb 9 | Prior Week |

| Foreign Buying Japan Stocks | 621.3 | 308.2 |

| Foreign Buying Japan Bonds | 175.9 | 397.7 |

| Japan Buying Foreign Bonds | 1499.3 | 456.7 |

| Japan Buying Foreign Stocks | 22.1 | -194.5 |

Source: MNI - Market News/Bloomberg

OIL: Largely Holding Thursday's Gains, Firmer For The Week

Oil benchmarks have largely drifted sideways in the first part of Friday trade. The front month Brent contract sits at $82.75/bbl in recent dealings, down slightly from end Thursday levels. We are marginally higher versus end levels from last week ($82.19/bbl). For WTI we are holding above $78/bbl, with a firmer rise in the past week compared to Brent (+1.6%). Dips sub $78/bbl have been supported so far today.

- The benchmarks are largely holding impressive gains from Thursday's session, although we haven't seen a test of Thursday highs.

- This may reflect broader risk trends, which are positive in the equity space, but the USD has edged higher, providing an offset.

- While risk tones are positive, Thursday's IEA report suggested some caution around the demand/supply balance in 2024.

- Focus will remain on the Middle East where the Houthi's vowed to continue attacks on Red Sea shipping.

- US President Biden spoke to Israeli leader Netanyhu and again urged restraint around a potential assault on the southern Gaza city of Rafah.

GOLD: Rebound After Weaker Than Expected US Retail Sales

Gold is little changed in the Asia-Pac session, after closing 0.6% higher at $2004.40 on Thursday.

- After falling earlier in the week in the wake of Tuesday’s hotter-than-anticipated inflation reading, the yellow metal climbed back over the $2,000 threshold on softer-than-expected retail sales (-0.8% m/m vs. -0.2% est. and 0.6% prior). Overall, the contraction in retail sales pointed to the weakest report since March 2023.

- According to the MNI technicals team, technical conditions for spot gold may be limiting the advance, following the prior breach this week of $2001.9, the Jan 17 low and a key short-term support.

- That breach highlighted a resumption of the bear leg that started Dec 28. A continuation lower would open $1973.2, the Dec 13 low and the next key support. On the upside, the yellow metal would need to clear resistance at $2065.5, the Feb 1 high, to reinstate a bullish theme.

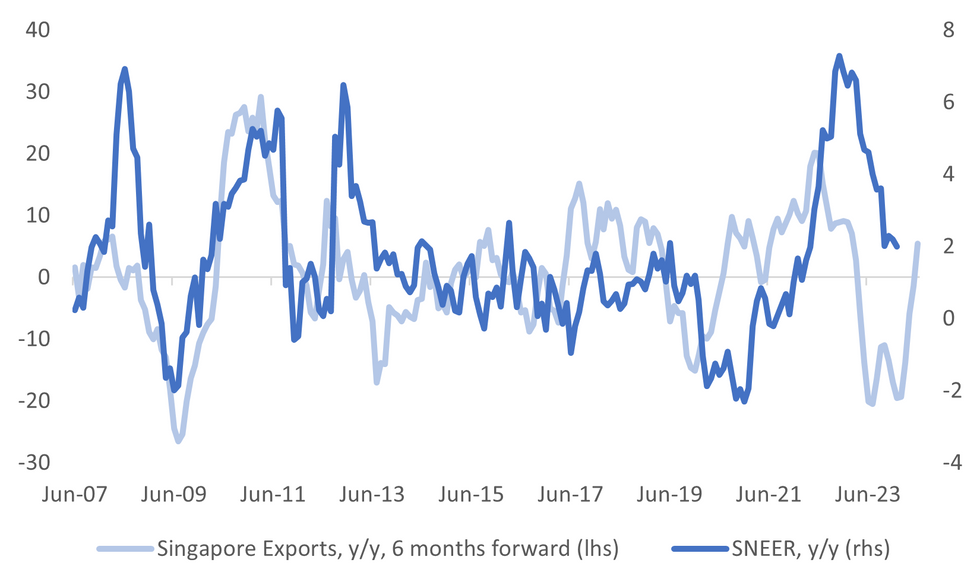

SINGAPORE DATA: Jan Export Beat Should Support Resilient NEER Backdrop

Singapore Jan export figures were stronger than expected. In m/m terms exports rose 2.3% against a 0.5% forecast and -1.7% prior (originally reported as a -2.8% fall). In y/y terms, we rose 16.8%, against a 4.3% forecast and -1.5% prior. This is the strongest y/y pace since early 2022. Electronic exports rose 0.7% y/y, versus -11.7% prior. This is first positive print since Q3 2022 for this series in y/y terms.

- Jan last year marked a trough point for y/y export momentum, hence base effects likely aided the bounce. Still, the detail showed fairly broad based gains in terms of the sub components, albeit with some from a low base.

- The electronic sub components were mostly up in m/m terms, but the large shift came from non-electronic exports, with chemical exports rising strongly in the m/m. Non-electronic exports were +21.2% y/y versus +1.4% in Dec.

- This improvement is line with better trends seen in other Asian export orientated economies like South Korea and Taiwan.

- For the MAS it forms part of a resilient growth backdrop, with Q4 growth GDP figures showing continued growth through the tail end of last year.

- The chart below plots export growth trends (pushed 6 months forward) against the SGD NEER in y/y terms. The picture paints a resilient NEER backdrop, all else equal.

Fig 1: SGD NEER Versus Export Growth Trend (6 Months Forward)

Source: MNI - Market News/Bloomberg

ASIA FX: China Markets Return Next Week, MLF Outcome Potentially On Sunday

USD/Asia pairs have been mixed, despite a generally positive equity tone to the region. A firmer US yields/broader USD backdrop has provided some offset though. As we look ahead to next week, China markets will return. Ahead of that the MLF outcome may print on Sunday (the first working day after LNY). No change is expected by the consensus, although come forecasters are penciling in a 10bps cut. Later next week we get the BI decision in Indonesia and BoK outcome, but neither central bank is expected to adjust policy rates.

- USD/CNH is little changed holding near 7.2180. The equity tone in Hong Kong has been positive for much of this week since markets returned, but this hasn't impacted CNH sentiment meaningfully as the market awaits the return of onshore markets next week from the LNY break. Note that Sunday is slated for the MLF announcement. No change is expected by the consensus in terms of the current 1yr rate at 2.50%, although some forecasters are penciling in a 10bps cut.

- 1 month USD/KRW has firmed versus end NY levels on Thursday, the pair last near 1331/32, around 0.30% weaker in won terms for the session. This comes despite a decent rise in onshore equities (Kospi up over 1.2%). The firmer USD backdrop against the majors is likely weighing at the margins. Earlier data showed a dip in the unemployment rate in Jan and a resilient jobs growth backdrop.

- USD/IDR has firmed in the first part of Friday dealing, although is off session highs. The pair was last at 15640. These moves keep us within recent ranges, albeit with spot testing resistance above the 20-day EMA near 15660 earlier today. Recent lows around 15565 remain intact. IDR is diverging somewhat from the positive local equity market trend. The JCI up a further 0.80% so far today, the index now close to the 7400 level, which is near early Jan highs. Yesterday saw a chunky $174.8mn in offshore inflows into local equities, the most in 2 months. The likelihood of clear election winner and policy continuity is aiding the Indonesian asset backdrop, although markets will look to the cabinet make up (particularly in terms of the FinMin) and fiscal discipline as important signposts for the new regime.

- Earlier data showed a stronger than expected bounce in Singapore exports for Jan. This was consistent with green shoots from the likes of South Korea and Taiwan in recent months. USD/SGD hasn't moved much though, last near 1.3460. The NEER is slightly firmer, last -0.40% from the top end of the policy band (per Goldman Sachs estimates). We were -0.60% earlier this week.

- USD/MYR sits down a touch, last just under 4.7790. Resistance is likely around the 4.8000 region. Earlier data showed better than expected Q4 GDP data, although full year growth for 2023 was slightly below estimates. Comments from BNM also suggested downside risks to the outlook. The current account position was barely positive in Q4. Net portfolio outflows continued in the quarter, albeit at a reduced pace.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/02/2024 | 0700/0700 | *** |  | UK | Retail Sales |

| 16/02/2024 | 0700/0800 | ** |  | SE | Unemployment |

| 16/02/2024 | 0745/0845 | *** |  | FR | HICP (f) |

| 16/02/2024 | 0845/0945 |  | EU | ECB's Schnabel lecture at EMU Lab | |

| 16/02/2024 | 1300/0800 |  | US | Richmond Fed's Tom Barkin | |

| 16/02/2024 | 1330/0830 | * |  | CA | International Canadian Transaction in Securities |

| 16/02/2024 | 1330/0830 | ** | | CA | Wholesale Trade |

| 16/02/2024 | 1330/0830 | *** | | US | PPI |

| 16/02/2024 | 1330/0830 | *** | | US | Housing Starts |

| 16/02/2024 | 1410/0910 | | US | Fed Vice Chair Michael Barr | |

| 16/02/2024 | 1500/1000 | ** | | US | U. Mich. Survey of Consumers |

| 16/02/2024 | 1710/1210 | | US | San Francisco Fed's Mary Daly | |

| 16/02/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 16/02/2024 | 1940/1940 | | UK | BOE's Pill panellist at 40th NABE Conference |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.