Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

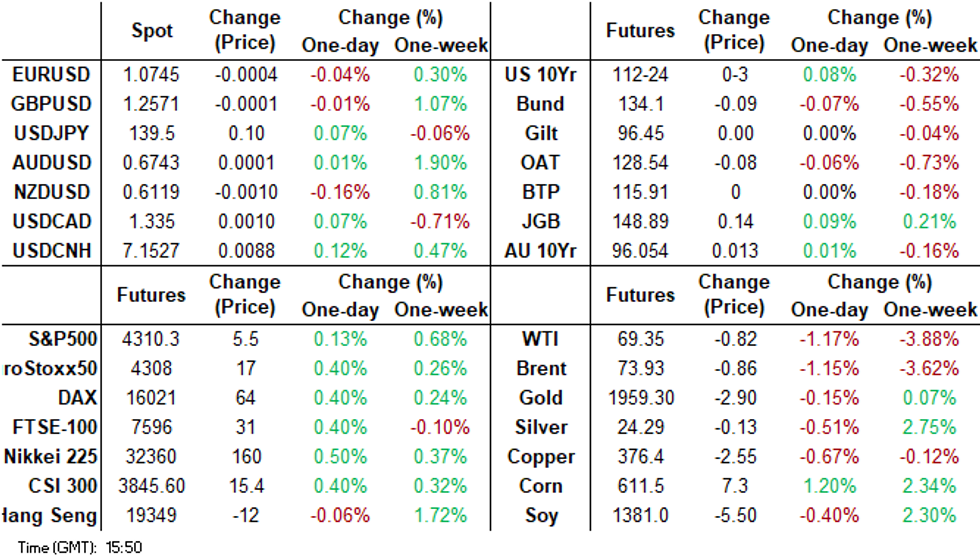

- At the open, despite the absence of any headline driver, TY gapped lower before finding support ahead of Friday's low and pared losses. Perhaps the proximity to tomorrow's CPI print and Wednesday's FOMC decision has kept local participants on the sidelines.

- JGB futures spiked higher as May PPI came in weaker than expected and an ex-BoJ Deputy Governor stated the central bank would hold steady this Friday. We are away from highs but have outperformed US Tsys. Moves in the G10 FX space were fairly muted, the BBDXY sits slightly higher. In the commodity space, oil continues to track lower, while some steam has come out of the iron ore rally.

- USD/CNH made another fresh high, close to 7.1600, as speculation rises we could see a MLF rate cut this Thursday.

- Looking ahead, the data is light tomorrow, but we do have US CPI tomorrow.

MARKETS

US TSYS: Marginally Cheaper In Asia

TYU3 deals at 113-11, -0-01+, with a 0-06+ range observed on volume of ~38k.

- Cash tsys sit flat to 1bp cheaper across the major benchmarks, light bear flattening is apparent.

- Tsys have ticked away from session highs dealing in a narrow range for the Asian session, perhaps the proximity to tomorrow's CPI print and Wednesday's FOMC decision has kept local participants on the sidelines.

- At the open, despite the absence of any headline driver, TY gapped lower before finding support ahead of Friday's low and pared losses.

- FOMC dated OIS price ~8bp of hikes into Wednesday's meeting, a terminal of 5.30% is seen in July with ~25bps of cuts in 2023.

- There is a thin data calendar on Monday, we have the latest 3- and 10-Year Supply. Further out the weekend is headlined by the aforementioned CPI print tomorrow and Wednesday's FOMC rate decision.

JGBS: Outperform Tsy Futures Post PPI Miss & Ex BoJ Deputy Governor Comments

JGB futures are sitting towards the upper end of their range for the session so far. We are at 148.17 currently (+0.16), after a 148.00/26 range. This has outperformed the slightly softer US Tsys backdrop evident in the session to date (TYU3 -01 at 113-11).

- Japanese domestic news has likely aided this outperformance at the margins. PPI printed weaker than expected early doors (see this link), while ex-Deputy Governor Wakatabe stated he sees no change from the BoJ this Friday, nor at the July meeting (an upward revision to the inflation view is expected at the July meeting though).

- These latter comments are in line with Bloomberg's BoJ report from late on Friday, which suggested little need for YCC tweaks in the near term.

- In the cash JGB space we have seen a slight downtick in yields but very little follow, with a firmer US cash Tsy yield backdrop likely providing some offset. The 10yr yield was last close to 0.425%. In the swap space it been a similar story, the 10yr last just under 0.59%.

- Still to come is preliminary May machine tool orders. There is no market consensus, but the prior read was -14.4% y/y.

JAPAN DATA: PPI Weaker Than Expected, JGB 10yr Futures To Fresh Highs

Japan's May PPI printed weaker than expected, coming in at -0.7% m/m (forecast -0.2%), although Apr was revised slightly higher to 0.3%, versus 0.2% prior. The y/y pace came in at 5.1% y/y, versus 5.6% expected and 5.9% prior. Import prices were a noticeable drag at -9.6% y/y, while industry results were mixed. Manufacturing slightly negative in y/y terms.

- Japan 10yr JGB futures have opened higher, last around session highs, currently 148.22 (+0.21). This is comfortably above Friday session highs. This is fresh multi week highs in the contract.

- Ex BoJ Deputy Governor Wakatabe was on Bloomberg Tv and stated that he was unsure if the BoJ would change policy in July, but expected some sort of upward revision to the inflation profile.

- USD/JPY has been relatively steady, last in the 139.35/40 region.

NZGBs: Marginally Cheaper On Monday

NZGBs have finished dealing 0.5-3.5bps cheaper across the major benchmarks, the curve has bear flattened.

- RBNZ dated OIS are little changed on Monday, pricing a terminal rate of 5.63% in October.

- Swap rates are a touch higher rising 2bp across 2s,5s and 10s.

- Retail Card Spending fell 1.9% M/M in May with the prior number revised lower to 0.5% M/M from 1.0% M/M. Retail Spending fell 1.7% M/M, the prior number was revised lower to 0.4% M/M from 0.7% M/M.

- NZIER's Quarterly Consensus notes that economists see 2023/24 GDP expanding at 0.6%. Westpac noted they see Fonterra 2023/24 milk price at $8.90/kg.

- Looking ahead, April Net Migration crosses tomorrow, before Q1 BoP and May Food Prices on Wednesday. Q1 GDP on Thursday headlines the week's docket, a fall of 0.1% Q/Q is expected.

FOREX: USD Marginally Firmer In Asia

The USD is a touch firmer in Asia Monday, however ranges have been narrow with little follow through on moves.

- Kiwi is marginally pressured, NZD/USD is down ~0.1% trimming some of Friday's gains. The pair has see-sawed around its 20-Day EMA with little follow through on moves. NZIER's Quarterly Consensus notes that economists see 2023/24 GDP expanding at 0.6%. Westpac noted they see Fonterra 2023/24 milk price at $8.90/kg.

- AUD/USD has observed a narrow range, last printing at $0.6740/45 little changed from opening levels. Resistance comes in at $0.6751 high from June 9 and support at $0.6623 the 20-day EMA.

- Yen is a touch firmer, USD/JPY sits marginally below opening levels however a ~25pip range has persisted in Asia today. Early in the session Japan's May PPI printed weaker than expected, coming in at -0.7% m/m (exp -0.2%), although Apr was revised slightly higher to 0.3%, versus 0.2% prior.

- Cross asset wise; US Treasury Yields are ~1bp firmer across the curve and BBDXY is up ~0.1%. E-minis are also ~0.1% firmer.

- The docket is thin on Monday, further out the highlights of the week are US CPI (Tuesday), FOMC rate decision (Wednesday) and BoJ monetary policy decision (Friday).

EQUITIES: Mixed Start To Busy Central Bank Week

Regional equities have gotten off to a mixed start this week. Japan stocks are modestly higher, while HK and mainland China are down slightly. SEA is mixed. US futures are positive but down from session highs. Eminis last around 4352.00, against a high of 4357.25. Nasdaq futures are slightly outperforming, last +0.15% at 14757.50, but also down from session highs.

- The Nikkei 225 is +0.25% at this stage, off from earlier highs. PPI data showed waning upstream price measures, while an ex-BoJ Governor didn't expect policy shifts from the central bank at the coming meeting this Friday.

- The HSI is down 0.57% at the break, while China stocks are slightly weaker. The CSI 300 remains above 3800 at this stage. Weakness in the HSI has been led by tech and banking sector names.

- There speculation the 1 yr MLF rate will be cut this Thursday, although recent commentary from the China authorities doesn't suggest we will see aggressive policy stimulus.

- The Kospi is tracking 0.50% lower, unwinding some of the recent outperformance, last around 2627 in index terms. The Taiex is tracking better, last around 0.50% firmer.

- In SEA Malaysia shares are the standout +1% higher. The government will extend existing subsidies and price controls for poultry and eggs beyond the original June 30 deadline. Also Malaysia named Shaik Rasheed Abdul Ghaffour as its new central bank governor, Malaysia's king approved Rasheed as the governor from July 1 for a period of 5 years.

OIL: Brent & WTI Close To Thursday Lows

Brent crude has continued to track lower. After opening closer to $74.90/bbl, we have mostly been on the backfoot, although some support has emerged sub $74/bbl (which is where we currently track). This isn't too far off Thursday lows, near $73.50/bbl, which came about post rumors of a US-Iran nuclear deal.

- At this stage, Brent is down a further 1.1%, having lost around 2.85% through Thurs/Fri last week. A fresh break of $73.50 will have the market targeting lows around $71.40/bbl from late May.

- WTI is back to just under $69.40/bbl, also close to Thursday session lows from last week (near $69/bbl).

- Goldman Sachs has cut its year-end Brent forecast to sub $90/bbl, the third downgrade it had made in 6 months.

- We did see investor positioning turn more constructive for oil in terms in the week ending June 6, but it remains to be seen if this is maintained following more bearish price action in recent sessions.

- Outside of the central bank meetings this week, also note that OPEC publishes its monthly Oil Market Report on Tuesday.

MNI Insight: USD/CNH Uptrend Persists, But The Authorities Appear Prepared To Ride Out USD Strength

EXECUTIVE SUMMARY:

- From earlier YTD lows, both USD/CNY & USD/CNH are nearly 7% higher. The yuan is the second weakest performer in Asia YTD (MYR is the worst). The yuan has come unstuck as the re-opening trade has lost momentum, which has weighed on China asset sentiment more broadly. US-China tensions haven’t helped either.

- A continued elevated US yield backdrop is the other yuan headwind, although China is not alone on this front. Uncertainty remains around the state of the US rate cycle, we get a fresh update on Fed thinking and May CPI this week.

- Despite the recent yuan weakness, the authorities appeal fairly relaxed about the current FX backdrop. The CNY fixing has shown little pushback against renewed depreciation pressures. This may change if we see depreciation pressures quicken or we revisit CNY lows from Q4 last year.

- This week we get updates on May China activity data, as well as new lending/credit. There is also speculation we could see a MLF cut on Thursday.

- All in all, it may take a more definitive peak in US rates/coupled with a better China growth outlook to bring a meaningful correction in USD/CNH.

- See here for more details.

ASIA FX: Fresh Highs For USD/CNH Before Retracing

Most USD/Asia pairs are firmer, although we are down from session highs, as USD/CNH spiked to a fresh high, before retracing. A firmer US yield backdrop has aided the USD, although a better regional equity tone late in the session has helped cap USD upside. Still to come late is India CPI and IP data. The data calendar is quiet tomorrow, but we are awaiting China new lending/credit figures for May.

- USD/CNH made fresh highs close to 7.1600 (7.1590) but has retraced back sub 7.1400 this afternoon. A reversal of earlier equity market weakness, with onshore bourses tracking higher after the break is likely aiding CNH sentiment. Speculation continues around a possible MLF cut this Thursday, the Securities Journal stating a 5-10bps move could be delivered.

- 1 month USD/KRW got to highs near 1292, as USD/CNH rose, but we now sit back at 1286.50, close to lows from late in NY on Friday. Local equities have struggled but are away from lows. Earlier data showed tentative signs of less headwinds around y/y export growth. BoK Governor Rhee also stated in a speech that it is too early to be confident on inflation easing, but attention needs to be paid to slowing growth as well.

- USD/MYR prints at 4.6170/4.6210 the pair is ~0.1% firmer in early dealing. Palm Oil futures are trimming some of Fridays ~3% gain, down ~0.6%. We remain well within recent ranges and sit ~4.5% off cycle lows registered in early June. Malaysia named Shaik Rasheed Abdul Ghaffour as its new central bank governor, Malaysia's king approved Rasheed as the governor from July 1 for a period of 5 years. More info here. The local data calendar is empty this week.

- USD/INR has opened dealing little changed from Friday's closing levels in a muted start to the week's dealing. Ranges continue to be narrow in recent dealing, the pair has see-sawed around the 20-Day EMA (82.49) with little follow through. Inflows into Indian equities from Foreign Investors continue, with $74.22mn on 8 June bringing to total inflow June to date to $721.3mn. On the wires today we have May CPI, the market expects a rise of 4.32% Y/Y moderating from 4.70% in April. Also due is Apr Industrial Production, a rise of 1.3% Y/Y is forecast, an uptick from 1.1% Y/Y in March.

- The SGD NEER (per Goldman Sachs estimates) printed a cycle high on Friday before paring gains to finish a touch softer. We now sit ~0.6% below the upper end of the band. USD/SGD is a touch firmer in early dealing, the pair last prints at $1.3430/40 as broader greenback trends dominate in early dealing. Data-wise the only data of note this week is May Export data. Non-Oil Domestic Exports are estimated to have fallen 1.1% M/M and 7.6% Y/Y. Electronic Exports is also due, there is no estimate for the release.

SOUTH KOREA: First 10-Days Trade Data For June Show Better Headline Results

The first 10-days of South Korean trade data in June showed some better headline results. Export growth was +1.2% y/y in the first 10-days. Average daily exports for the period were -6% y/y, which is still an improvement compared to recent months. Looking at the detail though, we had car exports +137.1%, ship exports 161.5%. Chips remained negative -31.1% y/y, and oil products fell -35.8% y/y.

- By country, export trends were better to the US and the EU, but China remained softer at -10.9% y/y. Taiwan (-49.8% and Singapore (-44.1%) were also weaker.

- Imports fell -20.7% y/y, in the first 10days, which aided some improvement in the trade deficit to -$1.41bn.

- South Korea FinMin Choo has spoken about a better export picture as we progress through H2 in recent weeks. This data is tentative signs of at least a less adverse y/y momentum backdrop in the early parts of June.

- However, a sustained recovery in chip exports and better demand from China is likely needed in H2.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/06/2023 | - | *** |  | CN | Money Supply |

| 12/06/2023 | - | *** | | CN | New Loans |

| 12/06/2023 | - | *** | | CN | Social Financing |

| 12/06/2023 | 1500/1100 | ** |  | US | NY Fed survey of consumer expectations |

| 12/06/2023 | 1530/1130 | *** | | US | US Note 03 Year Treasury Auction Result |

| 12/06/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 12/06/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 12/06/2023 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 13/06/2023 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 13/06/2023 | 0600/0800 | *** |  | DE | HICP (f) |

| 13/06/2023 | 0600/0800 | ** |  | NO | Norway GDP |

| 13/06/2023 | 0700/0900 | *** |  | ES | HICP (f) |

| 13/06/2023 | 0900/1100 | *** | | DE | ZEW Current Conditions Index |

| 13/06/2023 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 13/06/2023 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 13/06/2023 | 1000/0600 | ** | | US | NFIB Small Business Optimism Index |

| 13/06/2023 | 1230/0830 | *** | | US | CPI |

| 13/06/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 13/06/2023 | 1400/1500 | | UK | BOE Bailey Lords Economic Affairs Committee Hearing | |

| 13/06/2023 | 1400/1000 | | US | Treasury Secretary Janet Yellen | |

| 13/06/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 13/06/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 13/06/2023 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.