Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Chinese equities saw a sharp correction from lows which helped to stabilise markets overnight, in addition to triggering speculation re: China's "national team" stepping in to stop the rot in mainland equity markets.

- The DXY topped out around 92.50 as broader equity indices found a base.

- U.S. Tsy mid-month supply gets underway with 3s today, and comes in the wake of last month's 7-Year supply, which was particularly weak and triggered the well documented broader vol. in the space.

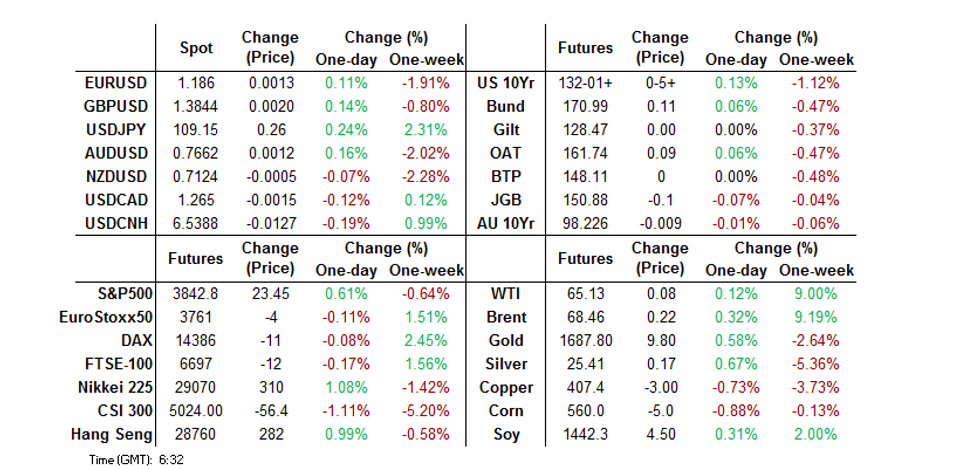

BOND SUMMARY: Core FI Mixed Overnight, But Off Worst Levels

Early modest cheapening in core FI markets unwound as circular drivers came to the fore during the early round of Asia-Pac trade. Asia-Pac $ IG bonds were under widening pressure and regional tech proxies in the equity space were sold heavily again, resulting in the DXY testing resistance and a solid bid in core global FI. Pressure was alleviated as Chinese equities rallied sharply from lows, resulting in desks and then major newswires suggesting that the Chinese "national team" had stepped in to quell the recent losses in the domestic equity markets. Still, broader core fixed income markets remained underpinned, even as regional equity indices recovered from worst levels.

- This allowed Tsys to bull flatten, with 30s sitting ~3.0bp firmer on the day, while T-Notes print +0-05 at 132-01, 0-02+ off best levels. In terms of market flow we saw the following: TYJ1 134.00 puts saw 1,875 lots sold on block, likely profit taking based on previously identified regional trading patterns. A FV/TY flattener (-7,435 lots vs. +4,825 lots). TYJ1 130.00 puts saw a 5,625 lot block buyer. Focus on the Treasury's mid-month auction schedule is evident. 3-Year supply gets things rolling today, which comes in the wake of an extremely poor 7-Year auction at the backend of February (which resulted in the well documented volatility witnessed on 25 Feb).

- JGB futures recovered from worst levels on the aforementioned defensive dynamic. There was little impact from a sub-par round of 5-Year JGB supply, with the recent round of core global FI vol. and questions surrounding the BoJ's ongoing monetary policy review likely dissuading aggressive bidding. 10s and 20s underperformed in cash trade, cheapening by ~1.0bp, with swap spreads running narrower across most of the curve. JGB futures saw a light bid into the close, closing 9 ticks below yesterday's settlement levels after briefly unwinding the entirety of Friday's post-Kuroda bid (with overnight weakness evident on the back of BoJ Deputy Governor Amamiya's comments re: 10-Year yield targeting & U.S. Tsy weakness witnessed on Monday). Local data had no tangible impact on the space.

- Aussie bonds managed to unwind most of the overnight/early Sydney pressure, even with a relatively heavy round of A$ corporate issuance outlined (targeting the belly of the curve). Still, the long end saw some lingering underperformance given the fairly linear recovery in the space, leaving YM +1.7, XM -0.9 at the close, with YM roll dynamics perhaps supporting the former a little more than otherwise would have been the case. A reminder that RBA Governor Lowe will speak on Wednesday. The address is titled "The Recovery, Investment and Monetary Policy." Elsewhere, A$1.0bn of ACGB 1.00% 21 November 2031 supply is due.

FOREX: Risk Tone Reverses

The greenback showed some weakness early on, but this was reversed along with risk tone as China state funds intervened in equity markets to stem losses.

- AUD has moved between gains and losses, the pair last up 15 pips at 0.7664. Data earlier in the session showed NAB Business Conditions rose to 15 in February, from 9 previously. The rate managed to shake off weaker iron ore futures to post gains. NZD struggled more than its antipodean counterpart, down 5 pips at 0.7123.

- PBOC fixed USD/CNY at 6.5338, just 2 pips above sell side estimates, offshore yuan weakened at the start of the session, USD/CNH touching 6.5515 as Chinese equity markets dropped. The yuan reversed its fortunes though, strengthening as equity markets reversed losses on touted intervention from China state funds. Offshore yuan is down some 125 pips, USD/CNH last at 6.5388, but still holding most of the gain from yesterday.

- JPY has weakened, data earlier in the session showed final Q4 GDP at 2.8% Q/Q, lower than the preliminary 3.0%, annualized GDP fell to 11.7% from 12.7%. Earnings data showed average wages fell 0.8% y/y in January, recording a 10th straight drop following a 3.0% fall in December. Real wages also remained in negative territory. Base wages, the key to a steady recovery in cash earnings, rose 0.3% y/y after falling 0.1% in December for the first rise in three months. USD/JPY has moved above 109.00, contacts noting USD/JPY demand from Japanese banks.

ASIA FX: Greenback Marches On

Further gains for the greenback on Monday saw Asia EM FX come under pressure from the open, but a reversal of sentiment saw most USD/Asia crosses retreat from session highs.

- CNH: PBOC fixed USD/CNY at 6.5338, just 2 pips above sell side estimates, offshore yuan weakened at the start of the session, USD/CNH touching 6.5515 as Chinese equity markets dropped. The yuan reversed its fortunes though, strengthening as equity markets reversed losses on touted intervention from China state funds. Offshore yuan is down some 125 pips, USD/CNH last at 6.5388, but still holding most of the gain from yesterday.

- SGD: Singapore dollar is stronger on the session, USD/SGD initially moved up to 1.3530, the highest since Nov 5, before dropping back to 1.3496 last.

- TWD: Taiwan dollar is weaker, USD/TWD rarely not spending the entire session under 28, the pair last at 28.348. Markets await CPI and trade balance data at 0800GMT/1600HKT.

- KRW: The won has weakened, stocks and bonds have both seen outflows from foreign funds have persisted for a third day.

- INR: The rupee has strengthened, but has come off best levels of the session. Markets focus on bond market developments amid a lack of local data.

- IDR: The rupiah continues to weaken, sliding despite intervention from the Bank of Indonesia yesterday.

- MYR: The ringgit has declined again, the latest resurgence of coronavirus and further restrictions are said to weigh on the outlook for GDP.

- PHP: The peso is stronger, resisting the prevailing trend of the region again. Data earlier showed the unemployment rate was steady at 8.7%

- THB: Baht is weaker, on track for a sixth day of losses which would be the longest losing streak since September, USD/THB is now close to challenging the 31.00 level.

ASIA RATES: Mixed, But Off Worst Levels; Auctions & OMOs Eyed

A drop in US yields made Asia debt more attractive, lower equity markets also boosted the appeal of sovereign debt markets, but some selling seen after China state funds were seen buying equities.

- INDIA: Space supported after a drop in US yields. Markets await the results of INR 216.7bn of bond sales by the state government for cues on investors' appetite for debt. Participants also await the increased purchase size Operation Twist.

- INDONESIA: Sovereign debt extends its drop ahead of the IDR 12tn sukuk auction later today, 10-year yields have gained around 25bps in the past three days.

- CHINA: The PBOC matched liquidity injections with maturities today, meaning the last liquidity injection was on Feb 25, with CNY 30bn being drained during that time. The overnight repo rate has jumped, last up 30bps at 2.0145%. Bonds futures are lower, 10-year future at sessions lows last down 0.220 at 96.94. Futures had been flat, with equity markets plunging, before China state funds stepped into buy equities, pushing markets back into positive territory and sapping support for fixed income.

- SOUTH KOREA: Bonds under pressure in South Korea, futures lower but off earlier worst levels. Decline in 10-year future is shallower after the Bank of Korea announced it will buy up to KRW 2tn of government bonds via auction today to improve liquidity in the bond market, the bank announced in February it would buy KRW 5tn - 7tn of government bonds in the first half of 2021.

FOREX OPTIONS: Expiries for Mar09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1610-15(E653mln), $1.1620-25(E562mln), $1.1640-50(E552mln), $1.1800(E652mln), $1.1835-50(E710mln), $1.1880-00(E662mln)

- AUD/USD: $0.7700(A$524mln)

- USD/CAD: C$1.2450($620mln), C$1.2550($545mln), C$1.2595-00($742mln), C$1.2725-30($828mln)

- USD/CNY: Cny6.56($500mln)

EQUITIES: Reversal

A mixed day for equity markets in the Asia-Pac region. Most indices were in the red with mainland China leading the way lower, the CSI 300 was down as much as 3.25% before reversing course, briefly printing in positive territory. The move higher was later confirmed to be the handy work of Chinese state funds buying stocks to support markets. The bid seeped into other markets, and saw markets in Japan, Hong Kong, Australia and India in positive territory, but South Korea is still lower on the day, but off worst levels.

- Futures in Europe and the US are mixed, the Dax is in negative territory after hitting a record yesterday, while US bourses are in minor positive territory. The Nasdaq has recovered the most after sustaining the worst losses yesterday, while the Dow managed to finish in positive territory, a divergence not seen since 2001.

GOLD: Off Worst Levels, Still Below $1,700/oz

Higher U.S. real yields and a firmer DXY pressured bullion on Monday, although a retrace from extremes has provided some support during the second half of Asia-Pac trade, with several inputs driving broader flows and flagged elsewhere. Spot last trades +$7/oz, hovering around $1,690/oz, after printing as low as $1,676.9/oz on Monday. Technically, bears need to force a break below the June 5 2020 low at $1,671.0/oz.

OIL: Crude Futures Pick Up After Decline

Crude futures sit a touch shy of best levels, with WTI & Brent printing ~$0.10 & ~$0.20 above their respective settlement levels at typing..

- The decline yesterday was attributed to USD rising to a three-month high, offsetting geopolitical risk concerns spurred by an overnight attack on Saudi Arabia oil infrastructure.

- There could be further pressure on oil, US refineries are resuming operations after the unprecedented cold blast in February, the Total Port Arthur refinery restarted its crude unit earlier in the session.

- Markets will look ahead to API inventory data; last week crude stocks rose for a third week in the previous period, while distillate and gasoline stocks fell.

UP TODAY (Times GMT/Local)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.